Across almost every market spreads tightened over the past last week, looking at Morgan Stanley data, reflecting an apparently synchronised shift in investor sentiment.

When spreads tighten and interest rates rally simultaneously, total returns become attractive, which can reinforce investor engagement. Primary markets activity supports this. There was US$63 billion in primary market supply priced in the last week for US investment grade bonds taking the total to +30% year on year. Issuers would not bring that volume unless they had confidence that demand existed, and the fact that spreads still tightened despite the increased supply suggests that demand absorption was more than sufficient and supports evidence of genuine appetite. Weekly issuance reached US$15 billion and US$9 billion across HY and loans, respectively with Morgan Stanley estimating total at US$102 billion which is 45% YoY in HY and US$120 billion which is down 17% YoY in loans.

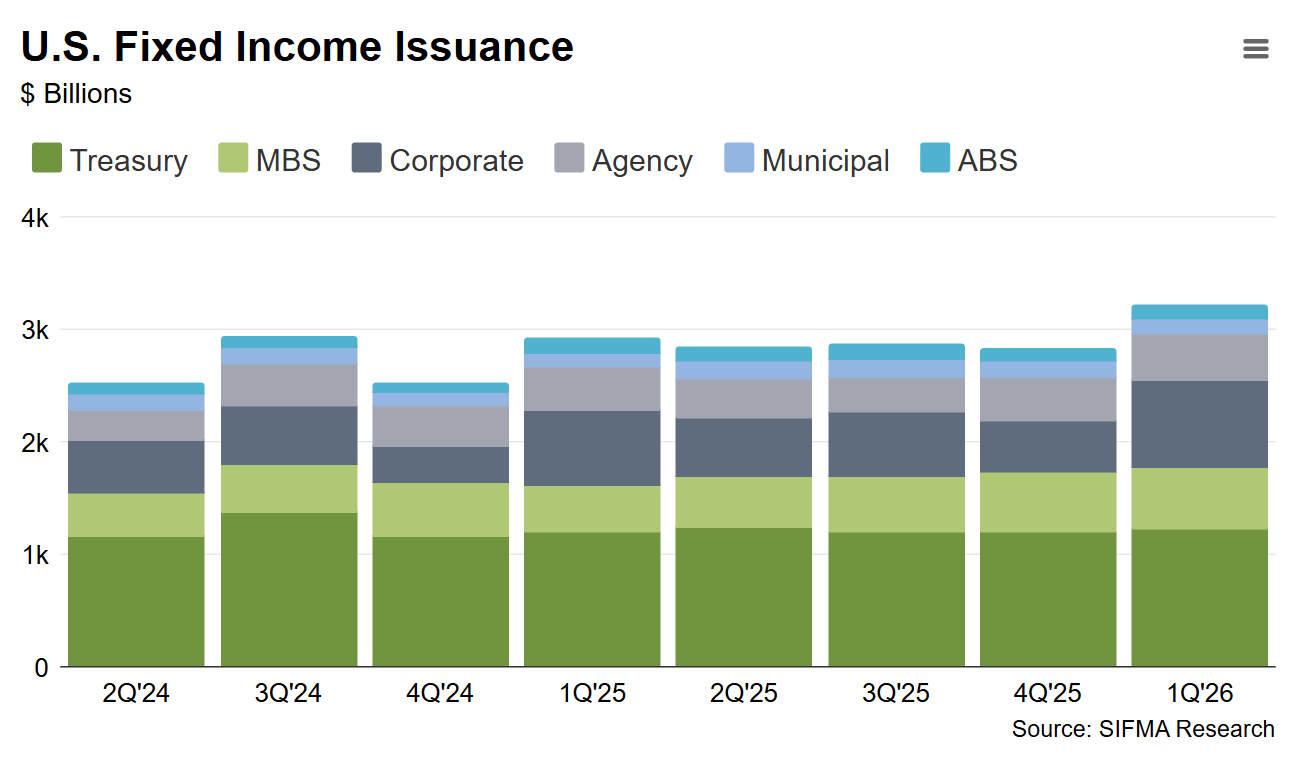

SIFMA noted that overall fixed income issuance in the US was US$3.2 trillion for the first quarter, up 13.7% quarter-on-quarter and 10.3% year-on-year.

“This was the first quarter where issuance exceeded US$3 trillion since 4Q21, with five out of six covered asset classes posting quarterly increases,” it wrote. “High levels of long-tern UST issuance continued at $1.2 trillion, marking the seventh consecutive quarter with issuance above US$1 trillion. Corporate issuance, is US$775.2 billion net which is up 70.3% Q/Q, and 15.6% YoY which is the largest quarterly total since Q2 2020.

The March stress suffered as a result of the Iran war was a trough in sentiment, but the US recovery which was faster and more consistent than Europe which has seen five weeks of IG outflows and YTD in HY are still negative, reflecting the region’s greater fragility and dependence on the macro backdrop.

Meanwhile, corporates have been aggressively taking advantage of investor appetite to issue debt. If that appetite were to reverse, the pipeline of supply would become a headwind very quickly, something worth watching in the US and Europe as the recovery continues but peace talks falter.

©Markets Media Europe 2026

more valuable")