US market regulator the Securities and Exchange Commission (SEC) has engaged in a series of initiatives that could collectively bring more structure and standardisation to the US fixed income markets.

In September 2020 the SEC proposed to “enhance the operational transparency, system integrity, and regulatory oversight for alternative trading systems (ATSs) that trade government securities as well as repurchase and reverse repurchase agreements on government securities,” by making government bond trading venues comply with Reg ATS, a set of rules that are commonly applied to trading venues for equity markets.

It also asked for comment on proposals to extend the regulatory framework for electronic platforms that trade corporate debt and municipal securities.

On 1 October 2020 the SEC’s Fixed Income Market Structure Advisory Committee (FIMSAC) recommended clearer reporting of electronic trading, as no consistent standard exists for publicly reporting electronic trading over the 20 trading platforms which it noted currently trade corporate and municipal bonds.

“Multiple inconsistent practices characterise the discretionary disclosure of volumes by the individual venues,” the committee wrote. “In some cases, the trading and settlement protocols of the varying platforms also impact the volumes that they and dealers report to TRACE. As a result, volumes are reported inconsistently, which makes interpreting them difficult.”

The problem this creates is in the inconsistency of reporting methods which limit the ability of regulators, market participants, investors, and researchers to look at aggregate trends in electronic trading volume and market share across fixed income markets.

Reporting to the Trade Reporting and Compliance Engine (TRACE) industry utility run by FINRA can be affected by inconsistencies in the data – for example where prices do not reflect the trading protocol used to execute an order – and that creates real problems.

“Remember, banks use TRACE data as an input to their risk limits, among other things, so this data really matters,” wrote Kevin McPartland, Head of Research for Market Structure and Technology at analyst firm Greenwich Associates in a recent paper ‘All Electronic Trading is Not Created Equal’.

As a result, determining the effect of electronic trading on liquidity conditions and transaction costs over time is difficult, noted the FIMSAC.

“Investors in the e-trading venues, whether public or private companies, lack precise information on volume and market share trends for the various companies in the fixed income e-trading sector, making investing decisions more difficult,” they wrote. “Further, without clear disclosure as to whether the various electronic trading volumes are limited to the retail, inter-dealer, or institutional customer markets, knowing whether electronic trading is bridging these disparate liquidity pools or whether they remain mostly separate is challenging.”

The committee has recommended that the SEC, in coordination with FINRA and the Municipal Securities Rulemaking Board (MSRB):

• Clearly define “electronic trading” so that any new regulation or framework comprehensively covers the platforms and trading functionality that the SEC intends to cover without reliance on the current ATS definition;

• Take the above-discussed factors into account when defining ‘electronic trading,’ including single dealer versus multi-party execution and fully-electronic versus post-trade processing; and

• Establish industry-standards for electronic trade reporting that address the current inconsistencies described above relating to ATS functionality, single-counting versus double-counting, and the treatment of “give-up” trades for settlement.

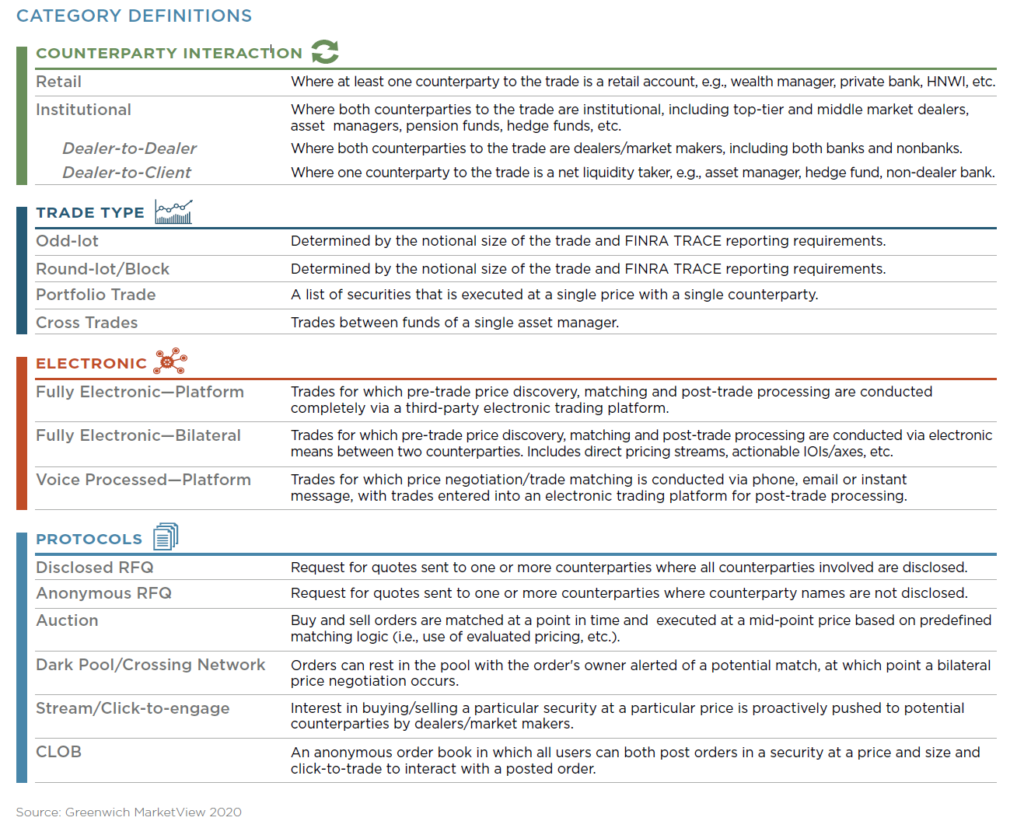

Greenwich Associates has defined a proposed set of standards, and it says nearly every US corporate bond trade executed could be defined by assigning one value from each of these four categories:

In the mean time, the application of Reg ATS would require government securities ATS operators to publicly disclose on Form ATS-G information about its manner of operations and the ATS-related activities of the registered broker-dealer or government securities broker or dealer that operates the ATS (broker-dealer operator) and its affiliates, and is designed to allow market participants to assess conflict of interest and understand how their orders will interact, match, and execute in the ATS.

This would create far greater transparency around the US treasuries market than exists today. Specifically, Form ATS-G would require a Government Securities ATS to disclose information regarding:

• Its broker-dealer operator, including identifying information and ownership.

• ATS-related activities of its broker-dealer operator, and the broker-dealer operator’s affiliates, including:

• the trading activities of the broker-dealer operator and its affiliates on the ATS;

• whether subscribers to the ATS can opt out from interacting with orders and trading interest of the broker-dealer operator and its affiliates;

• arrangements between the broker-dealer operator or its affiliates and other trading venues to access the ATS services;

• products and services offered to ATS subscribers by the broker-dealer operator and its affiliates;

• the activities of service providers to the broker-dealer operator and its affiliates; and

• written safeguards and written procedures established to protect the confidential trading information of subscribers.

• The manner of operations of the Government Securities ATS, including:

• types of subscribers, the criteria for eligibility for ATS services, and conditions for excluding subscribers from ATS services;

• means of entry for orders and trading interest;

• connectivity and co-location procedures;

• order types, attributes, and order size requirements and procedures;

• use of and conditions governing indications of interest;

• hours of operations, opening, reopening, and closing processes, and procedures for trading outside of the ATS’s regular trading hours;

• trading services, facilities, and rules of the ATS;

• arrangements with any subscriber or the broker-dealer operator to provide liquidity;

• segmentation of orders and trading interest and the provision of notice regarding segmentation;

• counter-party selection;

• display of orders and other trading interest;

• functionalities or procedures to facilitate trading on, or source pricing for, the ATS using markets for financial instruments related to government securities;

• fees;

• procedures for stopping or suspending trading;

• procedures regarding trade reporting, clearance, and settlement;

• sources and uses of market data; and

• aggregate platform-wide order flow and execution statistics provided by the ATS to one or more subscribers.

The proposed rules would also provide a process for the SEC to review Form ATS-G filings and, after notice and opportunity for hearing, declare Form ATS-G filings ineffective.

This level of accountability has been absent to date and the lack of supervision in US Treasury markets has led to considerable criticism which regulators had not previously responded to.

©Markets Media Europe 2026

more valuable")