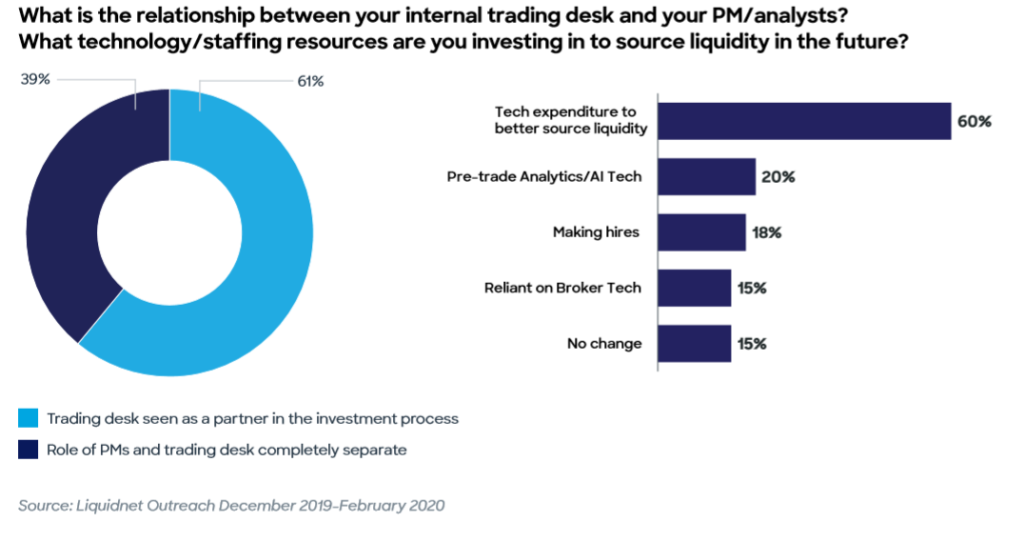

A new report by Liquidnet entitled ‘Unbundling Best Execution: What do traders need to know?’ has found that while most buy-side trading desks are now seen as a ‘partner’ in the investment process, a significant number are still perceived to be ‘trading support’ for portfolio managers (See Fig 1).

Trading is key to expressing investment strategies in the market, and plays a role in understanding both the liquidity of assets and their pricing. The inability to price a portfolio can lead to shuttering of a fund as its net asset value is calculated. In recent market volatility several Nordic funds struggled with this issue.

European regulators enforced a separation of payment for trading and investment research via the Markets in Financial Instruments Directive II (MiFID II) which came into effect in January 2018.

In the US, the stance from market regulator the Securities and Exchange Commission (SEC) towards payment for research had had hindered asset managers looking to unbundle it from execution costs.

In its report, authored by Rebecca Healey, head of market structure and strategy, Charlotte Decuyper and Lara Jacobs from the EMEA market structure and strategy team at Liquidnet, the firm noted: “Despite Section 28(e) of the US Securities Exchange Act of 1934 enabling investment advisors to obtain research financed through commission sharing arrangements, in practice several bulge bracket firms still looked to receive payment for research in trading flow. This can inhibit optimal execution even when using a client commission agreement (CCA), as firms can only switch trading counterparties once research bills have been paid.”

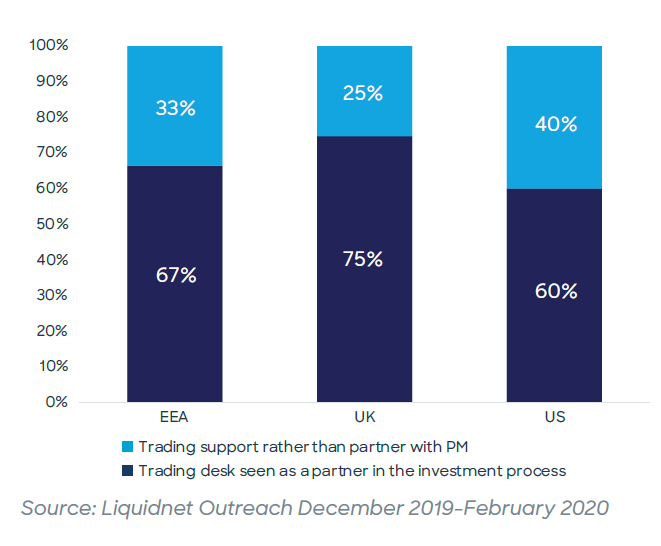

While 75% of trading desks are seen as partners in the investment process within the UK, that reduces to 67% in Europe more widely, and is lowest in the US, where just over half (60%) are seen as adding value in this way.

Regulators in the US have been keen to allow buy-side firms to separate payments out where they wished to, in part because it created less transparency for end investors who used asset managers across the US and Europe, with the potential for execution costs to only be visible in the latter.

“In November 2019, the SEC issued an extension of its October 2017, Temporary No Action Letter to July 2023, stating that the use of CCAs does not impact the broker-dealer exclusion in connection with payment for research under Section 28(e),” Liquidnet notes.

By separating execution service payments from the provision of research, end investors can be clear about where their money is being spent on research and trading, and when the asset manager is paying for those costs. From a trading perspective, having a separate execution cost allows the trading desk to focus on execution quality on a trade-by-trade basis and to adjust executing broker lists based on performance rather than the support provided to portfolio managers via research and corporate access.

“The ability to extract, analyse, store, and feedback historical execution data not only enable firms to support execution decisions but also provides an audit trail of which broker performed well, ensuring optimal future selection of brokers,” Liquidnet said.

©Markets Media Europe 2025

more valuable")