Paul Squires, Head of the EMEA Equities and Henley Fixed Interest dealing teams at investment management company Invesco discusses the benefit of experience, the state of electronic trading and how well his trading teams have coped in the pandemic.

What is your role today?

I run two trading teams – EMEA equities for all PMs across the global organisation and then Henley fixed interest which is a slightly different remit in that it involves all trading across a wide range of instruments but just for the single investment team in Henley which manages £28bn in assets. It covers cash management as well as fixed income, OTC derivatives, repo and FX.

What has been the impact of Covid-19 on your trading ?

Working from home was a very different prospect for all of the traders but we adapted to the initial upheaval quickly with communication prioritised and operational aspects almost instantly addressed. Over the past two years we have spent a great deal of time developing an electronic trading platform which has been particularly useful in this environment. It gave us a roadmap to follow order execution through our electronic channel and the ability to articulate what the right strategy was during a period of intense volatility and high workload. The evolution of the trading tools, algo wheels, research and data also provided a robust operational foundation. Although risk trading largely disappeared with the high volatility, we also had a concentrated group of brokers that did provide balance sheet to us with capital commitment because of the long-term relationships that we have cultivated.

Did your experience with past unprecedented events such as the financial crisis help navigate the market volatility in the Spring?

I don’t think you realise how meaningful those experiences are until you are faced with other extreme events, and then you realise you can get through it. We had such a long period of low volatility that even relatively experienced traders may not have been through the kind of scenario we saw in March. I was lucky that I had enough experienced people in my teams that we were able to navigate through it. It has also been a good experience for young traders to go through something like this. So much of what we do has become scientific, data driven and built on prescriptive recommendations, but it is based on benign market conditions. The balance tips in these events because historic data analysis becomes less relevant while the human value-add (intuition and instinct) becomes much more significant.

How easy was it to switch to a remote working environment and what do you think the long-term impact will be?

Invesco has for some time been promoting agile and flexible working as part of their wellbeing programme. For traders however, working from home was traditionally just done when required to test our business continuity plan. It is one thing to do it under a BCP or for the occasional day and quite another long-term. That said, the switch to working from home was a lot smoother than anyone had anticipated. We chose to send people home before lockdown was enforced and within 48 hours everyone on my teams were doing their jobs to the usual standards. In the past, traders thought they couldn’t work remotely because the technology wouldn’t stand up or the proximity to colleagues was so essential. What we have found is that we can adapt, even if the methods of retaining the communication with each other for example might be managed differently.

My equity team has three calls each day – pre-market, midday and close of day – initially this was as much to make sure that everyone was OK and we were communicating on the major work tasks but, it has become our normal routine now. For the fixed income traders, we only have one call a week but it is a longer one to catch up on more strategic work. What they do more of however is relay streams of information throughout the day via the team chat so it’s just a different method of communication.

I do think that there will be a long-term impact from discovering that there are different working environments to enable productive outcomes for clients, although I don’t think this will be unique to financial services

What has been the impact of regulation on trading and what would you like to see more progress on?

I think it’s important to register the positive progress that has emerged from a heavy itinerary of regulation in recent years. The most recent consultations show a constructive dynamic between regulators and market participants but there is now a bit of regulation fatigue. Your perspective also changes when you go through such an unprecedented event such as this global pandemic and the attention turns to much bigger considerations such as the economy and the impact the pandemic will have on companies. Regulation equally has to change its context.

Aside from Covid-19, I think one of the challenges is how do you promote global co-ordination around regulatory practices at a time when the world is becoming more nationalistic. I also think more can be done with data transparency. This is not a new theme, and we have been talking about it for a long time, but it would be nice to see all the concerted focus on a consolidated tape come to fruition. It is impossible for this to stand as a commercial initiative so there needs to be support of a mandated utility mechanism.

In your session at the FIX EMEA trading conference – your panel discussed multi-asset trading evolution? What does it now mean and how are trading desks set up for it?

The organisation of a buyside trading desk often depends on the size of the fund management company. It is a function of scale and strategy. For example, if you have a big team then you can trade multi asset classes on the desk, split to inject a level of specialisation. If you are a small boutique manager or hedge fund, you may be required to trade cross assets as there isn’t sufficient trade flow in any single asset class. The distinction is often pragmatically applied as well. For example, derivatives may be traded alongside programs by equities traders who may also trade convertible bonds and ETFs.

At Invesco we trade a wide range of asset classes and have dedicated trading desks, but it is more about sharing market intelligence. I am not sure we will see a single team covering every instrument type, but I do think there will be greater automation and systematic trading across orders of bonds, FX and equities. Fixed income is different because the main execution channel is still RFQ (request for quote) although more recently portfolio trading has been widely taken up, which historically belonged to the equity world. Equally there is now single stock RFQ and ETFs being traded on order book so the distinctions are less clear. In general, I think the future structure of buyside dealing desks will be determined by tech solutions which will enable more research and data-driven execution recommendations, with people still making the ultimate decisions. It will be an evolution, but we are not there yet.

I know predicting the future is difficult especially now, but what do you see as the main challenges and opportunities?

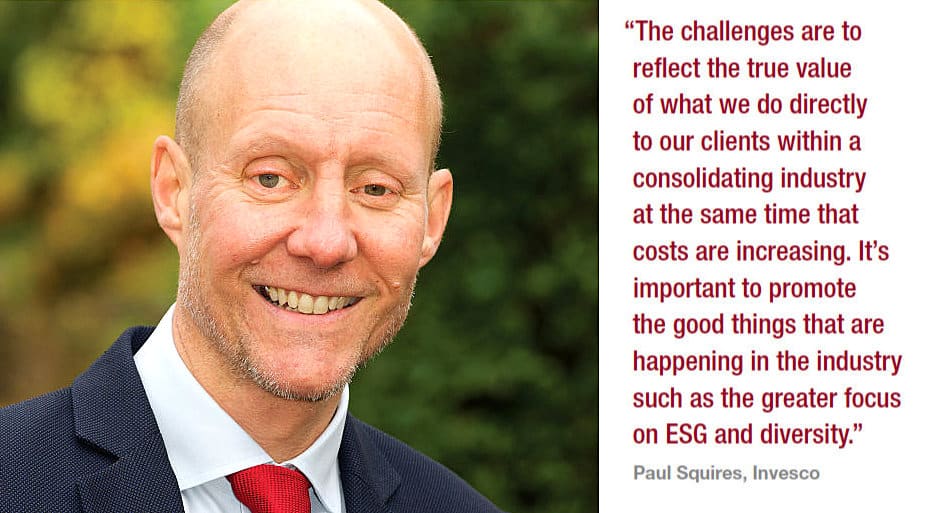

The challenges are to reflect the true value of what we do directly to our clients within a consolidating industry at the same time that costs are increasing. It’s important to promote the good things that are happening in the industry such as the greater focus on ESG and diversity. It presents both an opportunity and a challenge in how you embed ESG criteria in the investment decision making process.

From a cultural perspective, I also think it has been good that the industry is having serious discussions about mental health and wellbeing – just look at the recent proposals by AFME and the IA – to create an environment where talent is both drawn in and can thrive.

Biography:

Paul Squires is the Head of the EMEA Equities and Henley Fixed Interest dealing teams at Invesco. He joined Invesco in 2018 from AXA Investment Managers, where he was the Global Head of Trading and Securities Financing, overseeing a global team of over 70 professionals responsible for all dealing including equities, fixed Income, FX and money market securities.

Squires started his career as a UK equity dealer at Mercury Asset Managers in 1993 before joining Sun Life Investment Management (which later became AXA Investment Management) in 1996 where he went on to trade European equities and fixed income, setting up the London FI dealing desk.

Squires has been Co-Chair of the Investment Management Working Group of FIX, a non-executive Director of Smartpool and was a founding Director of PLATO (rejoining with Invesco in 2019). He has an honours degree in Business Economics from Reading University and holds both the SFA Registered representative dealing certificate and the Investment Management Certificate (IMC).

This interview was conducted by Lynn Strongin Dodds and is the cover article for the Autumn 2020 issue of Best Execution Magazine.

This interview was conducted by Lynn Strongin Dodds and is the cover article for the Autumn 2020 issue of Best Execution Magazine.

©BestExecution & The DESK 2020

©Markets Media Europe 2026