As we move into summer of 2026, central bank activity is strikingly different from where markets started the year, and it is directly legible in the trading data.

The Fed kept the federal funds rate at 3.5–3.75% for a third consecutive meeting in April. The ECB maintained its 2% rate in April. Investors have less confidence in Fed rate cuts later in 2026, which is a major shift from the two cuts anticipated earlier, with up to three ECB rate rises this year.

Recent comments from Fed members show that uncertainty remains while energy supply is constrained by the Iran conflict. As BofA analysts have observed, the fixed bottleneck created by the period of ongoing conflict already, sets a floor for the oil price, meaning costs will remain in a higher range than expected in 2026.

This appears to have created a sustained, high-turnover environment as investment managers rebalance duration exposure, rotate out of longer-dated bonds and into shorter maturities, or reposition to match curve expectations.

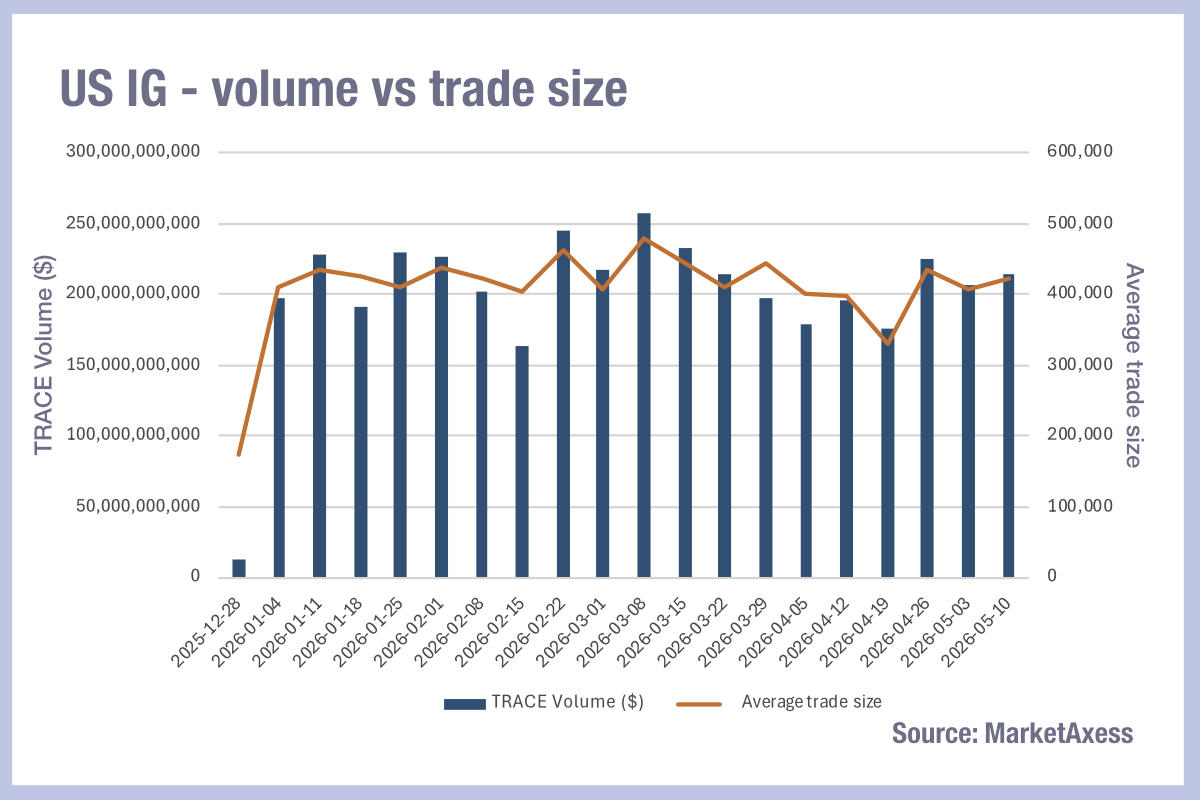

The most striking feature of this on trading costs, looking at the latest data from MarketAxess, is that US investment grade saw the tightest bid-ask spreads of the year in both price terms at 0.079 price % of par on week beginning 11 May, below the January lows). Average trade sizes have fully recovered to US$421k in the second full week of May, down from US$478k in the second week of March, and close to the year-to-date weekly average of US$420k and volumes hit a solid US$213 billion for that week, above the US$210 billion average.

Yet major electronic trading platforms are reporting reduced activity, as a result of the enormous primary market pipeline, some US$976 billion issued YTD, up 21% on the same period in 2025. Despite this supply of fresh on-the-run bonds that could be highly liquid, it appears to be having the opposite effect to normal, when primary activity increases secondary liquidity.

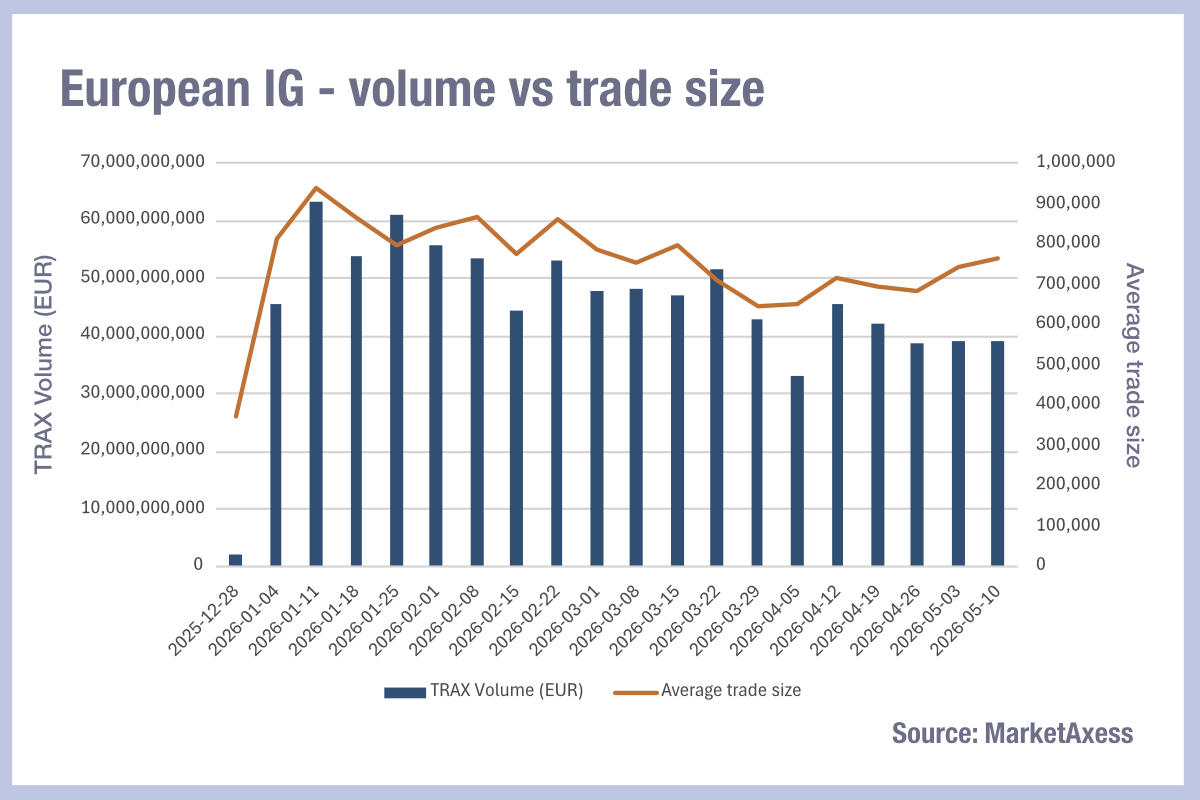

European IG also saw its tightest bid-ask spreads week of 11 May, at 0.059 price % of par, yet it saw average trade sizes of €763k which remain well below the January peak of €937k, and weekly volumes €39 billion are persistently below the €47–63bn range of Q1.

European IG also saw its tightest bid-ask spreads week of 11 May, at 0.059 price % of par, yet it saw average trade sizes of €763k which remain well below the January peak of €937k, and weekly volumes €39 billion are persistently below the €47–63bn range of Q1.

The ECB’s Governing Council has said, “The implications of the war for medium-term inflation and economic activity will depend on the intensity and duration of the energy price shock and the scale of its indirect and second-round effects. The longer the war continues and the longer energy prices remain high, the stronger is the likely impact on broader inflation and the economy.”

European IG investors face the prospect of a central bank potentially tightening rates into a slowdown, which could increase reduce new bond prices from the rates side relative to outstanding bonds, while headwinds to the economy increase credit risk from below. Dealers appear willing to show tight spreads for small clips, but participants are cautious about committing balance sheet to larger sizes.

©Markets Media Europe 2026

more valuable")

more valuable")