Dealers are now committing more capital in the muni market but future tax reforms threaten buy-side demand. Chris Hall reports.

Is the US municipal bond market experiencing a post-crisis correction, or exhibiting more worrying signs of systemic fragility and inexorable decline? It rather depends on your perspective. Annual trading volume fell by roughly half between 2006 and 2016 to US$3.14 trillion according to Municipal Securities Rulemaking Board (MSRB) data, while broker-dealer inventory levels also dropped by 50% (to US$25 billion) over the same period. A downward spiral that was accompanied by an accelerating sell-side stampede for the exit: the number of dealers registered with MSRB has fallen by 26% since October 2009.

Research shows many traditional retail bondholders already quitting the market – fewer than 1% of US households reported direct muni bond ownership in 2013, versus 3.5% in 1989, according to the 2015 report ‘Changing Patterns in Household Ownership of Municipal Debt’, by Daniel Bergstresser and Randolph Cohen. Will President Donald Trump’s tax-cutting agenda spell further trouble for the tax-exempt muni market?

For those with longer memories, current muni market trends represent a reversion to the mean, a welcome downsizing after a period of excess, albeit driven by post-crisis reforms.

Volumes might have plummeted over the past decade, but the pre-crisis 2000s saw the market pumped up above historical levels by proprietary trading, notes R.J. Gallo, head of municipal bond investment group, at Federated Investors. Broker-dealer prop desks and muni-specific hedge funds fuelled a surge in trading volumes that subsequently collapsed in the aftermath of the crisis, with many burned by losses sustained through forced sales as the era of leverage dissolved.

Reverting to type

The Dodd-Frank Act’s Volcker Rule permitted banks to continue to invest in munis, but the post-crisis period saw a sharp reduction in appetite and capacity with many surviving hedge funds reorientating their strategies as broker-dealers undertook the wholesale readjustment of their fixed-income businesses under the new conditions imposed by the Basel Committee and the Financial Stability Board, which penalised leverage and constrained balance sheets.

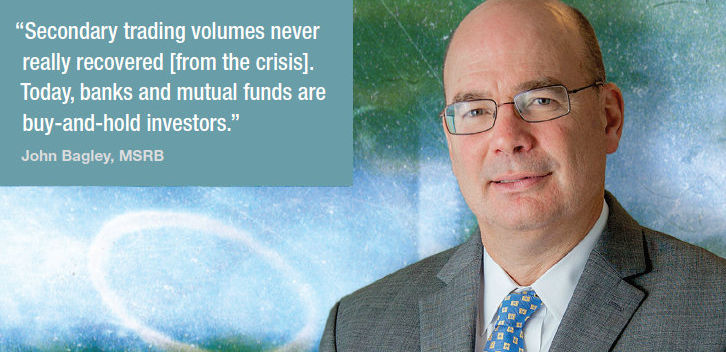

A key factor was the disappearance of tender option bond (TOB) programmes, which accounted for as much as 85% of secondary market muni trading in the immediate pre-crisis era. Typically sponsored by banks to provide short-term muni bond liquidity to money market and closed-end funds, TOB programmes were a casualty of the crisis and banks were barred by Volcker from creating new ones. Congress has delayed the forced liquidation of existing programmes but, according to MSRB chief market structure officer John Bagley, “Secondary trading volumes never really recovered. Today, banks and mutual funds are buy-and-hold investors.”

Nevertheless, Gallo is comfortable with his firm’s ability to source muni bond liquidity. “We’re still trading good volumes with around 20-30 firms,” he says. While Gallo asserts that there is still a wide array of sell-side counterparts in both the primary and secondary markets, he nevertheless recognises the challenges posed by the post-crisis decline in capital commitment levels. “There is less trading volume and lower fixed-income liquidity generally, but we are still able to navigate our portfolios very successfully. Markets do tend to ‘gap’ more, for example when there are fears of an interest rate hike. In times of stress, the market re-prices more rapidly, but things soon calm down once a new price level has been found,” he says.

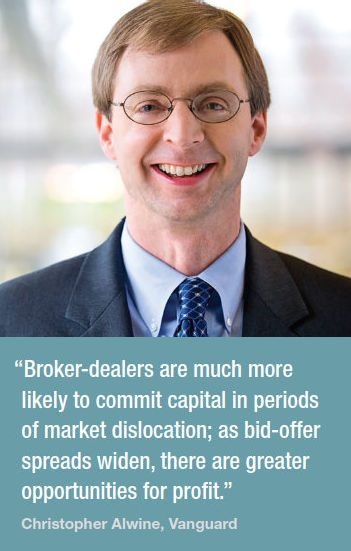

Like Gallo, Vanguard’s head of municipal bonds, Christopher Alwine, sees the mid-2000s as something of an aberration in the muni market, asserting that today’s market conditions are only marginally less conducive than the early 2000s, in terms of liquidity levels and market impact. While he notes a decline in capital commitment by broker-dealers in recent years, he attributes this not only to post-crisis reforms. “Broker-dealers are much more likely to commit capital in periods of market dislocation; as bid-offer spreads widen, there are greater opportunities for profit,” he observes.

Like Gallo, Vanguard’s head of municipal bonds, Christopher Alwine, sees the mid-2000s as something of an aberration in the muni market, asserting that today’s market conditions are only marginally less conducive than the early 2000s, in terms of liquidity levels and market impact. While he notes a decline in capital commitment by broker-dealers in recent years, he attributes this not only to post-crisis reforms. “Broker-dealers are much more likely to commit capital in periods of market dislocation; as bid-offer spreads widen, there are greater opportunities for profit,” he observes.

There are fewer block trades in the muni market in current conditions and higher levels of market impact due to lower trading volumes, but Alwine suggests that institutional market participants have adjusted to prevailing market realities over the past three to five years. “Broker-dealers are unlikely to use up balance sheet on a single CUSIP [Committee on Uniform Securities Identification Procedure instrument], but it’s a different story for smaller trades over a number of CUSIPs,” he says.

The buy-side opportunity

Thus periodic schisms should not necessarily be seen as signs of growing market inefficiency, rather as symptoms of adjustment to conditions which may yield opportunities for investors. The taper tantrum of Q2 2013 saw an upward leap in 10-year muni yields, as did November’s election result, which confounded entrenched expectations of higher taxation under Hillary Clinton, prompting a sharp reversal of year-long inflows. “There may be more frequent short-run overshoots to fair value,” says Alwine, but he insists this should not be mistaken for a more fundamental systematic weakness, pointing to the buyers that absorbed November’s outflows.

Tabb Group CEO Anthony Perrotta suggests there has been a post-crisis emergence of a new model for liquidity provision for municipal bonds, which echoes trends elsewhere. In the decades preceding the crisis, secondary market success relied on the ability of broker-dealers to hold inventory in a sufficiently wide range of issues to be a first or early dial for investors. However, the squeeze on balance sheets imparted by Basel III and other post-crisis reforms forced broker-dealers to either abandon or adjust this capital-intensive model.

Tabb Group CEO Anthony Perrotta suggests there has been a post-crisis emergence of a new model for liquidity provision for municipal bonds, which echoes trends elsewhere. In the decades preceding the crisis, secondary market success relied on the ability of broker-dealers to hold inventory in a sufficiently wide range of issues to be a first or early dial for investors. However, the squeeze on balance sheets imparted by Basel III and other post-crisis reforms forced broker-dealers to either abandon or adjust this capital-intensive model.

In short, firms with large distribution networks across one or more of the key muni investor groups shifted to sourcing liquidity for clients on a riskless principal basis, relying on information from clients to source and price liquidity cost-effectively, but without taking on positions themselves. Anecdotal evidence suggests investors are increasingly comfortable with an order-driven market model in which immediacy can no longer be guaranteed, but which nevertheless offers strong probability that the other side of the trade can be found through broker-dealers’ intensified efforts to leverage their client information networks. Perrotta see parallels with other markets that have seen an increase in the share of agency and/or riskless principal business.

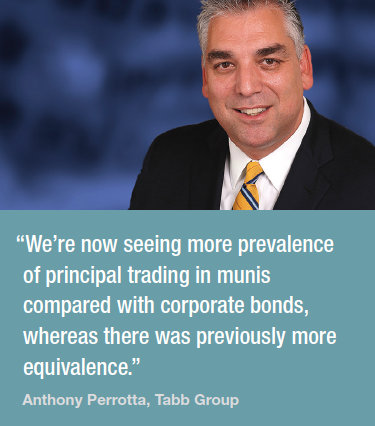

“In this model, broker-dealers are no longer using up balance sheet to facilitate client trades,” he says, warning that the increased value of information can make it harder to mask trading intentions. “That said, we’re now seeing more prevalence of principal trading in munis compared with corporate bonds, whereas there was previously more equivalence. Among the larger dealers that are experiencing a rebound in trading profitability, there is more willingness to commit capital.”

Brass tax

The secondary market may be in rude health, but political and economic developments have increased attention on the primary market, which has been far from immune from municipal bonds’ post-crisis realignment. As Basel forced big liquidity providers to draw in their horns, consolidation also shrank the pool of regional broker-dealers, but with almost 1450 MSRB-registered firms, Alwine suggests the sector is still overbanked.

More of a concern is the impact of impending tax reform. Aggressive tax-cutting by the Trump administration could weaken the rationale for holding munis for several investor constituencies, while a revival of Obama-era proposals to cap income tax-exemption benefits to muni holders has also been mooted. Either could weaken demand for munis at a time when local, state and city governments are expected to fund another part of the Trump agenda: infrastructure renewal.

Having made one significant post-crisis adjustment, Natalie Cohen, head of municipal research at Wells Fargo Securities, believes the muni market will be granted time to adapt again to changing circumstances. “The probable extended timeframe for tax reform will help the market to adjust, but much will still depend on the details of the proposal agreed by Congress. With infrastructure plans more likely to find Democratic support, we could see some new issuance in the second half of 2017,” she says.

©TheDESK 2017

©Markets Media Europe 2026

more valuable")