Automated trading and derivatives are changing the way US Treasuries are traded, exposing the buy side to high-frequency trading strategies. Chris Hall reports.

If big is beautiful, then US Treasuries is probably the most beautiful financial market in the world. Demand is diverse; supply is abundant. Average daily volume is north of US$500 billion, and new issuance has boosted the market at a rate of US$2 trillion per annum since 2009. But, big can be slow to change. It can also hide a multitude of sins.

October 2014’s flash event – during which 10-year US Treasuries oscillated in an alarming 37 basis point (bp) trading range – gave a fleeting glimpse into possible problems arising from the shift of liquidity provision from the market’s 22 primary dealers to a new generation of high-tech, high-speed proprietary trading firms (PTFs). Fears were raised about the systemic risks of relying on liquidity from lightly-regulated sources, but surprisingly little has changed since. For example, regulators have reported self-trading reaching levels of up to 15% of daily volume in dealer-to-dealer (D2D) markets, but have failed to investigate whether that might constitute manipulation.

The status quo has been shored up by a surfeit of liquidity and a prolonged absence of price volatility, stemming from US Treasuries’ status as the central banking world’s favourite reserve instrument in the era of quantitative easing. In February 2018, the Federal Reserve held US$2.4 trillion of Treasuries, with foreign central banks holding approximately US$3.1 trillion.

Yet heavyweight investors say that fixed income traders at buy-side firms face the same challenges in the US Treasuries market today as their equity trading counterparts did in the late 2000s; tempted to reveal their hand by attractive pricing levels posted by high-frequency traders (HFTs) / PTFs on electronic central limit order books (CLOBs), only to see ‘bait’ liquidity disappear in a flash. Once hooked, the outmanoeuvred buy-sider is left to complete orders with bids posted at higher prices by nimbler algorithms.

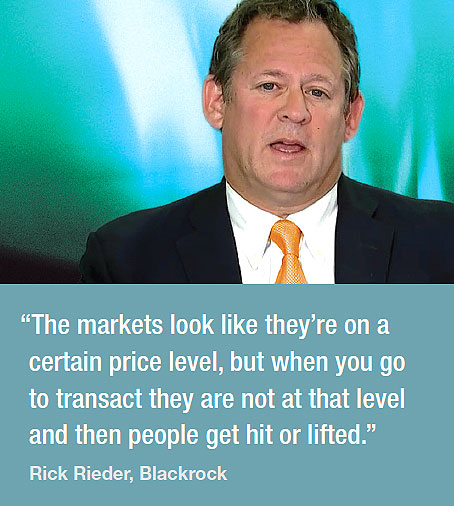

Last November, Rick Rieder, global fixed income chief investment officer at Blackrock, suggested the market was increasingly bifurcated between small electronically traded orders and larger voice-traded deals.

Last November, Rick Rieder, global fixed income chief investment officer at Blackrock, suggested the market was increasingly bifurcated between small electronically traded orders and larger voice-traded deals.

He said, “The markets look like they’re on a certain price level, but when you go to transact they are not at that level and then people get hit or lifted and then try and unwind their risk; you can create a staircase dynamic as people are trying to get out of their risk in smaller size.”

Speaking alongside Rieder at the Fed’s Annual Conference on the Evolving Structure of the US Treasury Market, David Tepper, co-founder of US$14 billion AUM hedge fund Appaloosa Management, noted the need for avoidance strategies.

“There is an extra cost to it, but there is always a way to fool the machines,” he said. “Markets are liquid; the futures markets are fantastically liquid. Any day you want to move around billions of dollars you can do it.”

Matthew Scott, a New York-based fixed income trader at AllianceBernstein, confirms the role of US Treasury futures in helping buy-side portfolio managers and traders achieve their objectives, noting, “Futures volumes as a percentage of cash volumes are 90% plus now, up from 50-55% just five years ago.”

Dissatisfaction with RFQ

On the buy side, CLOB-based electronic trading of US Treasuries remains a minority activity, with appetite dulled by the increasing availability of alternatives. In the ‘2017 Market Structure & Trading Technology Study’ by Greenwich Associates, 95% of buy-side traders said they do not currently trade on-the-run US Treasuries i.e. highly liquid recent benchmark issues, on CLOBs, with only 16% believing that doing so would improve execution quality.

With almost 90% of traders happily trading on-the-run Treasuries in sizes up to US$15 million via voice or electronic multi-dealer RFQ, the compliance, technology, execution and relationship challenges of CLOB trading would appear to comprise comprehensive disincentives.

And yet, there are signs that the buy side is not satisfied with traditional RFQ, in part because it does not provide the same kind of clear demonstration of best execution achieved in order-driven markets.

At a time when MiFID II is raising regulatory and stakeholder expectations on execution quality, simply sourcing quotes from five relationship banks falls short. In parallel, increased availability of trade data (FINRA-regulated firms started reporting US Treasury trades to TRACE in July 2017) is enabling buy-side traders to conduct more granular analyses, while continuing to pursue cost-efficiencies through further automation.

“Client demand continues to increase for new solutions that leverage their data more efficiently and effectively in advancing their overall trading performance,” observes Colm Murtagh, head of US Rates at trading platform operator Tradeweb, which now enables buy-side clients to automate low-touch US Treasuries trades, using a range of data-driven parameters to streamline and refine the RFQ process.

Although Tabb Group estimated in its report ‘New World, New Tools: US Treasury Trading’ that RFQ still accounts for 97% of volume executed by large dealers with buy-side clients, analyst Colby Jenkins predicts traders will increasingly use detailed metrics to carefully select counterparties, protocols and channels for US Treasuries trades, depending on underlying investment objectives, size of order, liquidity of issue, risk of market impact, etc.

“Best execution is driving buy-side curiosity on alternative protocols and sources of liquidity,” says Jenkins.

Sell side adapting to client demand

In response, brokers are evolving their execution propositions; trading venues on both the dealer-to-client (D2C) and dealer-to-dealer (D2D) sides of the market are offering a wider range of trading protocols; and high-frequency trading PTFs are offering liquidity to the buy side beyond CLOBs. Already providers of more than half of all liquidity in the D2D market, HFTs are responding to RFQs on the two leading D2C trading venues (Tradeweb and Bloomberg), offering streaming prices on D2D platforms, and striking partnerships with primary dealers to supply liquidity via their single-dealer platforms, which are rapidly turning into multi-functional eco-systems in their own right.

With balance sheets constrained by Basel III, primary dealers’ US Treasuries services to the buy side increasingly mirror those in equities, focusing on execution tools, liquidity access and analytics. Some, including Credit Suisse, have launched ATS-like platforms, to offer access to internal flow, third-party platforms and inter-dealer CLOBs, using a variety of execution options, with the bank serving as risk-transfer counterparty. Sell-side firms are also partnering with PTFs: in late 2017, BNP Paribas announced a deal with electronic market-maker GTS aimed at offering enhanced liquidity and pricing to institutional clients.

Meanwhile, the value propositions of venues are evolving, and in some ways merging, as direct stream aggregation (DSA) gains momentum. DSA emerged in the D2D market as a means of enabling PTFs to offer liquidity to primary dealers on a named, bilateral basis, to enable the latter to manage block-sized risk more effectively than on a CLOB. The primary players – Tradeweb, BrokerTec and LiquidityEdge – have differing approaches to widening out these capabilities to the buy side. The latter offers DSA alongside a range of relationship-focused protocols, having opened its DSA channel to the buy side in Q3 2017, since when 15 asset managers and five hedge funds have gone live. BrokerTec Direct is presently operating on legacy EBS technology, but version 2.0 is expected to have greater functionality, with RFQ and streaming protocols for sending inquiries to liquidity providers. Tradeweb’s buy-side clients can currently only view streaming prices between PTFs and brokers for benchmarking purposes. Both firms are leaving the door open for buy-side access to direct price streams, but are cautious as this would further blur traditional boundaries between interdealer brokers – Tradeweb also operates the Dealerweb D2D platform – primary dealers and buy-side clients.

More radical change seems inevitable. Although additional reporting requirements are expected to further enhance transparency in the US Treasuries market, only limited progress can be made due to the differing clearing options and regulatory obligations of primary dealers and PTFs, which currently frustrate attempts to monitor and compare overall execution outcomes. A more standardised approach to clearing – expected to be proposed by a Federal Reserve Bank of New York working group in the first half of 2018 – may also make it easier for new trading venues to launch, potentially offsetting claims made in a recent class action brought by US pension funds that primary dealers have used their dominance to limit market access and manipulate auctions.

A further challenge for the US Treasuries market this year may lie in shifting dynamics of supply and demand. “Large asset managers have probably faced very few problems sourcing liquidity in the US Treasuries market in recent years, but volatility only has one way to go with macro factors such as higher interest rates and Federal Reserve balance sheet unwinding,” notes Hirak Biswas, head of product and strategy at LiquidityEdge.

At the end of January, the US Treasury Department said it planned to increase the size of upcoming bond and note auctions in the Feb-April quarter by US$42 billion to meet increased funding needs arising from the Fed’s unwinding exercise and the tax bill passed by Congress in December 2017.

AllianceBernstein’s Scott acknowledges that the market is “worried” about expanding deficits. “Primary dealers and PTFs may need to trade more defensively around liquidity events such as auctions, month-end, quarter-end, and fiscal year-end,” he added.

Only time will tell whether the US Treasuries market is big enough to simultaneously digest increased supply and accommodate major structural change.

©Markets Media Europe 2026

more valuable")