The new Treasuries protocols

Breaking away from the request-for-quote protocol could allow for tighter pricing without information leakage.

Traders engaged in the US Treasury (UST) markets face a growing range of execution options in 2018 with several new platform launches. BGC, Tradeweb and BrokerTec are all revealing new offerings in the next 12 months, each of which is expected to deliver new trading protocols to better reflect the way that both dealers and clients engage in execution. The elephant in the room is the potential impact of CME’s planned acquisition of Nex Group, including the interdealer BrokerTec’s US treasuries platform. Bringing the derivatives and cash markets together would be a powerful proposition.

These new developments are taking place in a market that has seen transparency thrust upon it in the form of the Trade Reporting and Compliance Engine (TRACE), which began reporting UST trades in July 2017. Faced with greater exposure of trading activity via TRACE, and seeing new trading protocols open up, traders may find themselves drawn to new ways of managing their market engagement.

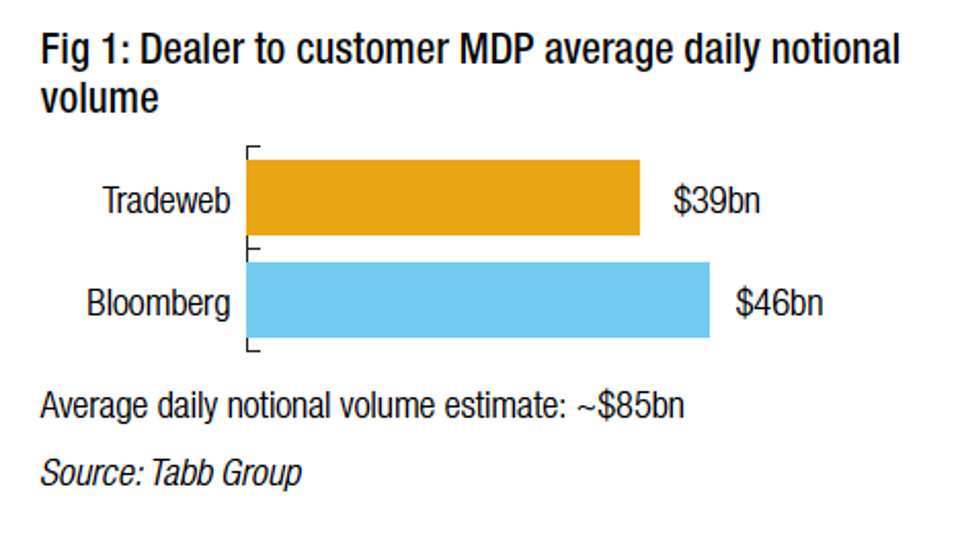

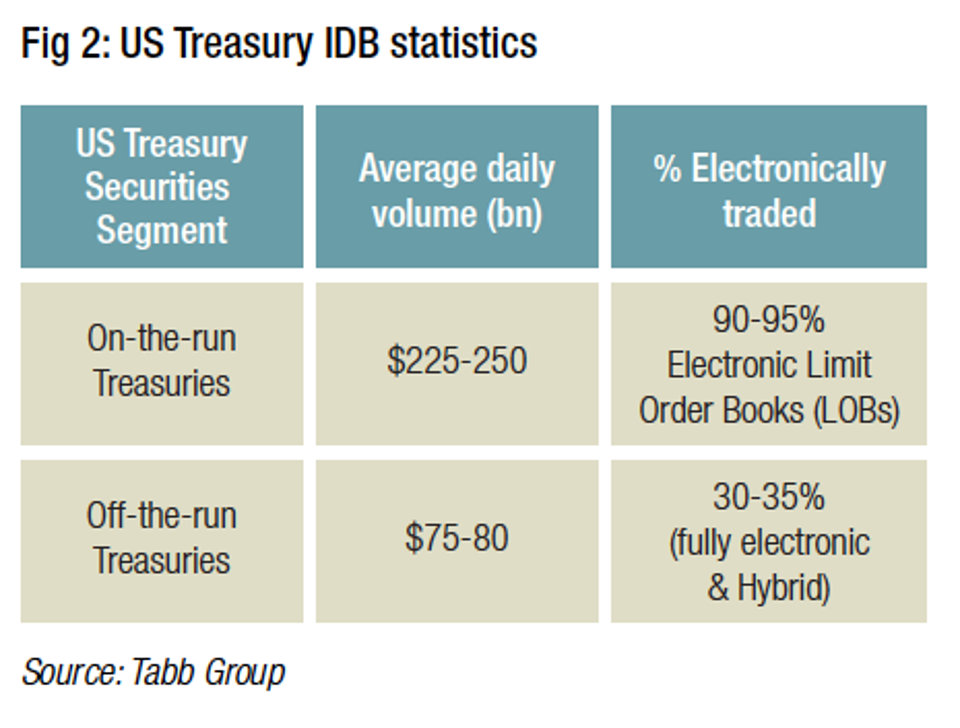

At present, the request-for-quote (RFQ) protocol is most commonly used, whilst central limit order books (CLOBs) drive dealer-to-dealer (D2D) trading (see Fig 1). Both buy- and sell-side side firms have adapted workarounds to try and overcome the limits of the existing models (see Fig 2).

At present, the request-for-quote (RFQ) protocol is most commonly used, whilst central limit order books (CLOBs) drive dealer-to-dealer (D2D) trading (see Fig 1). Both buy- and sell-side side firms have adapted workarounds to try and overcome the limits of the existing models (see Fig 2).

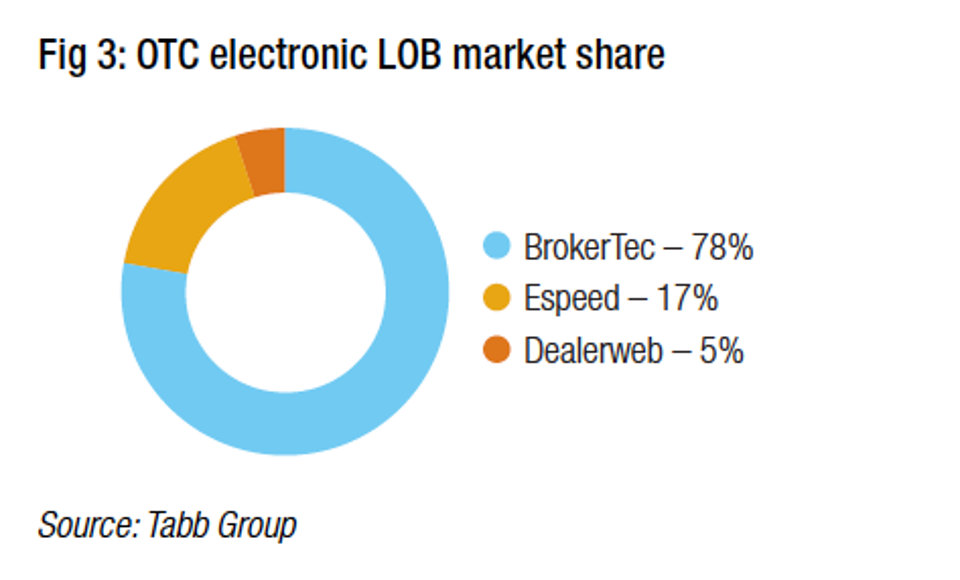

While the IDB market is dominated by Nex Group’s BrokerTec at present – research firm Tabb Group estimates it sees 75-80% of volume (see Fig 3) – the D2C market is more fragmented due to the prevalence of voice, bilateral trading, RFQ-based multi-dealer markets and electronic auto-quoting. Voice RFQ makes up around 55% of dealer average daily notional volume (ADV), platform-driven electronic RFQ is approximately 42% of dealer volume, and around 3% is conducted via ‘new protocols’, according to Tabb Group research.

“Several dealers are autoquoting up to substantial sizes,” says a senior rates trader at a tier one asset manager. “Over time our implementation of an automated RFQ execution protocol has become a significant portion of our workflow. We use rules-based trading processes so that a large portion of orders within our system in specific criteria can be automatically routed out to this auto RFQ model.”

Better access

Clients have the option of accessing liquidity directly from dealers through bilateral relationships and voice negotiation, via electronic multi-dealer platforms (MDP), which allow for an array of execution protocols and customisation, or dealer ATS and ATS-like trading portals.

Colby Jenkins, research analyst at Tabb Group, wrote in a December 2017 paper that the market is being pulled in two directions.

“In one scenario the market will evolve into an ultra-transparent, highly regulated equities-model, in which the buy side will eventually have full access to the interdealer CLOBs through a dealer, and transaction cost analysis (TCA) becomes a regulatory necessity,” he wrote. “Another direction is a market in the mould of an FX framework where participants on all sides will be interconnected through bilateral trading agreements, complimented by anonymous electronic communication network (ECN) liquidity.”

However, the new announcements are offering a wider range of execution options, in order to better serve the gap between RFQ and CLOB.

Chris Amen, head of US Treasury Central Limit Order Book Market at Tradeweb, says, “We are starting to see some fragmentation in the marketplace that could be better addressed by more direct channels of liquidity in a streaming protocol.”

New protocols

The platform launches are diverse. BGC Partners’ FENICS USTreasuries is launching in June, with a new block trading protocol that will allow dealers to provide prices to buy-side firms. With access to interdealer market pricing, buy-side participants are expected to see more competitive pricing of block trades, and from a wider pool of market participants.

“It’s an economically protected and beneficial system for the buy side and allows market makers to do what they do best, which is compete with each other for business but take care of institutional clients to ensure they get the service that they are used to,” says Howard Lutnick, CEO of BGC Partners.

The launch (see p.44) comes five years after parent interdealer broker BGC sold the treasuries market, eSpeed, to Nasdaq. The FENICS platform will also include a CLOB offering to support the more frequent, smaller orders typically traded by dealers and high-frequency trading (HFT) firms.

Tradeweb, which currently has a range of D2C and D2D execution options in the UST space is also expected to launch a new offering. The market operator is moving from the indicative pricing structure to a firm pricing architecture. At present this is expected to take the form of bilateral customised liquidity pools.

“The platform we are preparing to launch will take this approach to the next level,” says Amen. “We are helping market participants build alternative channels for liquidity where they can exchange risk on a high-quality basis, and without some of the execution risk that comes with trading in a central limit order book.”

It will offer a fully firm and executable streaming protocol to buy-side customers, allowing them access to liquidity with no last look to the dealer, with firm pricing the trader can agree upon directly.

Nex’s BrokerTec first began offering buy-side access to its interdealer model in 2016 via sponsored access, allowing firms to use their broker’s IDs to engage interdealer liquidity without disintermediating their dealers. However, it has not seen great success and the IDB is reviewing its offering, with a new planned launch in the first quarter of 2019.

“Buy-side clients are interested in the depth of liquidity in the interdealer market; they want a peek inside of that. We believe our indicative composite [price] at BrokerTec Direct will be the most accurate in the market because we are able to take in levels from traditional counterparties like primary dealers, levels from high-frequency trading firms, regional brokers, and a much broader range of counterparties, along with our own reference data,” says Nicole Shumpert, global head of BrokerTec Direct.

“Buy-side clients are interested in the depth of liquidity in the interdealer market; they want a peek inside of that. We believe our indicative composite [price] at BrokerTec Direct will be the most accurate in the market because we are able to take in levels from traditional counterparties like primary dealers, levels from high-frequency trading firms, regional brokers, and a much broader range of counterparties, along with our own reference data,” says Nicole Shumpert, global head of BrokerTec Direct.

She notes that “a lot of clients don’t have the ability to click to trade on a streaming price level – because of fiduciary responsibility – they are still using RFQ because they need to get three firms’ quotes back.”

“We will provide a mechanism by which they can capture the firm quotes they see in a streaming capacity,” she says. “We will work with them and their investment committees to deliver an acceptable solution.”

Shifting sands

The appetite for new protocols is clear. There are other elements in play. Regulation has played a role in pushing dealers away from the UST market and while there has been no liquidity problem, like those reported in credit, regulation has impacted the type of intermediation.

On 12 June 2017 the US Treasury recommended excluding US Treasuries as part of the supplementary leverage ratio calculation, part of the Basel III rules. Regulatory pressure on sell-side activity has hit second and third-tier banks hardest, according to Tabb’s Jenkins.

“The leverage ratio requirements and the emergence of high frequency trading (HFT) non-bank liquidity providers has increased the competitive landscape of a market that operates with very thin margins,” he wrote.

The market response to the Treasury’s 2017 announcement was seen as “freeing up bank balance sheets to intermediate more purchases of USTs,” according to a research note published by UBS strategist Chirag Mirani, and Seth Carpenter, an economist. They wrote that “In theory, if the proposal is adopted by regulators, the markets are right. However, in practice, even if the changes in regulations are ultimately approved, the changes will be a long time coming.”

As has been seen in the credit space, new platforms can find it hard to get traction. Getting the right balance of dealer, HFT, alternative and institutional buy-side liquidity in a working model that has critical mass is a tall order.

As Jenkins observed, “The bottom line is, whoever is able to provide access to natural liquidity via the most efficient trading ecosystem will succeed in the new treasury trading arena.”

©Markets Media Europe 2025

more valuable")