Electronification of bond trading makes order/execution management systems vital, yet traders feel they are having to push providers to keep pace. Dan Barnes reports.

If a trading desk wants to become really efficient it has to have tools that can give traders scale, speed and increasingly multi-asset functionality. However fixed income traders often find that order/execution management systems (O/EMSs) have been developed with bond trading as an afterthought.

John Greenan, CEO of capital markets consultancy Alignment Systems draws a parallel with the Pacer, a car made in the mid-1970s by AMC. The US design had the door on the right of the car longer than the door on the left, so people in the back seat could get out of the passenger’s side easily at the curb. When AMC decided to market the car in the UK they put the steering wheel on the right hand side, because that is where drivers sit in Britain. But they did not flip the doors around.

“OMSs similarly get built to work in America and then bastardised to try to work in Europe,” he says. “So they always do half the job but not all of it. Or they get built to handle equity workflows and bastardised to handle fixed income and other asset classes.”

Cash fixed income products are less liquid than other instruments due to the extent of issuance and consequently their market is less geared towards electronic trading models. As a result O/EMS vendors typically develop functionality in equity or FX markets and bring it into the fixed income space.

Christoph Hock, global head of trading at investment managers Union Investment, says “Regardless of whether you look at trading platforms or O/EMS in fixed income there is definitely room for development. When comparing the various asset classes it is fair to say that fixed income is not the most advanced when it comes to electronification. There are still a number of new protocols and platforms under development.”

Sticking points

The order management component typically transfers the request for an instrument from the portfolio manager to the trading desk and provides pre-trade and post-trade workflow to support internal operations. Execution management systems are focussed on the point of interaction between the trading desk and the market, with pre- and post-trade functionality to support effective execution. Working together – and with other tools or platforms – is where many OMSs fall down.

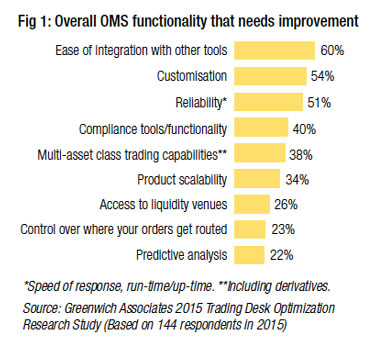

A survey by analyst house Greenwich Associates for its ‘Trading Desk Optimisation Research’ in 2015 found greater ease of integration between OMS and other tools was the most lacking functionality (see Fig 1). As bond markets become more electronic the need for greater integration of data flows and other tools including EMSs increases.

A survey by analyst house Greenwich Associates for its ‘Trading Desk Optimisation Research’ in 2015 found greater ease of integration between OMS and other tools was the most lacking functionality (see Fig 1). As bond markets become more electronic the need for greater integration of data flows and other tools including EMSs increases.

As sell-side firms pull back from risk trades across all asset classes, it becomes increasingly important for buy-side O/EMS platforms to provide the connectivity that will allow liquidity to be aggregated. The mistake for providers is to consider the models of trading across markets to be comparable says John Adam, global head of product management at EMS provider Portware.

“You are not working in an integrated market with exchange-distributed quotes,” he says. “If I am trading over-the-counter (OTC) my liquidity resources in the fixed income world are going to come from a variety of electronic platforms like Tradeweb or MarketAxess as well as voice relationships with my dealers.”

Under the revision of the Markets in Financial Instruments Directive (MiFID II), scheduled to come into effect in 2018, traders will see pre- and post-trade transparency increase dramatically.

“There is a risk that as more data becomes available in the marketplace, the cost of consuming that market data goes up substantially and people could be publishing it in incompatible formats which loads up the cost,” says Grant Wilson managing partner of Etrading Software which manages the not-for-profit FIX messaging utility Neptune. “We have seen a demand to look at standardising the market data consumption, so if there is an explosion of different data sources they can be amalgamated easily.”

Making the break

Changing an OMS can be tricky for several reasons and that can potentially limit the commercial pressure that OMS providers feel to change. OMSs are commonly a longstanding feature of a trading desk. When asked to rank their incumbent system against others, many heads of desk will acknowledge that having only used one or two for any length of time, frequently for up to a decade, it is hard to evaluate what they have against the full range of functionality available on the market.

“Most investment banks have technology management people who engage in strategic relationships with vendors,” says Greenan. “On the buy side, typically a head of trading comes in and on-boards the toolkit that he or she is familiar with, based on what they used at their last shop. I think that the lack of coordination is usual in buy sides.”

Nevertheless there are growing pressures on the buy-side execution desk that are driving heads of desk to consider the appropriateness of the systems they use.

“On the buy side the big focus on best execution and risk management has driven evolution, for example with a demand for better audit trails in order to prove that you have achieved best execution and fulfilled your fiduciary duty,” says Kevin McPartland, head of Greenwich Associates market structure and technology advisory service.

The rise of multi-asset trading desks, combined with the broadening of best execution requirements to all asset classes under MiFID II in Europe, is increasing scrutiny of O/EMS functionality across the board. “The days of having a single asset OMS or EMS are behind us,” says Adam.

Hock says when bringing together the equity, FX, fixed income and derivatives desks into one function he saw the imperative to assess the existing platform.

“We applied due diligence by looking at seven competitors to figure out if our current EMS system we are using was state of the art, and what is key for us is that the O/EMS provider can implement features that we consider essential for our best execution process,” he says.

Reasons to change

One global head of trading reported that his own delivery of a multi-asset trading desk led him to a decision between either adding an EMS to the firm’s existing OMS, or by exploring the different ways to complete the actual OMS framework by using best-in class trading tools, new asset classes and derivatives.

He chose the second option, which delivered cost savings and also trading efficiency, while he saw the opportunity to bring traders and IT teams closer.

“This was also a great collective challenge,” he says. “We first had to clarify our objectives, be pro-active, innovative and organise ourselves accordingly. Then, we have engaged in a strong dialogue with our OMS provider – we have some requests for the things we cannot do ourselves and we are happy to share work, for example in the area of fixed-income transaction cost analysis, with them.”

MiFID II is going to force dealers to track the various touch points they have with clients – for example in a typical workflow a buy-side desk client speaks to the salesperson, who speaks to the trader and a certain amount of negotiation occurs. Those touch points now need to be captured electronically, across functions under pre-trade and post-trade transparency requirements making effective electronification of orders increasingly important says Sassan Danesh, chief executive of Etrading Software.

“You need some kind of rules engine as soon as the client comes in to identify whether the instrument is liquid or illiquid. If it’s liquid, is the order above large-in-scale or below? Is there a waiver? In order to address this in a systematic manner you need a lot more digital information that can be analysed and processed with rules engines.”

For O/EMS providers, the demand for standardised, integrated systems is clear; however for software firms used to building proprietary, commercial technology, adapting to these new demands will be challenging.

©TheDESK 2016