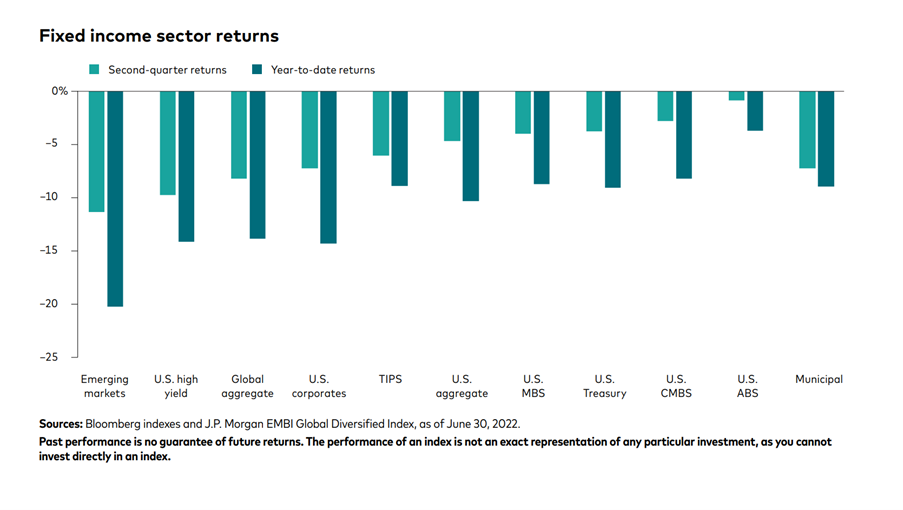

Fixed income sector investments have proven worst for emerging markets funds year to date, according to data from JP Morgan and Bloomberg indices, driving outflows for the fund managers. According to the Institute of International Finance, a very positive sentiment from investors over the past 18 months has soured, leading to five continuous monthly outflows for EM funds to July.

For heads of trading, building the capacity to trade into emerging markets can be a real challenge – and as this data show one full of pitfalls. The risk of building a large EM trading function from the ground up is a potential cost that may hang over a trading team if the assets under management (AUM) being booked through that trading function are relatively transitory.

For heads of trading, building the capacity to trade into emerging markets can be a real challenge – and as this data show one full of pitfalls. The risk of building a large EM trading function from the ground up is a potential cost that may hang over a trading team if the assets under management (AUM) being booked through that trading function are relatively transitory.

There are limited ways to manage this risk, without setting up a trading desk on location and biting the bullet on the fixed cost and resource commitment.

One is to develop a flexible trading desk with traders covering EM as well as other markets. This can mean one or more team members working out of hours, and being tied up handling largely one-directional liquid flows, but integrating very easily into the existing investment process.

Another is to use electronic platforms, which traders say can be very positive especially with the request for market trading protocol. These limit the outlay but also carry the risk of on-screen pricing becoming unreliable in volatile conditions, according to buy-side traders.

A third is to buy flexible resource through an outsourced trading provider, to support trading on a temporary or permanent basis.

While no solution will fit every circumstance, it is clear that heads of trading should be considering each of these seriously in order to avoid having resources tied up too heavily, when flexibility is needed.

©Markets Media Europe 2026

more valuable")