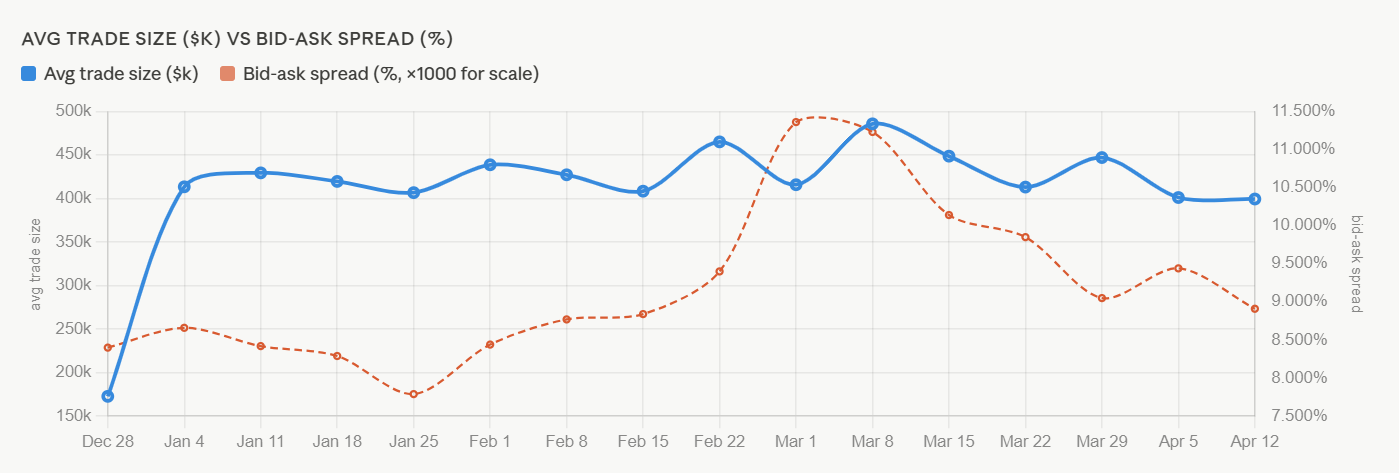

The latest data from MarketAxess’s TraX data tool, which follows activity across multiple marketplaces, and its CP+ pricing tool, show that US markets, particularly US investment grade, are reaping the benefits of a deeply electronic, all-to-all marketplace.

When stress hit this year at the start of the Iran war, bid-ask spreads widened as dealers repriced liquidity, but volumes held firm and average trade sizes rose. That is the signature of a market where liquidity doesn’t depend on any single dealer relationship. Participants can find the other side of a trade through request-for-quote protocols, anonymous platforms, and portfolio trading without needing a bilateral dealer commitment. The market might clear trades at a higher price, but it does clear them.

US IG market comparison

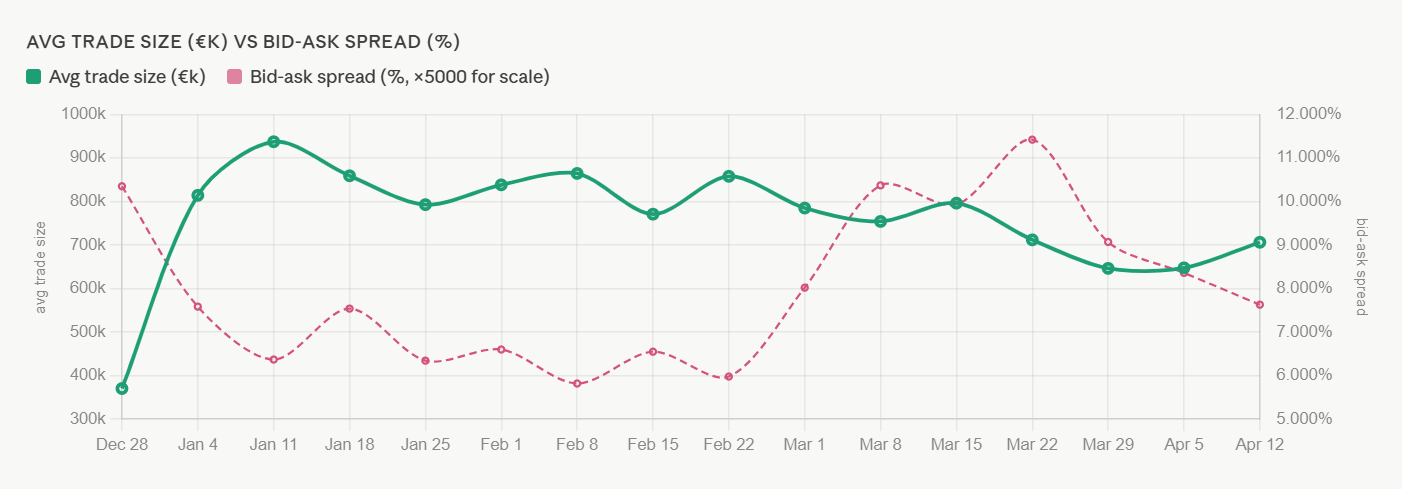

European markets, especially European IG, show the opposite pattern. Looking at activity this year, sizes compressed and activity fragmented under stress. That is more consistent with a market that still relies heavily on voice and relationship-based dealing, where the dealer’s willingness to commit balance sheet is a binding constraint. That means when dealers pull back, buy-side traders don’t just pay more, they trade less and in smaller clips.

European IG market comparison

The average trade size differential is telling in this respect. US IG averages around US$420k per trade, while European IG averages about €830k, which is roughly double. This seems counterintuitive if you expect electronic markets to facilitate smaller, more frequent trades, but it makes sense in the modern context of bond trading.

In fact, US IG’s high electronification has enabled electronic portfolio trading and aggregation protocols to flourish, which allow institutional orders to be executed simultaneously. The result is a high trade count at moderate average sizes without substantially increasing the typical risks for a dealer on the other side of a trade.

European IG’s relatively larger average sizes reflect a market that still pushes larger clips through fewer, more deliberate block trades, so when those relationships become strained and dealers reduce the risk they are prepared to carry, the average ticket size shrinks. Anecdotally we also hear that e-trading on the continent is more characterised by orders that are sent to many dealers, making the risk of trading against a client higher for a market maker.

This data arguably shows is that electronic trading in the US has changed the resilience profile of the market under stress by changing how the bonds are traded. The US IG market absorbed a significant macro shock through the opening of the Iran war without a liquidity availability crisis. The European markets, operating with lower electronic penetration, experienced a more traditional stress pattern where cost and availability moved together.

The caveat is that electronification is not a silver bullet. A massive shock to the risk appetite of electronic market-makers could produce a very fast and correlated withdrawal, like in March 2020, which demonstrated even electronic markets can seize up if the stress is large enough.

©Markets Media Europe 2025

more valuable")