Based on their own view of TCA success, buy-side traders could apply analytics to support trading and execution goals.

Based on their own view of TCA success, buy-side traders could apply analytics to support trading and execution goals.

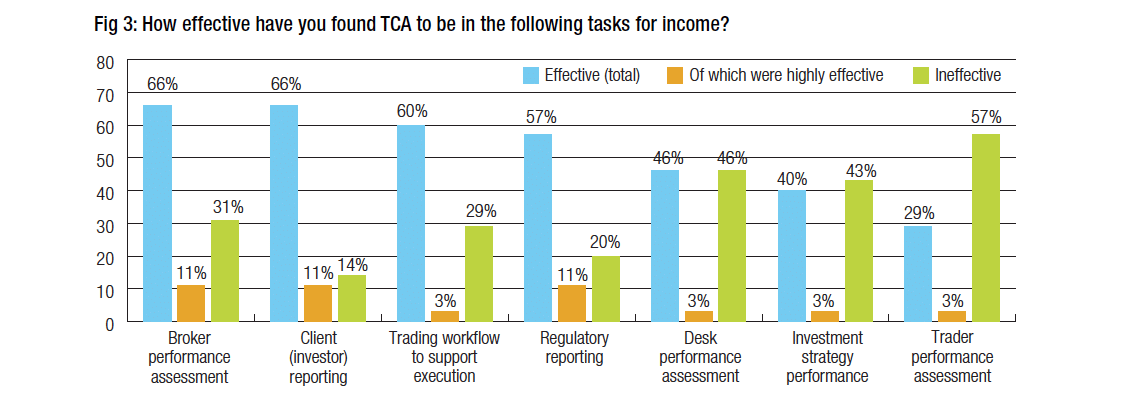

The DESK has found that fewer than half of buy-side bond traders use execution analytics in the trading workflow to support trade execution, but nearly 70% believe it is effective or highly effective in the role, suggesting there is an opportunity to expand its use.

In primary research, conducted across 35 asset management firms, The DESK examined the use of trading analytics and transaction cost analysis (TCA) in fixed income markets, to assess how it is used, where it is effective and which service providers are employed.

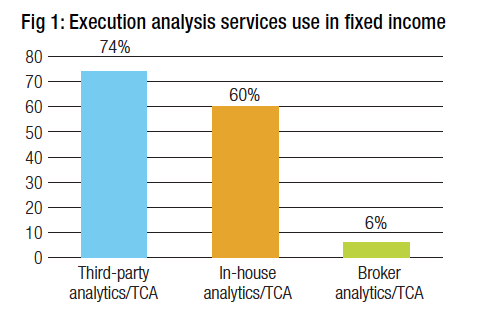

The majority of trading desks use analytics provided by third-party providers and in-house systems (Fig 1). Very few use broker supplied analytics which is in direct contrast to the equity market in which sell-side firms such as Virtu (through its acquisition of broker ITG) have been longstanding suppliers of TCA services.

The majority of trading desks use analytics provided by third-party providers and in-house systems (Fig 1). Very few use broker supplied analytics which is in direct contrast to the equity market in which sell-side firms such as Virtu (through its acquisition of broker ITG) have been longstanding suppliers of TCA services.

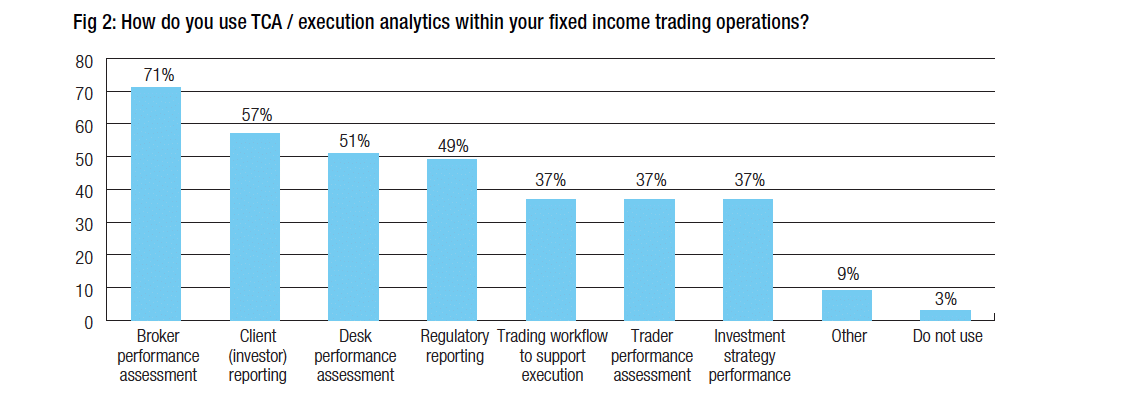

In the fixed income space, more than 50% of respondents (Fig 2) used trading analytics for tasks such as broker review, for client reporting and for assessing trading desk performance with just under half (49%) also using it for regulatory reporting.

It is used far less for supporting the trading workflow, for assessing tasks such as trader performance and for use in investment strategy performance, although nearly 40% of respondents are employing analytics for this purpose reflecting the strong division in employment.

When the current use of TCA / analytics is compared to the effectiveness that traders assign to the service (Fig 3), there is an imbalance between use and perceived effectiveness. For example, 60% of traders think it effective in the trading workflow, only 39% use it for that purpose.

There are also very split views of effectiveness, 46% thought TCA effective for desk performance and 46% thought it ineffective. A slight majority thought it ineffective at assessing investment performance, against (40%) who thought it effective.

Unpicking the division

To look into the possible causes of these divisions, we assessed those result on a supplier basis and on a portfolio basis i.e. which types of portfolio were being traded for, as both of these are dynamics which could affect use and affect performance.

As respondents typically trade for a wide range of portfolios, this did not prove a viable way to clearly delineate asset managers.

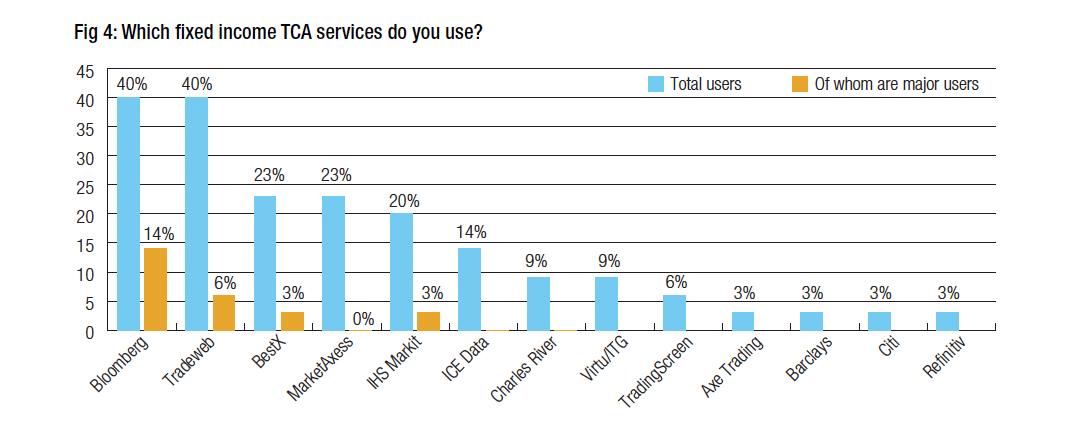

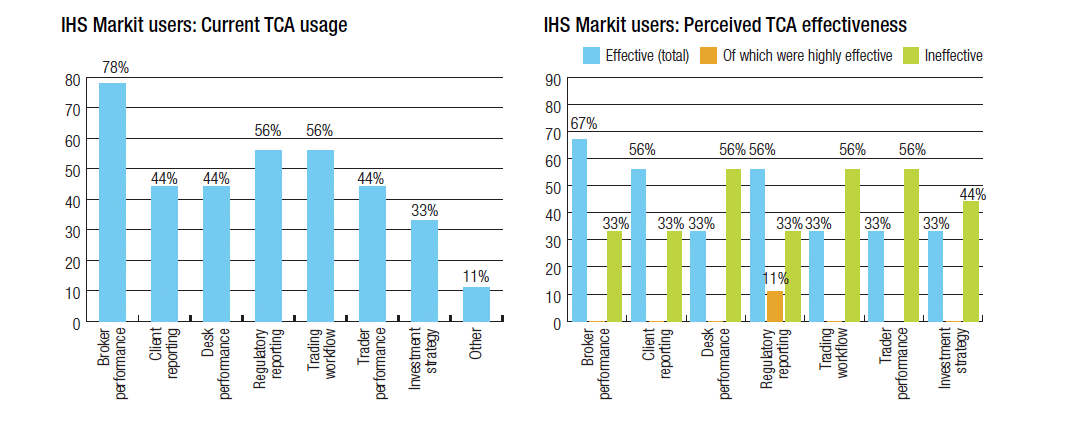

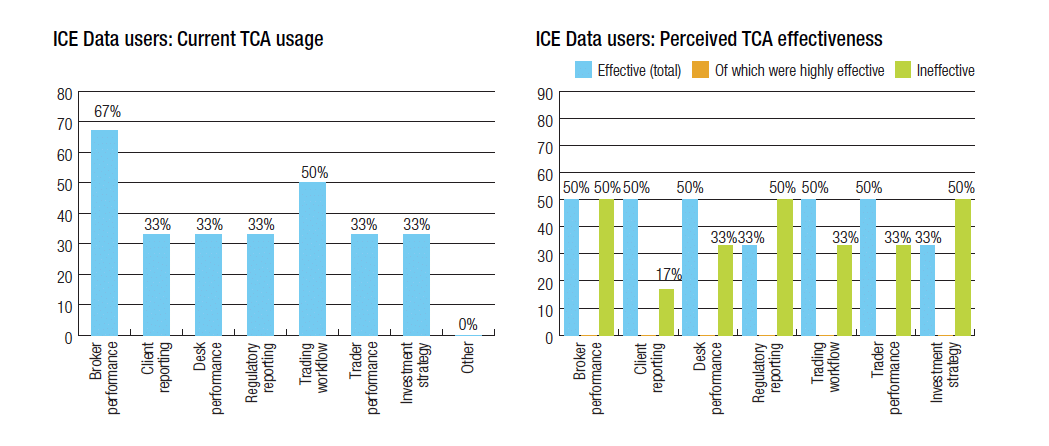

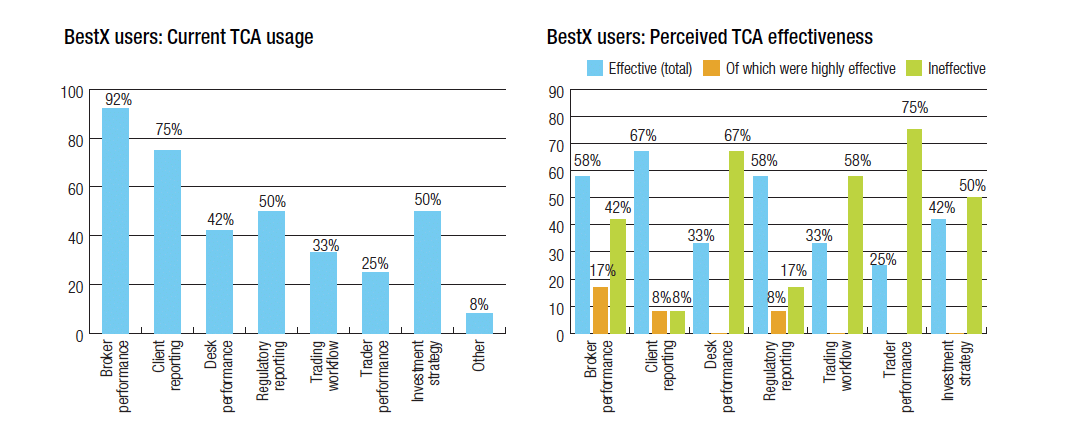

By contrast, the average buy-side firm only used between one and two third-party TCA providers. The top five most popular ranked by total users and the proportion of those who are major users, are Bloomberg, Tradeweb, BestX, MarketAxess and IHS Market (Fig 4). Each of these provides a range of services to clients.

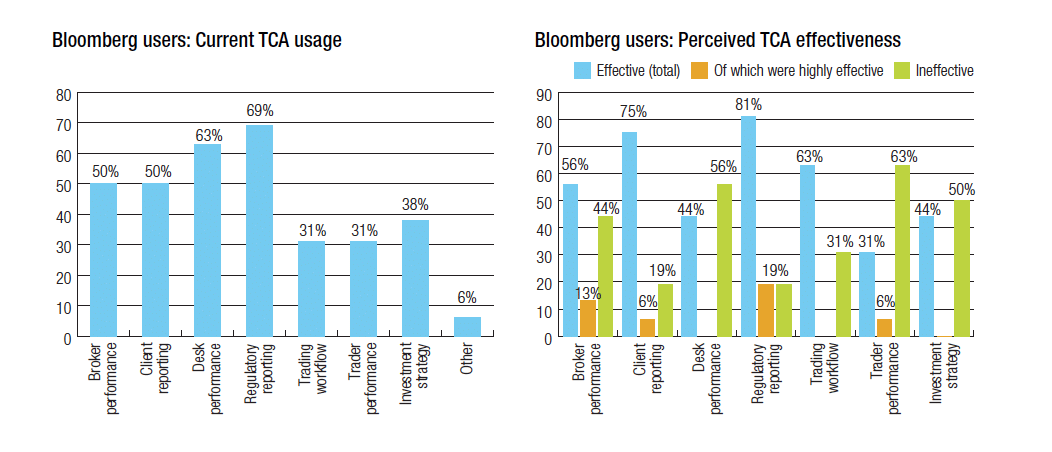

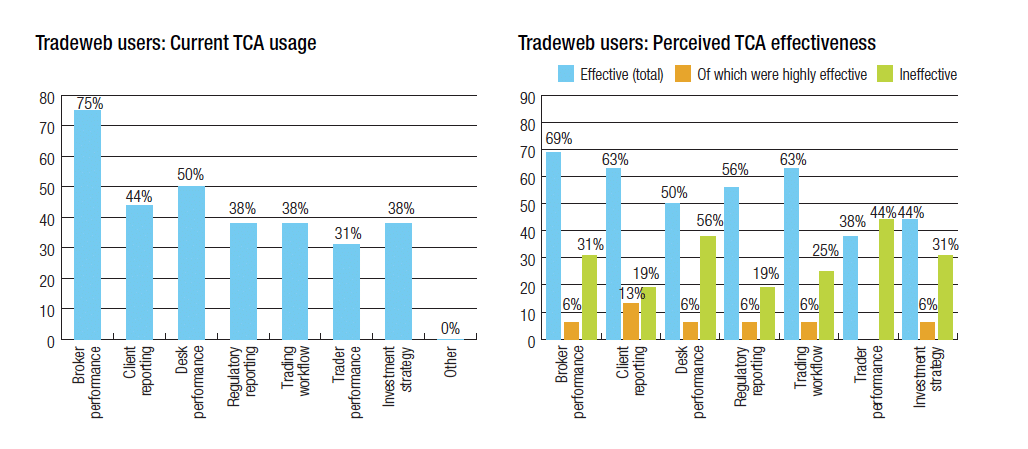

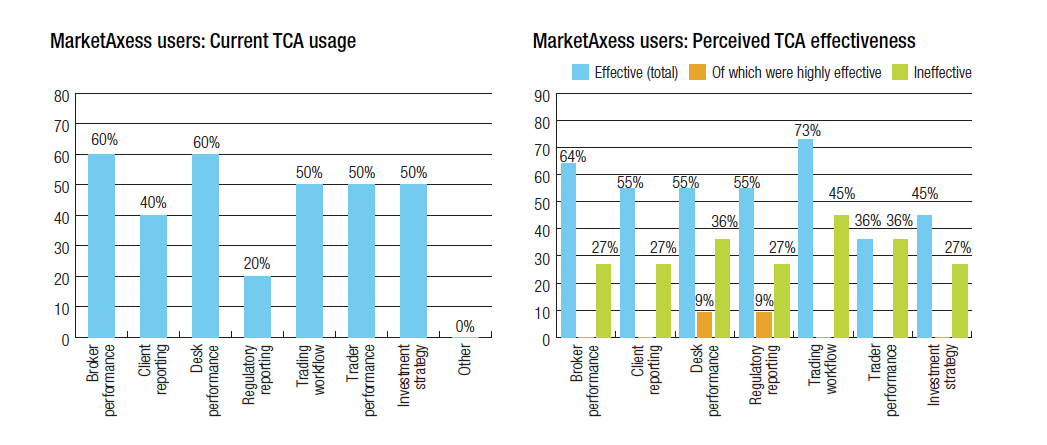

By analysing responses for firms that use particular service providers (not always exclusively), we find clear usage differences. For example, traders who use Bloomberg primarily used TCA for regulatory reporting (69%) and desk performance (63%) while the most common applicaton for traders using other platforms is to assess broker performance. By comparison regulatory reporting is low down the curve for Tradeweb and MarketAxess users.

By analysing responses for firms that use particular service providers (not always exclusively), we find clear usage differences. For example, traders who use Bloomberg primarily used TCA for regulatory reporting (69%) and desk performance (63%) while the most common applicaton for traders using other platforms is to assess broker performance. By comparison regulatory reporting is low down the curve for Tradeweb and MarketAxess users.

Users of ICE, IHS Markit and MarketAxess tools are for the most part bringing TCA and analytics into their trading workflow to support execution, while the users of other platforms have a lower proportion (below 50%) doing so.

The division between perceived efficacy and use is replicated at a service user level. For example, 75% of Bloomberg users report that TCA is effective for client investor reporting, yet only 50% of them use TCA for that purpose; 63% see it as effective at supporting the trading workflow while just 31% employ it for that purpose.

Double-digit levels of users consider TCA to be ineffective, for any given use case, bar one – just 8% of BestX users think TCA is ineffective at client reporting.

While there is some scepticism of TCA effectiveness for many tasks for which it is currently used there are also successes. Feedback from traders is that the buy-side needs to consider how to get better service from providers.

This includes better communication between buy-side traders and TCA providers, particularly in the questions that TCA services are capable of answering today. Although there is broad agreement that trying to provide services to too wide a set of buy side firms can lead to none of them being happy with the result, it is also acknowledged that the TCA providers have limited resources.

If buy-side traders can present a unified set of requirements for service providers, that could help to deliver better services across the board.

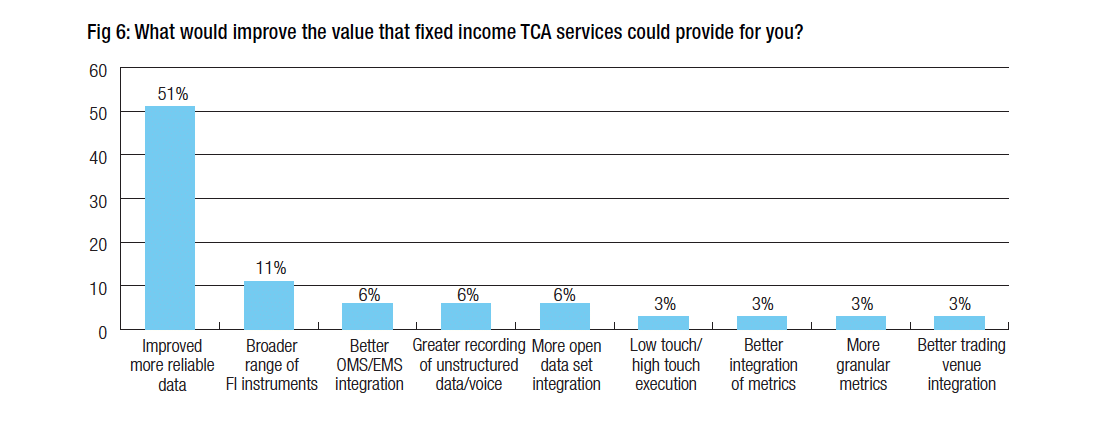

The greatest challenge is data (Fig 6), according to respondents, with 51% citing ‘improved quality and more reliable data’ as the one factor that would improve the value of fixed income TCA services. With both US and European regulators making steps towards more standardised transparency in fixed income, better data ought to be available publicly or commercially in the bond markets in coming years.

Demographics

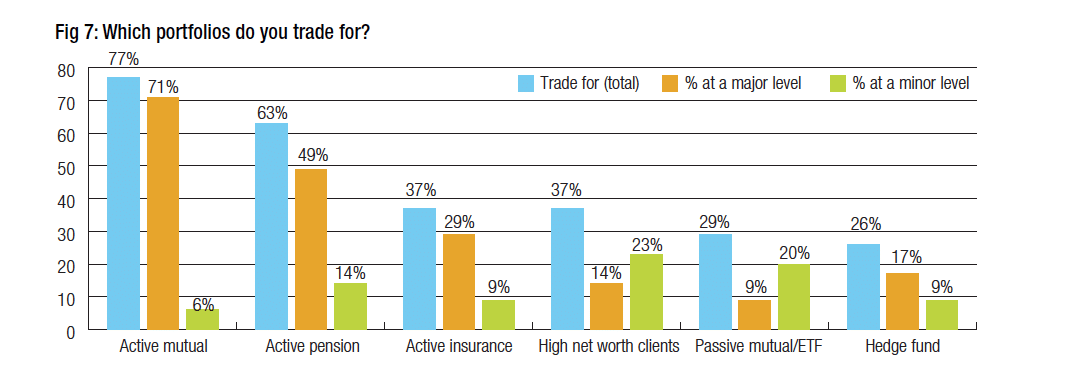

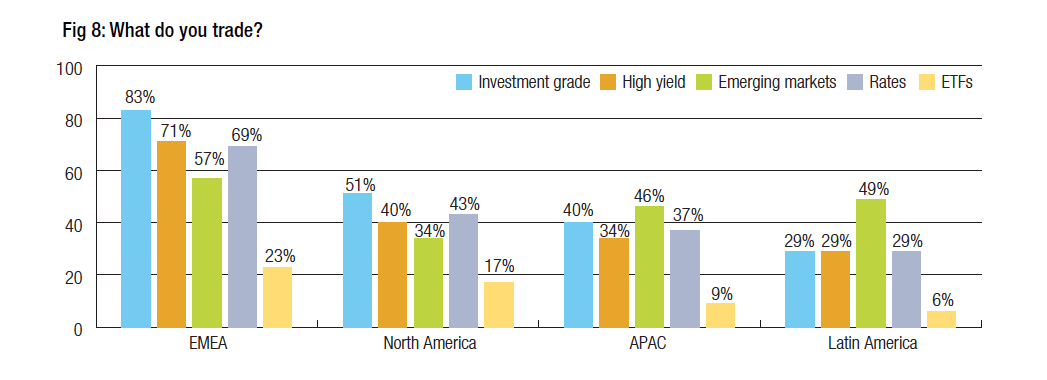

Thirty five buy-side trading functions from different took asset managers took part in this research trading for a range of portfolios (Fig 7) and across different asset classes and geographies (Fig 8). We would like to thank all of those traders and asset managers who took part.

©Markets Media Europe 2026

more valuable")