An asset manager may need to assess the value that an outsourced trading provider offers using a range of measures in fixed income markets.

An asset manager may need to assess the value that an outsourced trading provider offers using a range of measures in fixed income markets.

Fixed income trading costs and trading execution quality are notoriously hard to quantify for asset managers. Not only are fixed income instruments traded using a wide range of cost models, with some traded on the bid-ask spread and others on fees.

When outsourcing a service to a third party, that typically requires a careful assessment of the value and cost that the in-house function provides, in order to measure it against that of an outsourced provider.

This would appear to present a potential challenge for the outsourcing of trading for fixed income, as a like-for-like comparison is hard to make.

However, outsourced trading providers say there are both quantitative and qualitative measures that can be used to assess both execution quality and the value of trading operations to compare insourced and outsourced models.

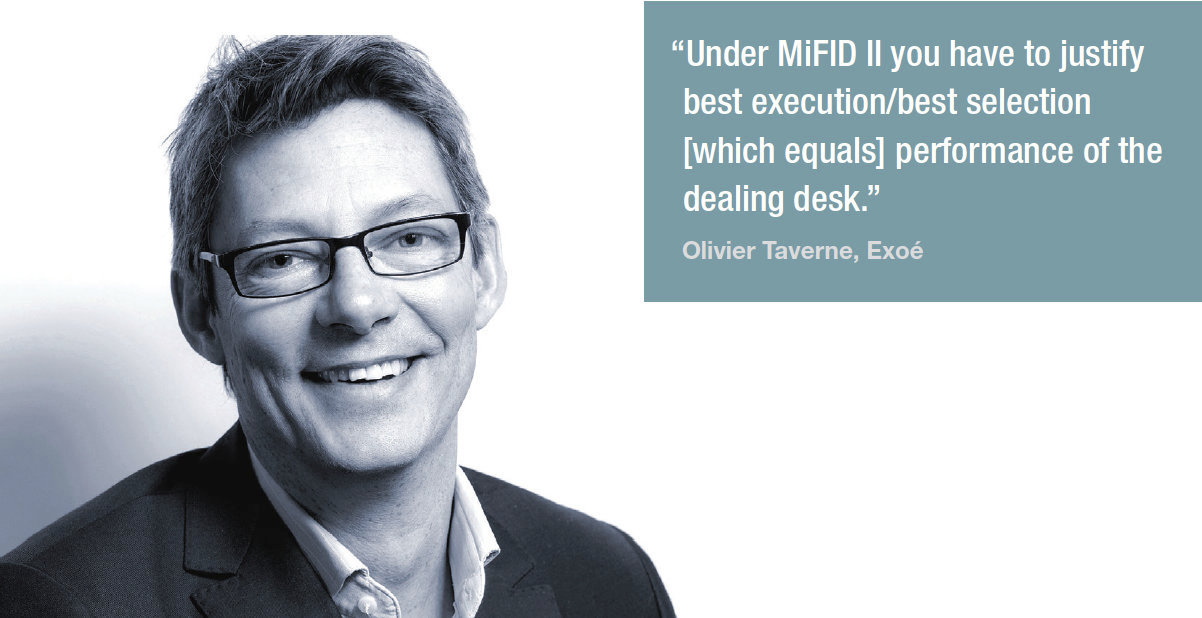

“Under MiFID II you have to justify best execution/best selection [which equals] performance of the dealing desk,” explains Olivier Taverne, of outsourced trading provider, Exoé. “As the dealing desk is in charge of execution strategy to reduce market impact, the dealing desk has to measure/quantify/collect proof of execution quality. For brokers who executed orders and the desk that made choices – because portfolio managers (PMs) are not interested in chasing whose fault it is – they want an aggregate performance.”

Consequently, all dealing desks have to justify performance improvements, “especially if it is an externalised one,” he observes.

“For anyone who is using an outsourced trading desk, the most important things to understand are around how you are structured,” says Shane Swanson, market structure & technology associate at analyst firm Greenwich Associates. “With the vendor you have to understand what that relationship brings and what matrix you are using for success. In particular, with outsourced trading you do have to have full knowledge of what they are doing, how they are doing it and that requires transparency. They are for all intents and purposes performing the function of an internal team.”

Quality of service

The abilities that an outsourced trading function provides can be more holistic than a numbers-for-numbers comparison, for example by increasing reach into new markets or to a wider selection of assets.

“Some firms that outsource are looking for cost reduction but more typically it is an expansion of capabilities that has driven adoption for outsourced trading,” says Swanson. “So if a fund doesn’t have global access they can basically adopt an outsourced trading vendor to have that global presence in one fell swoop. If they don’t have the ability to trade complex derivatives or cross assets, again outsourcing could be appropriate to give them that access in a straightforward manner.”

For instruments that typically have less data available to use for assessing the costs of a transaction, and may therefore have a harder time quantifying execution, outsourced trading potentially provides a more complete service.

Jack Seibald, co-head of global outsourced trading at Cowen says, “Having a solution that has the ability to go out and find liquidity for bonds that don’t trade as easily is where much of the value proposition will be seen. It’s getting deeper into corporate credit, including high yield and emerging markets.”

In cases where portfolio managers are trading directly rather than via in-house trading desks, either due to the company’s culture and strategy regarding PMs trading, or because the resources to develop a trading desk are proving too challenging to develop, engaging with a third party can deliver a bolt-on capability that has more fundamental effects.

“In that case, the question should rather be, does the portfolio manager miss out on opportunities in the market, because they spent too much time executing orders in other parts of the market,” observes Frank Lynge Jensen, chief trader at fixed income trade outsourcing specialist Sherpa Edge. “Are their clients, the investors, eventually worse off, because the time spent finding the right investment cases, doing thoroughly analysis and portfolio construction most often ends up being a residual of the time spent on executing trades, hence with the risk of delivering a product of lower value or quality?”

Where most PMs within institutional investment firms would have long-term investment goals, with the majority of alpha generated by picking the right investments, timing of the trading would typically have less impact, and therefore a PM’s primary goal could be said to be better spent on assessing those investment goals rather than managing the interplay around liquidity and price formation.

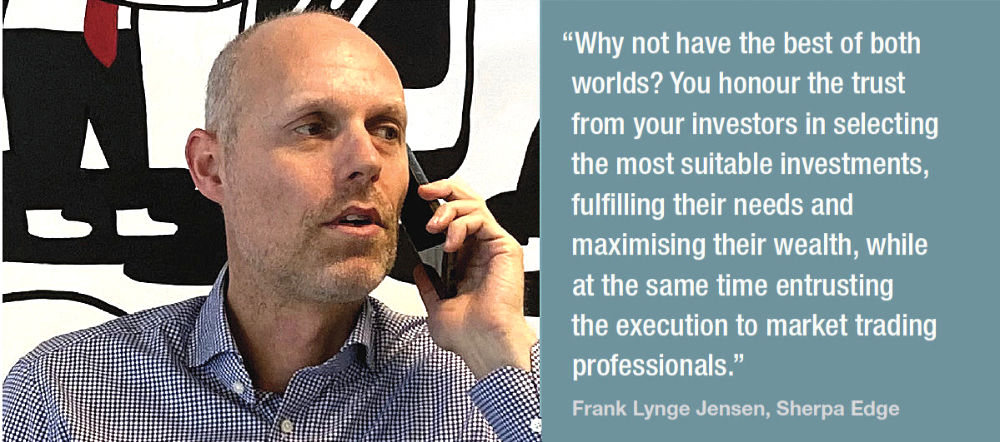

“Why not have the best of both worlds?” says Lynge Jensen. “You honour the trust from your investors in selecting the most suitable investments, fulfilling their needs and maximising their wealth, while at the same time entrusting the execution to market trading professionals. Agreed, the latter approach would be difficult to cost quantify beforehand and could also require a more holistic view.”

The value can also be delivered via a mutualised service model in which fixed costs – which might prove daunting for a small operation – are far more manageable for a provider who is trading at scale based on a larger flow of orders from multiple investment managers.

“We offer our clients a greater level of access to the institutional marketplace,” says Joram Siegel, head of fixed income outsourced trading at Cowen. “In an over-the-counter marketplace, access to liquidity is not the same across the board for all investors. Many of our clients have not been able to establish or don’t want to carry the cost of that infrastructure. We have direct relationships with liquidity providers and connectivity to the platforms to access it, maintaining that infrastructure so our clients do not have to.”

“We offer our clients a greater level of access to the institutional marketplace,” says Joram Siegel, head of fixed income outsourced trading at Cowen. “In an over-the-counter marketplace, access to liquidity is not the same across the board for all investors. Many of our clients have not been able to establish or don’t want to carry the cost of that infrastructure. We have direct relationships with liquidity providers and connectivity to the platforms to access it, maintaining that infrastructure so our clients do not have to.”

Quantifying execution

These qualitative elements of outsourced trading services should not preclude the understanding of trading costs and value. There are clear metrics which can be applied within the bond market space.

Lynge Jensen says, “The easy approach would be to start crunching the numbers: what was the volume traded last year, and which fee brackets did we trigger in each market? This should quickly leave you with a cost figure, easily comparable with the cost of running an in-house trading desk.”

Exoé says that its reporting to clients includes daily analysis, weekly committees, monthly reports and meetings every six months with PMs to analyse:

• List of brokers/counterparties and accordance with needs (flows, volumes, market caps, countries);

• Transaction cost analysis (TCA) approach;

• Blocks and improved liquidity;

• Fees and executions strategy (e.g. low touch/high touch);

• Toxicity and aggressivity;

• Broker review analysis with scores/ranking.

“Clients could also have a BI tool access to monitor daily performance [across] more than 15 pages of analytics,” says Taverne. “These results are used to improve pre-trade analysis and suggesting brokers for next period. On FI we add other anal-ysis with spread improvements, multiple RFQs etc.”

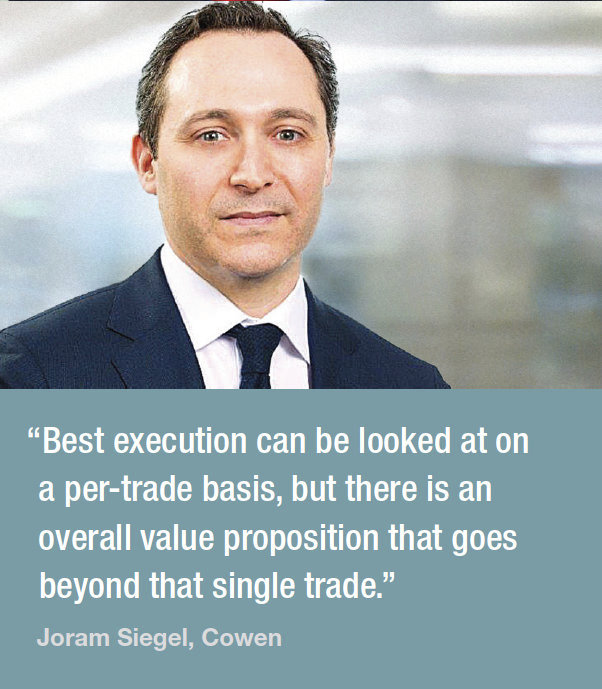

Siegel adds, “Best execution can be looked at on a per-trade basis, but there is an overall value proposition that goes beyond that single trade. We are offering a comprehensive service model that also helps our clients reduce their fixed costs.”

Acceptance of the outsourcing model is still relatively new to the bond markets, although it has found fertile ground amongst smaller and rapidly expanding firms.

“There are certainly firms that have used outsourcers as a stepping stone,” says Swanson. “Firms that are on a growth trajectory and want to dip their toe in the international waters, they outsource that. They learn what is needed to trade suc-cessfully in those markets and develop internal capabilities.”

However, he has found that that longer term use is increasing as buy-side firms become more comfortable with their measurement of outsourcing value.

“Increasingly it seems that outsourced trading desks are becoming more accepta-ble, or accepted as a practice,” he says. “Firms that have started up with an out-sourced trading as their trade desk, only have outsourced trading desks as their ex-ecution methodology.”

©Markets Media Europe 2026

more valuable")