By Tom Harry

By Tom Harry

SFTR reporting obligations are fast approaching. The first wave of reporting under the Securities Financing Transactions Regulation (SFTR) is set to commence in April 2020. Repo market participants must now prepare for the most significant regulatory change since the introduction of MiFID II.

Participants will be required to report their repo and other securities financing transactions to a trade repository, such as UnaVista, by T+1. The action market participants take over the coming months will make or break their ability to hit the ground running in April next year.

With the countdown to SFTR reporting well underway, market participants are making it a priority to understand which fields need to be reported, where they can find those fields and how they will deliver them to their trade repository.

What are the challenges?

SFTR reporting presents significant challenges to the repo market. Up to 155 fields will be reportable in a specific format for trades, collateral updates and reuse for repo and other securities financing transactions. In most cases both sides of the trade must be reported to a trade repository. Where the two sets of data sent to the repository do not match, counterparties should look to reconcile inconsistencies.

Many market participants see their trading activity fragmented across different manual workflows, including phone, email and chat systems, particularly in the dealer-to-client space. These manual workflows present greater risks of human error and discrepancies in what the counterparties report. These risks are further compounded by data often being recorded inconsistently across different systems.

In the SFTR world, maintaining these manual workflows will require a significant uplift and on-going effort in order to capture, format and submit the required data. This will be a hugely time-consuming task that distracts individuals away from their core trading focus, ultimately impacting their performance and profitability.

In the SFTR world, maintaining these manual workflows will require a significant uplift and on-going effort in order to capture, format and submit the required data. This will be a hugely time-consuming task that distracts individuals away from their core trading focus, ultimately impacting their performance and profitability.

SFTR reports also demand extensive reference data, for stakeholders and collateral.

Up to twenty fields require LEI codes to identify various institutions, including not just the counterparties but also CCPs, clearing members, custodians, tri-party agents and brokers. Where a bond is used as collateral, for example, reporting counterparties will be required to report several reference data points in relation to that bond. This includes the bond’s CFI code, the issuer’s LEI and country code and the collateral quality. Market participants will have to source and maintain these reference data points in order to report correctly.

Meanwhile, sell-side firms will face the additional challenge of dealing with requests from their buy-side clients to handle SFTR reporting on their behalf. This could become a key differentiator for buy-side firms when choosing their sell-side counterparties. The inability to support their clients with SFTR reporting could mean losing repo business to a better-equipped competitor.

UK-based institutions will also have to consider the outcome of the Brexit negotiations. Market participants may have to consider whether they need to report under the EU SFTR, UK SFTR or potentially both.

The solution: go electronic

Electronic trading is the way forward for market participants to streamline their workflows ahead of SFTR reporting. Electronic matching and confirmations ensure a single and consistent source of trade data for both counterparties. It also offers greater scope for market participants to automate processes, reducing the need for human intervention and freeing up resources to focus on value-added activities.

MTS enhances this proposition further by bringing together both the interdealer and dealer-to-client repo markets in a single platform. Market participants can leverage the MTS Repo platform’s rich suite of order book, RFQ and trade registration functionalities to trade specific and general collateral and triparty baskets on MTS’s regulated trading venues. This is complemented by full STP, including FIX connectivity, for trade capture and extensive links to CCPs and CSDs for automated clearing and settlement.

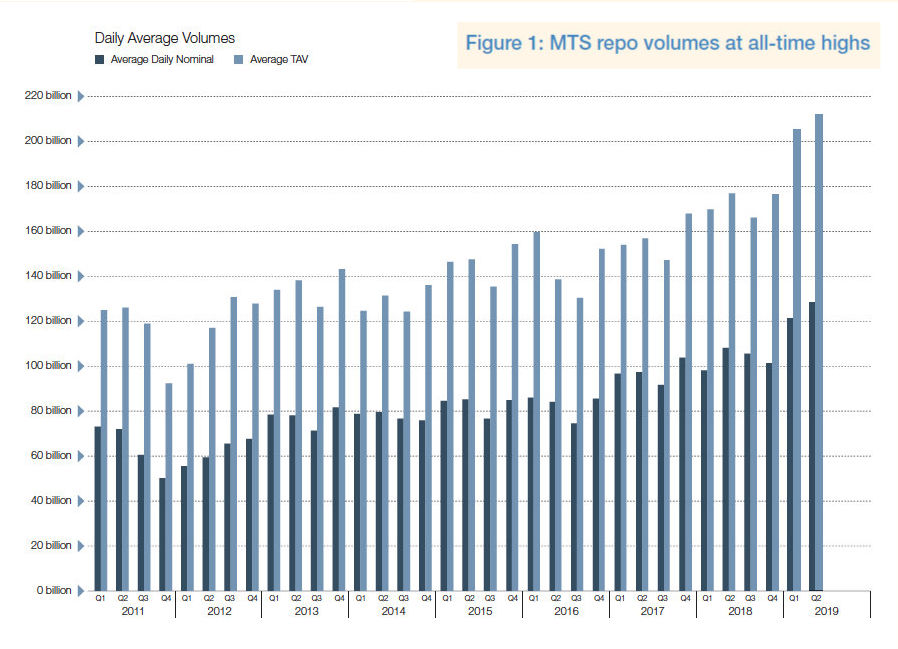

Market participants are capitalising on the clear advantages presented by electronic repo trading. Average daily volumes (ADV) on BondVision Repo, the dealer-to-client segment, are up 300% year-on-year. MTS Repo trading venues overall have set an all-time record for on-screen ADV of EUR 133bn for 2019 H1.

One stop shop: the SFTR Blotter and beyond

In the run up to SFTR implementation, MTS has worked with a diverse group of industry stakeholders, including CCPs, industry groups and other vendors. We have identified a clear need from market participants for greater standardisation of trade messages to streamline SFTR implementation.

In response, MTS has developed a purpose-built product: the SFTR Blotter.

The SFTR Blotter has been designed to give market participants a head-start in implementing their SFTR reporting processes. Trades are automatically mapped to the SFTR fields and formats and enriched with master agreements, collateral reference data and UTIs. The SFTR Blotter is made available in real time via API and to auto-export from the MTS GUI, with the additional option to send securely to third-party services.

The SFTR Blotter has been designed to give market participants a head-start in implementing their SFTR reporting processes. Trades are automatically mapped to the SFTR fields and formats and enriched with master agreements, collateral reference data and UTIs. The SFTR Blotter is made available in real time via API and to auto-export from the MTS GUI, with the additional option to send securely to third-party services.

As a result, both buy-side and sell-side firms will be able to leverage the SFTR Blotter service to accelerate their implementation process. Its flexibility will also allow sell-side firms to support their clients. Buy-side firms can permission their sell-side counterparties to receive the SFTR Blotter on their behalf to support their SFTR reporting.

MTS is also working with UnaVista to offer an Assisted Reporting service as part of an end‑to‑end reporting solution. MTS will be able to send reports to UnaVista, allowing clients to review their reports prior to submission to the trade repository.

More data and greater efficiencies

The move to electronic platforms like MTS Repo is an opportunity to drive automation across the repo market, improving overall market efficiency.

The requirement to report repo activities in a standardised and aggregated manner raises an exciting prospect: a rich source of ‘Big Data’ for repo. This promises the opportunity to develop new analytics and insights to inform decision making in the front office.

By moving repo trading onto the MTS Repo platform, market participants can position themselves today for the brave new SFTR world. In turn, this will enable market participants to focus on what they do best: their repo business.

Tom Harry is Product Manager at MTS, focusing on regulatory solutions for the interdealer and dealer-to-client repo and cash bond markets.

©Markets Media Europe 2026

more valuable")