Sources report the Danish Financial Services Authority (DFSA) has launched an investigation into fund losses from mortgage bond holdings, as rising interest rates have pushed down bond prices and increased selling pressure.

Denmark’s mortgage lenders issue bonds to underpin the loans using the ‘match funding’ principle, which allows a potential homeowner to take out a mortgage for which the bank raises finance by selling mortgage bonds of the same value. The borrower pays the bank the principal and interest payments, while the money is then transferred to the bond holders. Callable mortgage bonds mean that borrowers on a high fixed rate can repay their loan early and take out a new mortgage at a lower rate if interest rates decline.

In a recent podcast, Mikael Mogensen, COO of financial website Mybanker, explained the cycle of selling: “When bonds are trading close to par, the probability of them getting pre-paid means that duration [the length of time for an investor to be repaid the bond’s price by its total cashflows] are significantly lower than the maturity date signalled, but now when they are trading Kr 0.85-0.90 [to the 1 Kr] it is much less likely that they are going to be prepaid at par,” he says. “That has increased duration, and the entire duration in the market increases, when this happens … When duration increases the need to sell bonds increases, and that creates a self-enforcing loop where interests rates going up, meaning duration is going up, meaning people have less appetite for mortgage bonds. That forces another round of selling which increase duration and so on.”

Danmarks Nationalbank reports that foreign investors owned Kr 827 billion Danish mortgage bonds in January 2022 which corresponds to 26% of the total nominal value of Kr. 3.2 trillion. The rest, owned locally, is held by a combination of investors including leveraged hedge funds. Where it find insurance and pension fund portfolios are balanced between bond classes, other investment fund portfolios are skewed toward callable bonds.

Issued bond prices are inversely linked to interest rates, becoming less valuable to investors as interest rates rise; as interest rates have risen in Denmark this has triggered losses amongst bond holders, which are even greater for leveraged funds.

Brett Chappell, CEO of Sherpa Edge Trading, speaking on the same podcast said, “I don’t recall any time over the past decade where we have had such a sell off – between 10 and 15 figures down.”

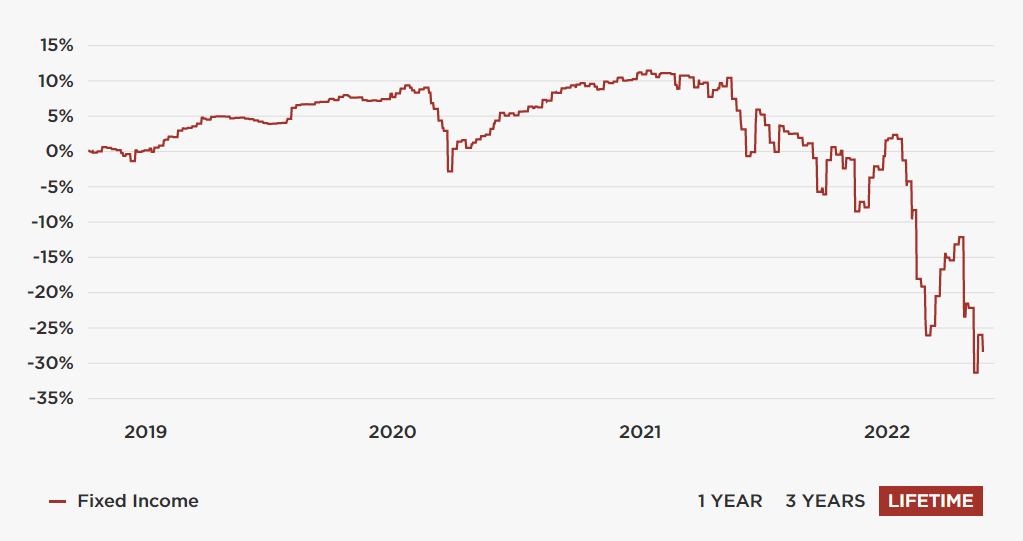

Several Danish fund are already reporting significant losses; HP Fonds’ Fixed Income fund is currently reporting losses over a 12-month period of 33%. It invests primarily in Danish government and mortgage bonds and secondarily in short- and medium-term European government bonds, corporate bonds and European covered bonds.

CABA Hedge focuses on the creation of absolute returns, after costs, of 5-6% per year measured over a 5-year period. It is currently reporting 12-month losses of 12.86%.

“If you’re an investor, what is going to happen if you are leveraged?” asked Chappell. “Because you are going to find yourself in a situation where there are going to be redemptions. If you’re a pension fund that is one thing. You have to figure out your assets and liabilities. But if you are a Danish mortgage bond hedge fund you might be pretty concerned now because you are going to have withdrawals.”

A paper entitled ‘Domestic bond portfolio adjustments during duration jumps’ published by the Danmarks Nationalbank in December 2021 had no mention of leverage, but did note, “Detailed information about the sectors’ uses of interest rate swaps and derivatives, which are particularly relevant for I&P companies and some investment funds, is unavailable. This implies that we are unable to capture if the companies or funds counter duration increases using swaps and thereby fully explore how they react to duration jumps. Interest rate derivatives are necessary to have to obtain the full picture of duration management. With our data, we are still able to analyse the bond transaction reaction following duration jumps. These are what matters directly for the yield spread dynamics in the bond market.”

©Markets Media Europe 2025

more valuable")