We reveal the buy side’s use of platforms for pre-trade data, executing orders in the market and trading venues.

Trading Intentions Survey highlights

- Bloomberg has the largest number of users for pre-trade data, trading interface (messaging) and trading venue.

- MarketAxess is the most effective platform at finding liquidity. Bloomberg, Tradeweb, Liquidnet and Neptune are all highly rated.

- Amongst O/EMS tools, Bloomberg has the most users. Charles River and BlackRock Aladdin have the highest proportions of major users relative to overall – 100% of BlackRock Aladdin traders are major users. Flextrade has the greatest pipeline of new business.

- Amongst venues, Liquidnet and MarketAxess have the highest proportion of all-to-all trading; Bloomberg and UBS Bond Port have the highest proportion of click-to-trade.

- Despite dealer streamed prices being a popular pre-trade pricing tool, execution against them is low.

New in 2020

- New potential tools for finding liquidity include Bondcliq, Ediphy, Katana, streamed dealer prices and Symphony SPARC.

- This year breakdown is by pre-trade data sources; trading interfaces including EMSs and OMSs; and trading venues.

- Preferred trading protocols on each venue are analysed across total respondents and across confirmed users of each platform.

- As the sample size nearly doubled this year, we saw a drop in users of 6.5% on average across platforms, bar Bloomberg, reflecting a wider geographical distribution.

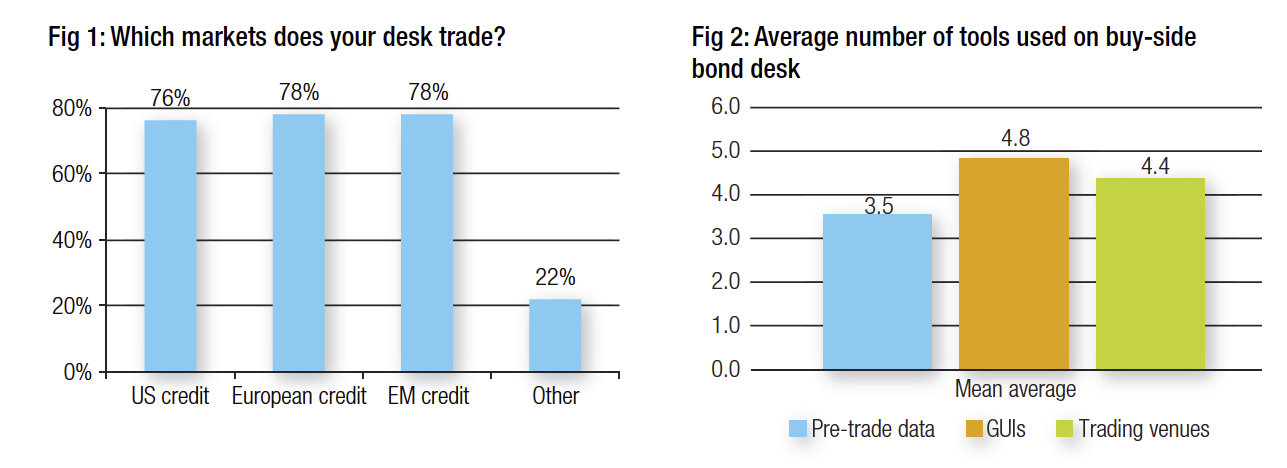

We spoke to the corporate bond trading operations at 55 major asset managers in Europe, US and Asia Pacific (see Fig 1).

On both modal and mean average they typically used four pre-trade data sources (ranging between 1 and 7), five trading interfaces (between 1 and 9 on their screens) and used four trading venues (typically between 2 and 8) to execute trades (see Fig 2).

Traders dealing only in US and/or EM credit had fewer pre-trade data sources (averaging two) than those also trading European bonds, and traders only in Europe and/or EM used a slightly higher number of trading venues (averaging five) than those who traded in the US market.

Of those using a single pre-trade source of information the majority used Bloomberg, but streamed dealer prices and ‘human effort’ were also cited. Those using only a single graphical user interface (GUI) – whether an order or execution management system (O/EMS) or platform GUI – to access markets had no consistent favourite. Most traders had one O/EMS and then one or more direct interfaces into trading venues. Only one trader said they used a single venue to execute – most used two or more.

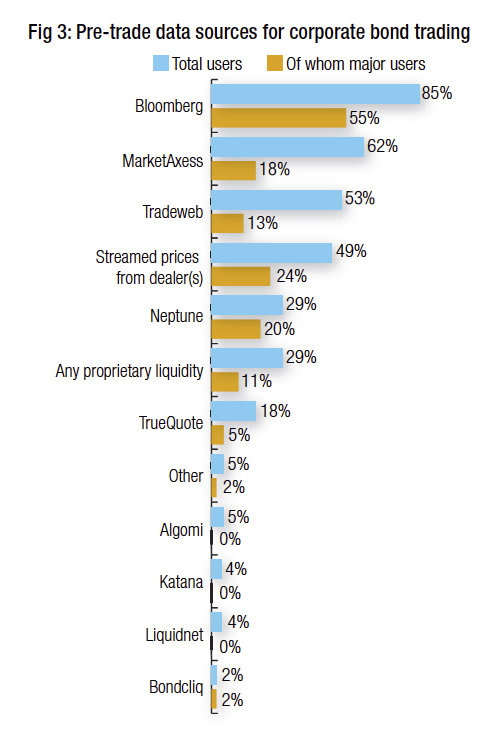

Pre-trade data sources

Bloomberg dominated this category acting as a pre-trade data source for 85% of traders with 55% of those being major users (see Fig 3). MarketAxess, which carries the Trax data and offers the Composite Plus (CP+) tool was used by a total of 62%, with 18% being major users and 44% being users of its data. Tradeweb was used by a total 53% of traders as a pre-trade data source.

Data streamed directly from dealers was also popular with 24% of traders being major users of it, although Neptune’s offering which standardises dealer data has clearly won favour, with most of its users being ‘major users’ (20% of all respondents).

TrueQuote has successfully built on its gains of 2019, with 18% of users citing it as a pre-trade source, and 5% as a major source. Algomi has a 5% user base, while new tools such as Katana (4%) and Bondcliq (2%) are starting to make inroads. The closure of B2Scan in 2019 may have led to new opportunities for some providers.

One missing element may be that of other trading venues; Liquidnet, UBS Bond Port, MTS and Trumid were not initially included as choices in this section but were mentioned by traders, so their role may be under-reported.

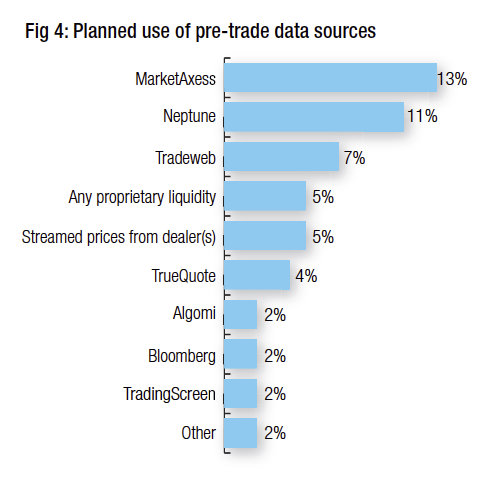

The pipeline for new business for pre-trade data sources (Fig 4) is looking most positive for MarketAxess and Neptune, both who have double figure percentage of traders planning to use them. Tradeweb also has a positive line of growth in this space.

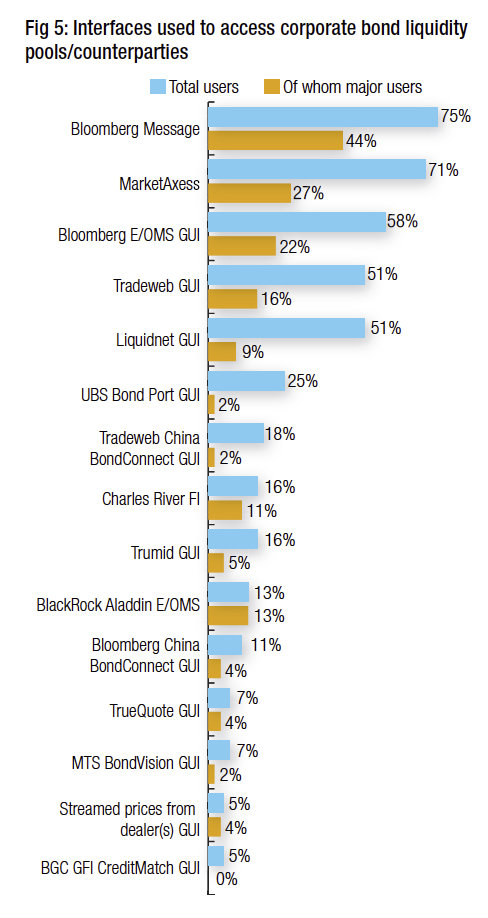

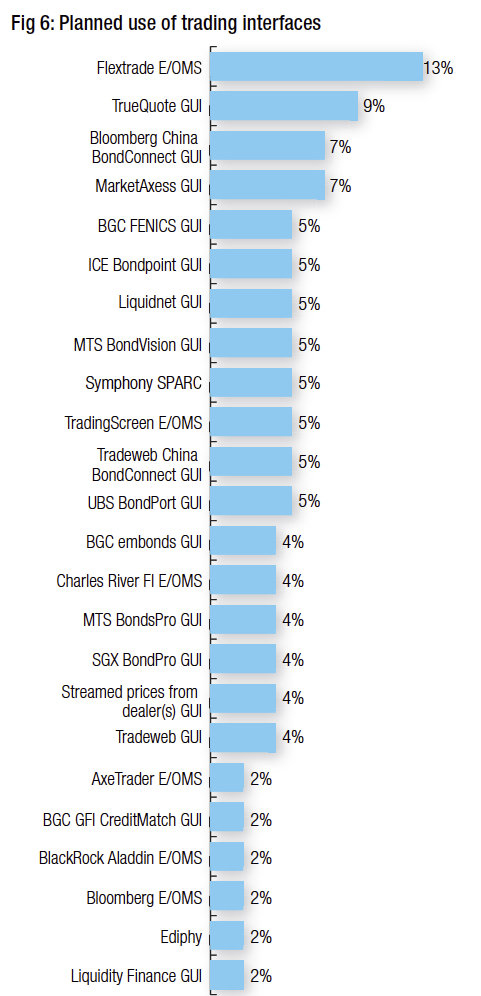

GUIs, order and execution management systems (O/EMSs)

The over-the-counter nature of the corporate bond market is apparent in the choice of interface for exchanging order information. Bloomberg messaging tools are used by 75% of traders and 44% consider themselves major users (see Fig 5).

The next most used interfaces are those of trading venues themselves. MarketAxess has the most popular graphical user interface (GUI), used by 71% of traders with over a quarter (27%) marking themselves as major users. Both Liquidnet and Tradeweb’s GUIs are used by 51% of traders, although Tradeweb’s has more ‘major users’ (16%). Tradeweb has also had good success moving into China with 18% using its China BondConnect GUI against Bloomberg’s 11% for its China interface.

Of the other platforms, UBS Bond Port and Trumid are both performing well as interfaces into the market with 25% and 16% of traders respectively using them.

Amongst the O/EMS offerings, Bloomberg is again dominant with 22% of traders as major users out of a total 58%. Charles River has 17% of traders, 11% being major users while BlackRock Aladdin has 13%, all of whom are major users.

Although it did not figure highly in use to date, Flextrade had the greatest pipeline with 13% of traders planning to use it. TrueQuote’s interface is expected to be used by another 9% of traders while both Bloomberg’s China BondConnect interface and MarketAxess have 7% of traders expecting to use their interfaces.

Trading venues

The big four market operators for fixed income have consistently been Bloomberg, MarketAxess, Tradeweb and Liquidnet, with UBS Bond Port in fifth place. TrueQuote and Trumid have maintained solid positions, the former having rocketed in use last year, the latter having seen considerable trading volume growth over the last six months, and increased sell-side support.

This year Bloomberg overtook MarketAxess as the leader from 2019, increasing its total users to 84% (up from 76% last year), while MarketAxess saw its total users drop slightly from 83% in 2019 to 80% this year.

There was a general decline of total users across platforms, averaging 6.5 percentage points, and a decline in the number of users classifying themselves as ‘major users’. This is potentially representative of the larger sample size this year (nearly double that of 2019), which captured a larger number of buy-side desks that only traded across one or two of the three possible markets (Europe/US/EM) and therefore had more varied execution goals.

The most significant growth story in venues is Tradeweb’s China BondConnect tool, which had no users as of last year and was expected to be used by 14%, but is being used by nearly a quarter (24%) of traders.

Perhaps not coincidentally, Bloomberg China BondConnect has one of the largest proportions of traders planning to use it, with 10% in the pipeline. TrueQuote Volumematch has 9% of traders on its books, suggesting that the firm could leverage its success in the internal crossing space to broader execution choices.

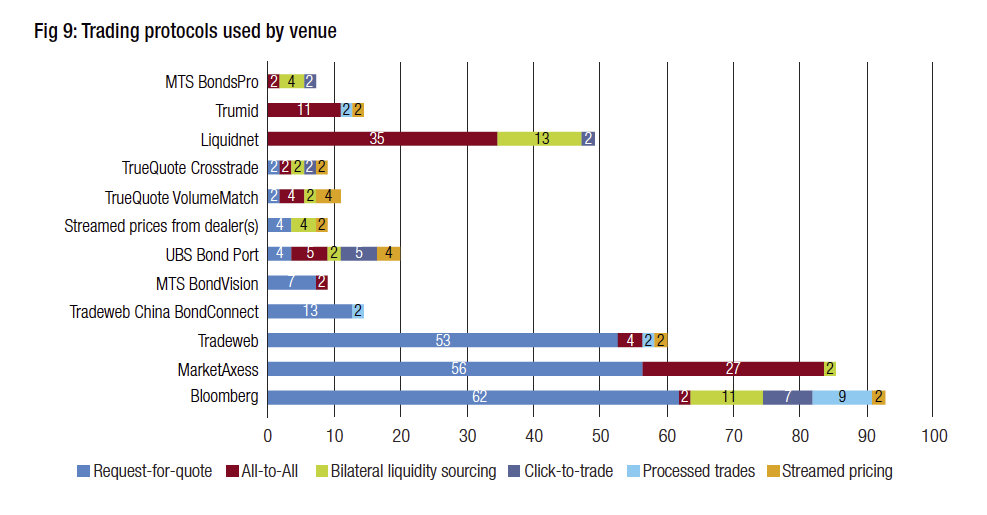

Most trading is conducted via the request-for-quote (RFQ) protocol, with Bloomberg, MarketAxess and Tradeweb leading the field (Fig 9), but analysis of trading types shows some interesting differences between venues. Liquidnet, MarketAxess and Trumid are the leaders in all‑to‑all trading.

(measured as percentage of respondents)

(measured as percentage of respondents)

Bloomberg, UBS Bond Port, TrueQuote, and MTS show the highest levels of diversity in protocols used. Bloomberg has the highest proportion of ‘click-to-trade’ execution. Bloomberg also has the highest proportion of processed trades amongst traders, followed by UBS Bond Port. We have profiled the main platforms to analyse execution even further.

Overall performance

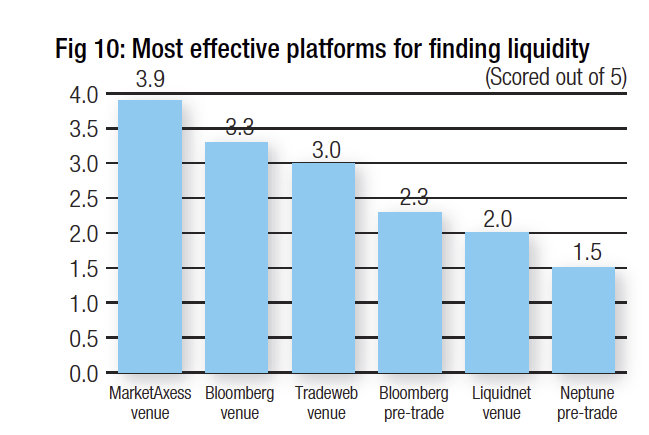

When considering the effectiveness of all tools in finding liquidity, buy-side traders identify the three major trading venues – MarketAxess, Bloomberg and Tradeweb – as the best three tools in that order (see Fig 10), with Liquidnet in the top five, and Neptune as one of the top six providers.

Separating Bloomberg into its data element and trading venue, we see its venue is perceived as more effective at facilitating liquidity than its pre-trade data source, but nevertheless its use as a pre-trade data source is the fourth most effective source for finding liquidity, according to respondents.

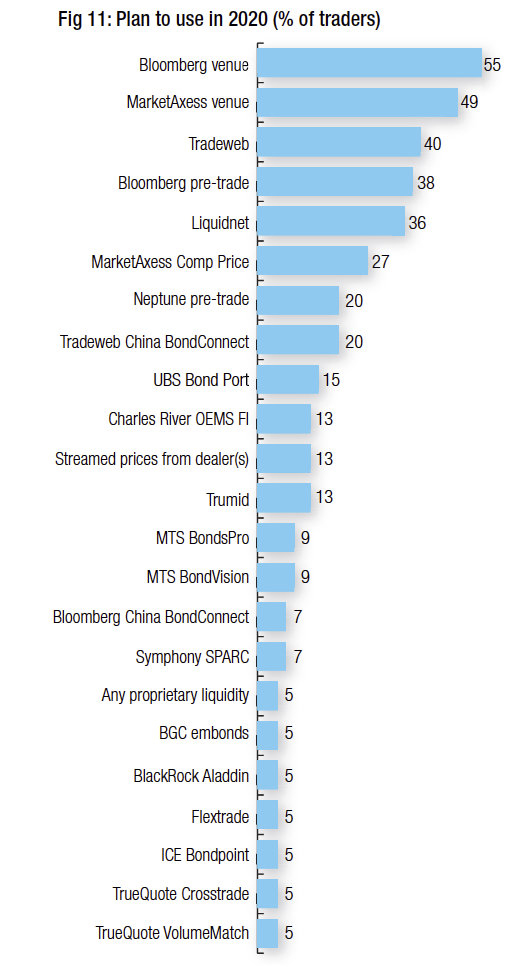

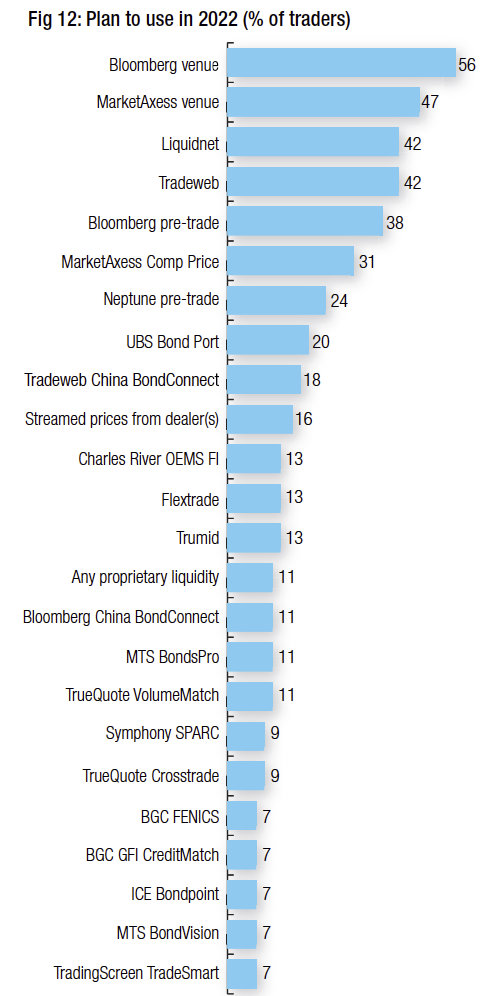

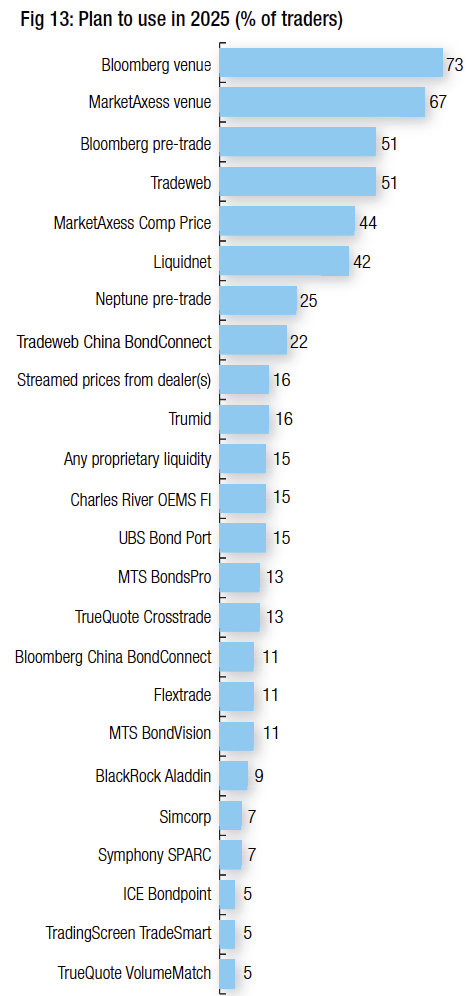

Looking at future confidence over the next year (Fig 11), two years (Fig 12) and five years (Fig 13) largely mirrors current usage patterns, with the big three represented in the same order as they are today, albeit with occasional ties for third place. With MarketAxess’s CP+ tool marked separately to the trading venue, it ranks highly against other tools.

Other consistently supported platforms are Liquidnet, which ranks highly and in 2022 is rated as joint third in likely usage, Trumid, TrueQuote, and UBS Bond Port who all see solid expectations of support over the next few years. The MTS platforms and Bloomberg China BondConnect show consistent growth as time goes on.

Some highlights in this assessment are Flextrade, whose strong pipeline of users this year is also reflected in the confidence over the medium- to long-term, with 11% of traders expecting to be using it by 2025. For a platform that does not have a significant number of users today, that is notable; by contrast rival BlackRock Aladdin has mid-to-high single figures amongst the survey respondents expecting to use it in the future in all three timeframes. Also of note is Symphony SPARC, the new trading protocol being launched for credit and a new entrant, shows reasonable interest.

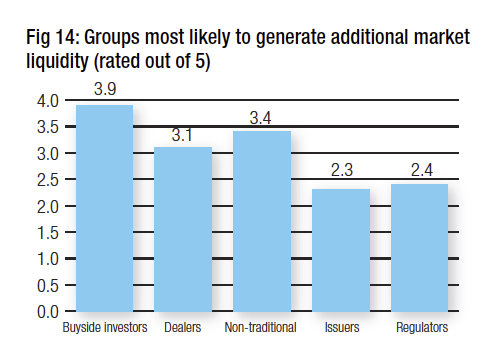

Outside of the platform space, non-traditional liquidity providers are increasingly expected to be a generator of new liquidity (see Fig 14), having increased their score year-on-year, putting them just behind buy-side firms – consistently voted the most likely source of new liquidity – for the first time. Dealers and buy-side investors are seen as less likely to make a change that generates additional liquidity this year, while confidence continues to grow that issuers and regulators may have a positive impact.

©The DESK 2020

©Markets Media Europe 2026

more valuable")