Direct streaming of dealer prices could allow traders to bypass third party venues, if their desktop systems can be used to execute direct streams from dealers.

Direct streaming of dealer prices could allow traders to bypass third party venues, if their desktop systems can be used to execute direct streams from dealers.

Execution management systems (EMSs) could become a focal point for direct connectivity with dealers on the buy-side desktop. To date they have often struggled to find a place in the hearts of many buy-side bond traders. Their capabilities have been severely truncated in the fixed income space where low-touch trading is less advanced, relative to more liquid asset classes, and there are more stages requiring human intervention.

Yet some buy-side traders believe that EMSs have a future on their desks as a way of combining prices sent straight from dealers, platform trading and new protocols.

“We started trading with one major dealer who wanted to directly connect and stream their axes in this way,” says Tim Morbelli, head of municipal trading at AllianceBernstein, which is rolling out its own EMS across fixed income asset classes. “Now every major dealer wants to connect in this way. It is not only dealers streaming their axes. We are building trade protocols through it as well such as click to trade, click to engage – if I want to engage on a bid wanted in the marketplace – all of that exists today.”

For an EMS to function effectively it needs prices that can be traded against a lot of input, including data on execution which can support trading decisions, and to manage orders to the point of execution.

In bond markets this can present a problem. There can be little to no natural pre-trade transparency in the market, as would be provided by an exchange’s central limit order book in the equity markets. If a price is requested from a dealer, it will not necessarily be firm.

Even when prices are streamed directly from a counterparty to a client or a venue, they will not necessarily be executable. The buy-side may not know this until they try to trade against the price, due to a lack of standard terminology around price distribution.

Equally, post-trade information is limited. It can be acquired from private sources, any one of which might cover up to 75% of the market. In the US there is a public post-trade tape, TRACE, which provides a restricted view of what has traded and at what size. Europe has no equivalent.

Now, changes are taking place which could allow EMSs to operate more effectively. Firstly, streaming prices is becoming more commonplace in the bond markets which supports price formation on the trading desk.

The International Capital Markets Association (ICMA) has set out guidelines harmonising the language used to describe the way dealers distribute prices – which in turn clarifies whether or not they are firm, and which level of information will be provided.

Liz Callaghan, director of markets at ICMA. “Streaming can be on trading venues and it can be through direct trading. More trustworthy pricing distribution and standardised practices will positively impact electronic trading and automation, whether execution is direct from sell-side to buy-side or on a trading venue. We cannot expect to have advanced electronic trading unless we have bond pricing distribution standardisation.”

Collectively this means that EMSs could become a tool for aggregating executable prices and engaging with them on a negotiated or more automated basis, and putting the buy-side trader on the front foot.

Mark Watters, co-founder of EMS provider AxeTrading says, “In terms of the evolution of the fixed income EMS we are at a pivotal moment in trading technology. Can the buy side trader receiving prices take a more active role supporting price making as well as price taking?”

Next-stage evolution

This does not herald an immediate change in trading behaviour, rather it creates a potential path to make the EMS a more viable tool, by supporting bilateral execution on the desk as well as multilateral trading on venues. The ability to engage directly with executable prices is still in its early stages.

“There are a lot of buy side firms asking for access to single dealer APIs, initially to get pricing data,” says Watters. “Now some of those firms are looking beyond being price takers to more interesting and challenging engagements. If they can aggregate multiple sources of data on the desk, they can use that to build their own prices, before they go out into the market.”

Barriers exist, including technical hurdles that will limit some EMSs ability to cope, not least if they are adapted from systems for trading other instruments.

“Most EMSs that exist today are equity-based technology that have been augmented to meet fixed income needs,” says Morbelli. “We are not the equity markets, we have different dynamics and protocols.”

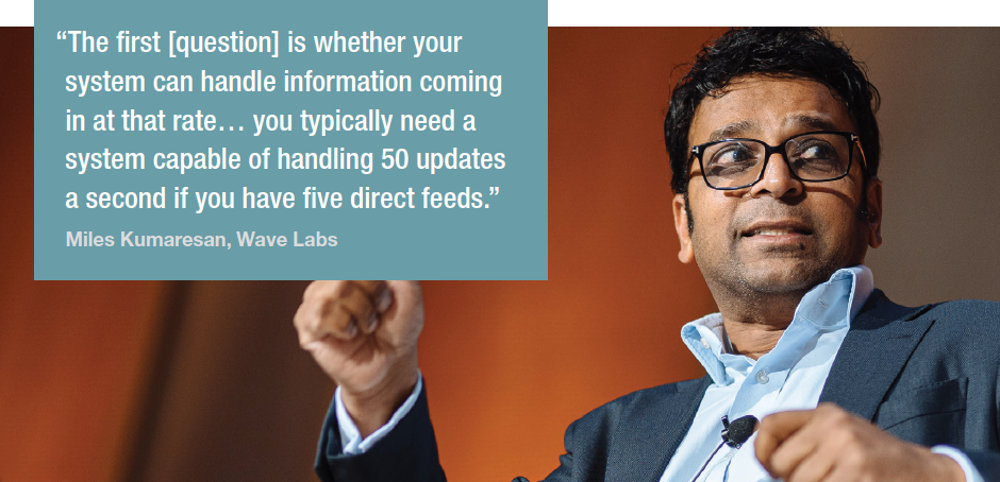

There are two challenges in handling streaming prices, notes Miles Kumaresan, founder and CEO of execution system provider, Wave Labs.

“The first is whether your system can handle information coming in at that rate,” he says. “With Neptune sending out a million ticks in Europe and the same in the US that works out to be roughly ten updates a second. Banks send updates every time they make a change to an axe. An ETF market maker might send out roughly 500,000 updates if you cover the whole fixed income universe. So you typically need a system capable of handling 50 updates a second if you have five direct feeds.”

The other technical issue is around the value it provides once it has the streamed prices.

“You need to ask how you use it, beyond simply aggregating – how do you show the information and apply it,” he adds. “That said streamed prices would be very useful, not least for TCA as well as execution.”

Where execution happens

There may also be regulatory challenges to direct trading, not least if the EMS is perceived to be a trading venue of some sort. Byron Cooper-Fogarty, interim CEO at axe-streaming platform, Neptune, believe these could hamper progress.

“It feels like the regulatory headwinds are against direct executions,” he says. “Most notably in Europe, but also in the US as well. You have the CFTC looking at Treasuries, the SEC looking at corporate bonds and muni’s as well, and the Reg ATS rules expanding there.

Nevertheless, he believes that streaming via a system like Neptune could still deliver that access to executable prices on the desk.

“There has been a revival around direct connectivity; I think that’s a bit of a fad,” he argues. “Dealers want to connect to the major OMS/EMS clients through application programming interfaces (APIs), and that they can get that through Neptune via one connection rather than having several hundred. That’s where standardisation makes sense for those guys.”

If the right systems can be employed and the right connectivity established, Morbelli believes that both direct and multilateral execution could be employed simultaneously in order to deliver best execution.

“An API costs US$2500 per year to build out and maintain,” he says. “The costs for connectivity are getting less expensive. That said, will an asset manager want to connect with 20 dealers? No. Will a dealer want to connect with 200 asset managers? No. But we do [a lot] of our business with our top six dealers. We also want MarketAxess’s Open Trading network. We want Tradeweb’s ability to net spot. These are additive to our clients, so want to connect to [those] markets too.”

©Markets Media Europe 2021

©Markets Media Europe 2025

more valuable")