This year is shaping up to be a landmark year for corporate debt markets globally, with issuance running at record or near-record levels on both sides of the Atlantic.

The US investment-grade market has led the charge by a wide margin. SIFMA data shows US corporate bond issuance reached US$1.01 trillion through April 2026, up 28.2% year-on-year, putting the market on course to smash previous annual records.

Three structural forces are driving this boom. First, is the refinancing wave with banks estimating more than US$1 trillion of corporate debt will needs to be refinanced in 2026, much of it originally issued during the ultra-low interest rate years of 2020–21. Second, is the AI spending cycle. Analysts at Morgan Stanley estimate AI-related debt issuance could hit US$400 billion in 2026, as AI hyperscalers fund development of infrasctructure with debt. Third, M&A activity is generating additional supply, with debt-funded transactions across a range of sectors adding to the pipeline.

The financials sector issued $274 billion of bonds in Q1 2026 alone, according to Breckinridge Capital Advisors, driven by high redemptions, regulatory capital requirements, and balance sheet growth. Utilities have also been active, with the sector issuing $56 billion in Q1 to help increase electric grid capacity for data centres and other uses.

Nicolas Alfner, co-head of research at Breckinridge, wrote, “Spread volatility driven by geopolitics, AI, and private credit concerns did have a market impact with some ‘no deal’ days and periods when new issues traded wider. As expected, hyperscalers brought large, multi-tranche bond deals that were priced to move given the large size of the borrowings. The Technology sector was the third largest borrower, issuing $64 billion and adjacent sector Communications issued $50 billion.”

European corporate bond markets have also seen elevated activity, though at a smaller absolute scale. The strong Eurobond issuance trend from 2025 carried into early 2026, underpinned by reduced recession fears and inflation closing in on European central bank targets. Law firm, Akin Gump, noted in March that is had seen US companies being significant participants: aggregate Eurobond sales by US issuers reached a record US$100 billion by September 2025, a trend that has continued into this year as corporates seek to diversify their funding currency.

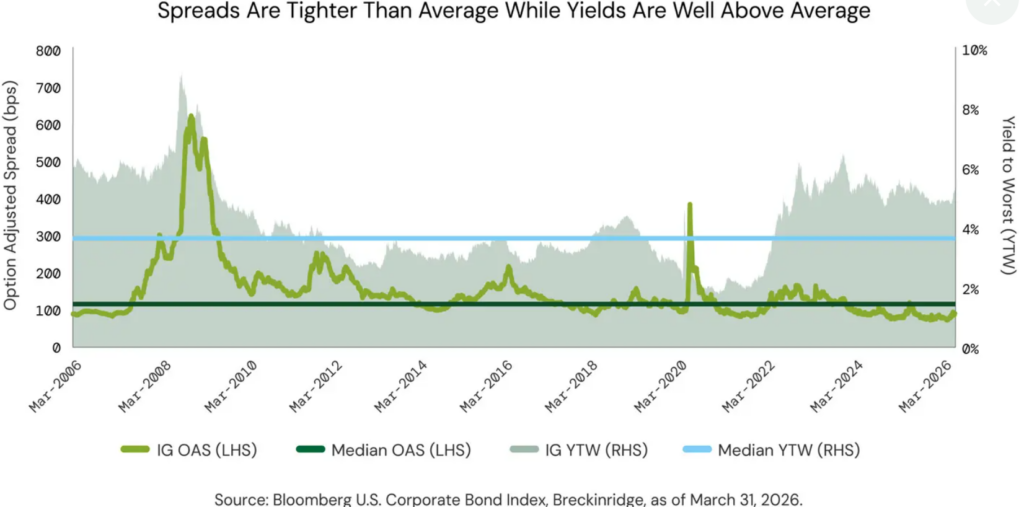

Corporations and governments globally borrowed roughly $260 billion across currencies in the first week of 2026 alone, the highest tally on record for that period. Underpinning all of this is a receptive investor base: investors expect strong corporate balance sheets, continued economic growth, and some expect Federal Reserve rate cuts, which have collectively kept spreads tight and demand for new issuance strong in 2026.

©Markets Media Europe 2026

more valuable")