Sell-side firms appear to be increasing their engagement with corporate bond trading platforms. The narrative of increased bilateral trading between dealers and clients has been well-reported, with The DESK first picking up the story in 2019, but contrary to some reports this appears to be in parallel with platform trading, not counter to it.

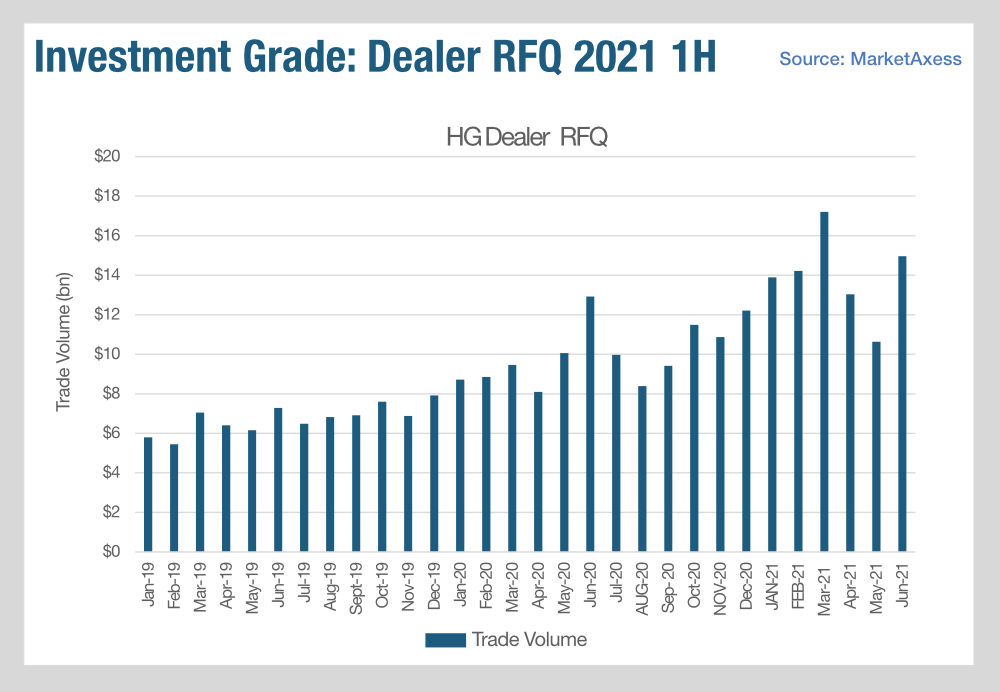

Trading volume for dealer request-for-quotes in investment grade (IG) on MarketAxess has reached US$84 billion to end of June 2021, up 44% year-on-year. That includes a jump in June, as volumes recovered from a dip after Q1. The same growth has been seen in high yield (HY) with US$34 billion in dealer RFQs year to date, up by approximately 44%.

Perhaps surprisingly, IG saw a record high in March 2021 of US$17 billion monthly volume against just over US$9 billion in March 2020 during the sell-off. This is positive as it suggests dealer engagement to find natural liquidity via platforms reflects a secular change of engagement, more than a response to market activity.

Notably, MarketAxess data has found that 43% of dealer inquiries traded with an end client, showing that the all-to-all model is functioning as an interdealer tool as well as a dealer-to-client model.

A recent report from Greenwich Associates observed that execution across both multi- and bilateral trading was being explored by buy- and sell-side traders and anecdotally The DESK has seen interest in these developments, but based on MDP engagement today it would seem the growth across these models is with the intention of scaling up trading capacity.

With no abatement in the concern about commitment of bank balance sheet to risk trading, it would seem prudent for buy-side traders to explore wider access to the credit and rates markets. The key challenge to this will always be resource; finding budget and time to support increased connectivity will be an imperative for traders in the next year.

©Markets Media Europe 2025

more valuable")

more valuable")