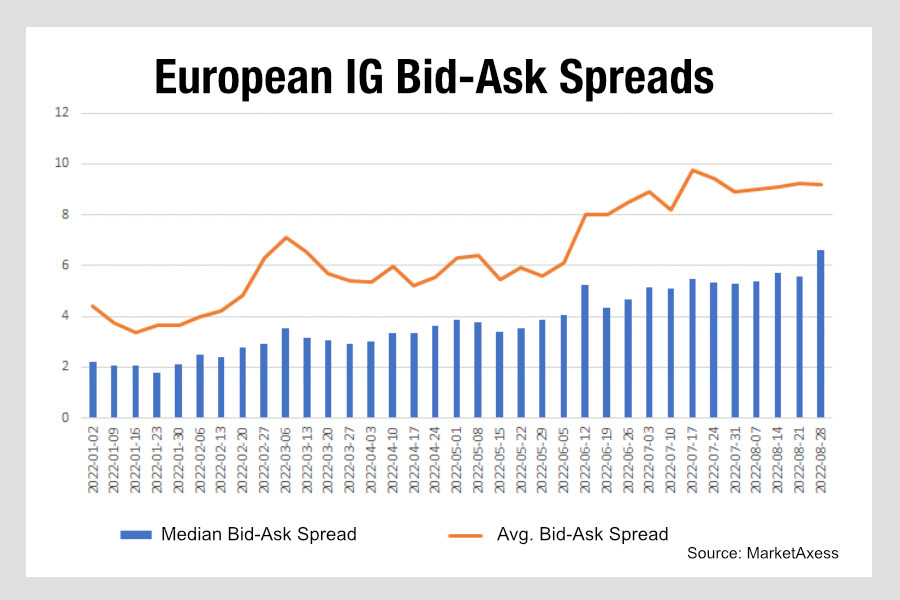

Liquidity in the European corporate bond market is becoming more expensive in both high yield (HY) and investment grade (IG) trading. According to MarketAxess data, where average bid-ask (BA) spreads were around four basis points for IG in January, they have more than doubled to bounce between 8-10 bps from June to August

Europe’s IG markets have been worse hit than US IG but as the European Central Bank hikes rates this is only likely to increase as a result of market volatility.

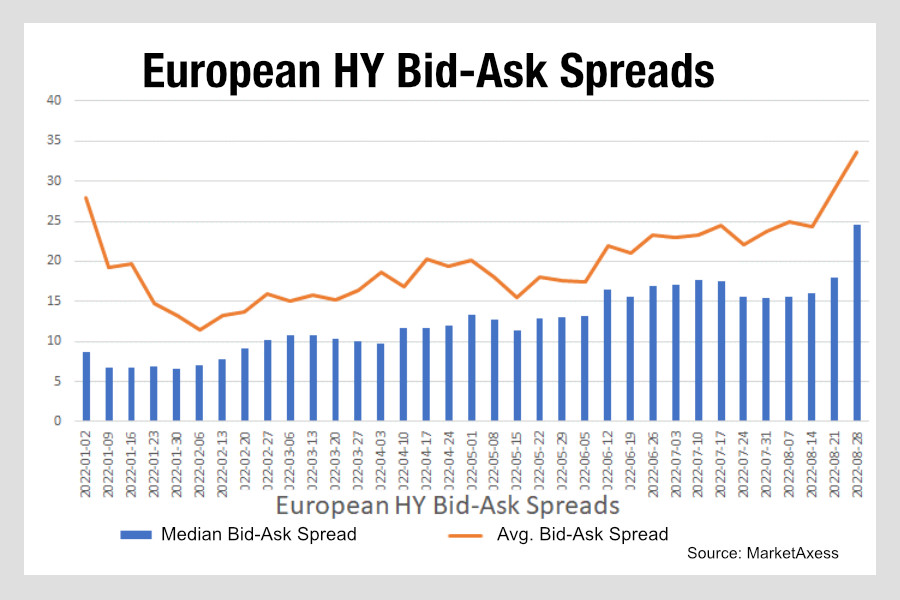

HY BA spreads are also shooting up at the end of summer to their highest levels this year.

Two possible causes are the complexity of European markets and the sophistication of US market makers, who have developed central risk books to help their trading desks manage positions more efficiently.

The response from traders will need to be twofold. Firstly, they will need to prep with portfolio managers, so that the increasing costs of liquidity are factored into any investment and portfolio decisions.

Secondly, they will need strategies to bring down BA spreads wherever possible. Market makers who have held up well are often those with either a central risk book, who are able to recycle e risk more effectively into the market without falling over their own feet, and those with strong exchange-traded fund (ETF) market making teams, which allows them to transfer the liquidity from the ETF markets into cash bonds and vice versa.

Bringing down spreads will not only be based upon strong broker relationships but also wider all-to-all networks in order to find liquidity wherever possible – bidless markets have become a real problem at times – so finding natural liquidity anonymously can be a real help particularly for smaller trades.

Finally, using data to work out where fair value is pre-trade will be challenging but invaluable if a reliable model can be established.

©Markets Media Europe 2026

more valuable")

more valuable")