Key parts of bond market electronification are still up for contention, with stiff competition across pre-trade, primary and secondary market services.

Key parts of bond market electronification are still up for contention, with stiff competition across pre-trade, primary and secondary market services.

In 2024 The DESK has conducted its 10th annual Trading Intentions Survey, designed to help buy-side traders gauge consensus around which platforms are being used by other traders. The report was instigated at the behest of a trader who said he could not see how a specific platform was going to work, and he wanted to know what his peers thought of the market for data, analytics and trading services on offer.

This year we see the big incumbents in place ten years ago are still the big three, but there has been solid growth from several other players, and there are big moves from certain challengers.

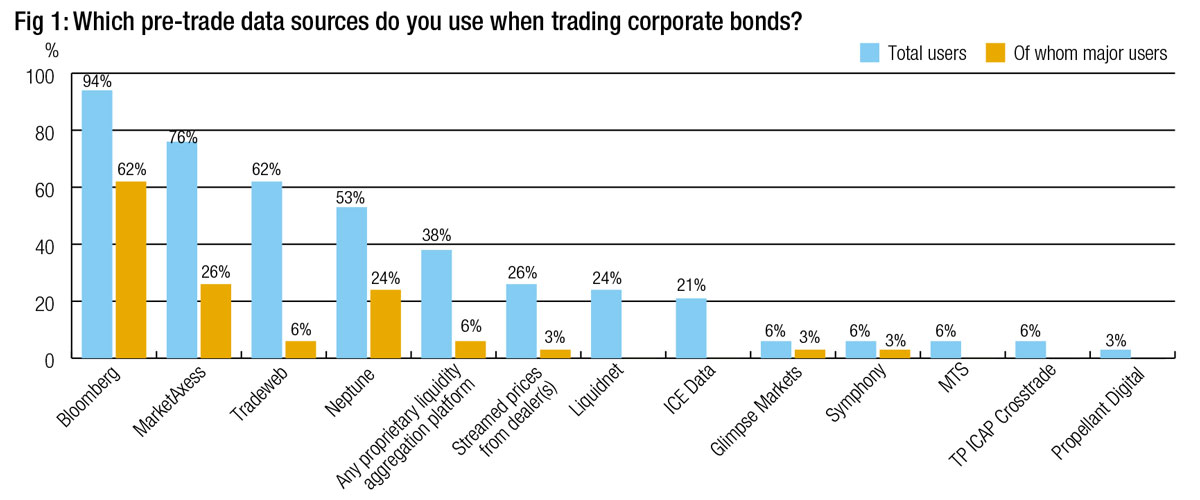

Pre-Trade Data Sources

Bloomberg is the leading pre-trade service, with the greatest number of buy-side desks in 2024, with 94% of respondents using it. MarketAxess is in use by 76% of respondents, followed by Tradeweb at 62% (see Fig 1).

Neptune is in use by over half of respondents, demonstrating that efficient engagement with axes is still key to liquidity discovery for buy side traders, with approximately half of users classifying themselves as major users of the platform. Proprietary analytics tools are still a major part of the buy-side armoury and use of dealer streamed prices is also invaluable pre-trade.

Both Liquidnet and ICE are well-used pre-trade tools, while other platforms are relatively nascent across the whole respondent base.

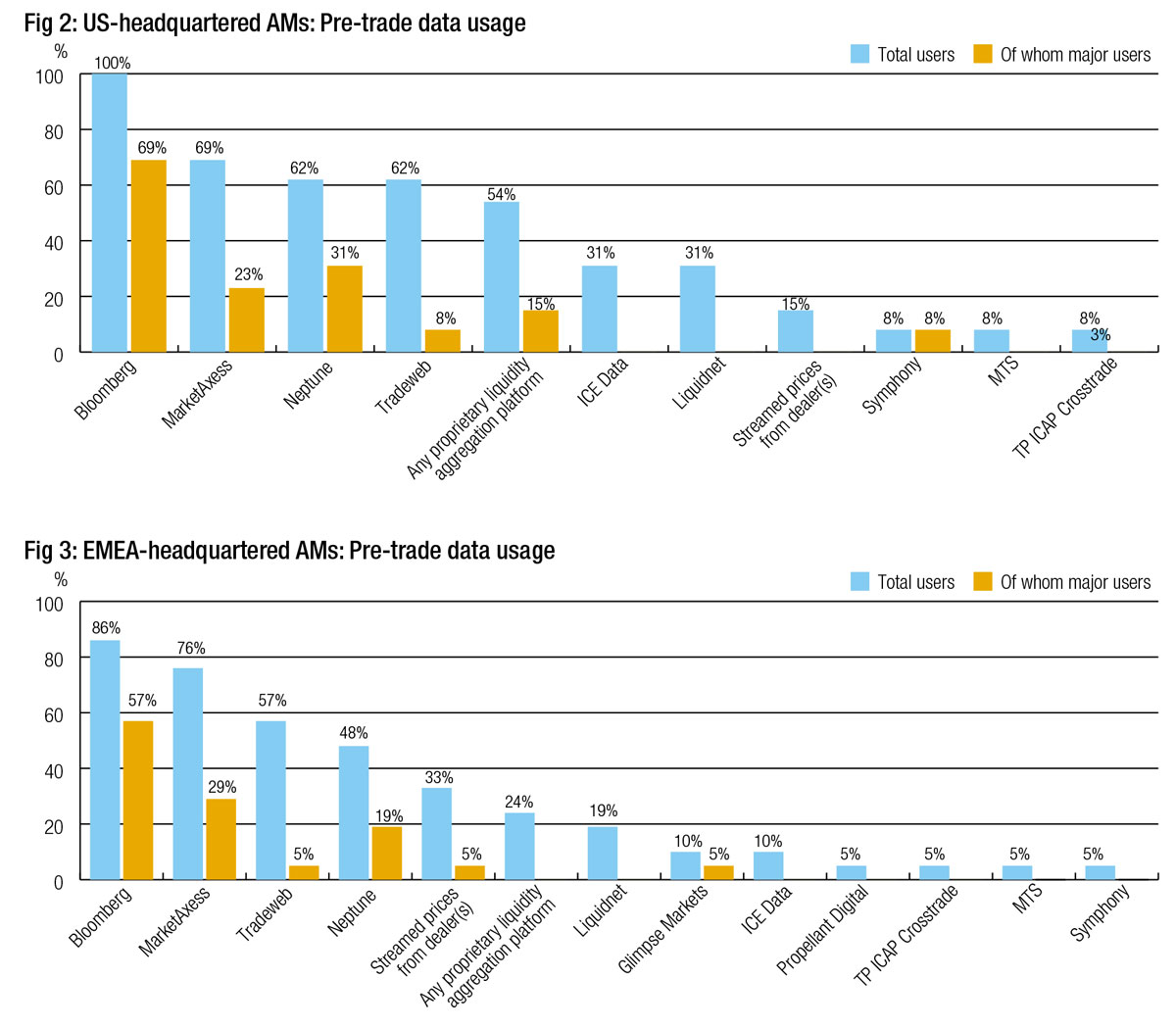

Breaking that down by geography, firms headquartered in the US (who also largely trade internationally) are 100% engaged with Bloomberg on pre-trade data and 69% consider themselves major users (see Fig 2).

They are also big users of MarketAxess pre-trade data, as well as Neptune axe information and Tradeweb’s data. More than half of these firms also have a proprietary liquidity aggregator, while a third are employing ICE Data Services and using data from Liquidnet.

European headquartered firms (who also largely trade internationally) are also majority Bloomberg pre-data users although to a slightly lesser extent than in the US (see Fig 3). These firms use MarketAxess data to a greater level than US headquartered firms, and the use of streamed pricing data is twice as high than for US based firms. Conversely, while data from both Tradeweb and Neptune is in use by roughly half of these firms, that is lower than that seen by US headquartered businesses. There is also engagement with Glimpse Markets by these firms, the buy-side data sharing collective based in Europe which has a 10% market share – half of whom are major users.

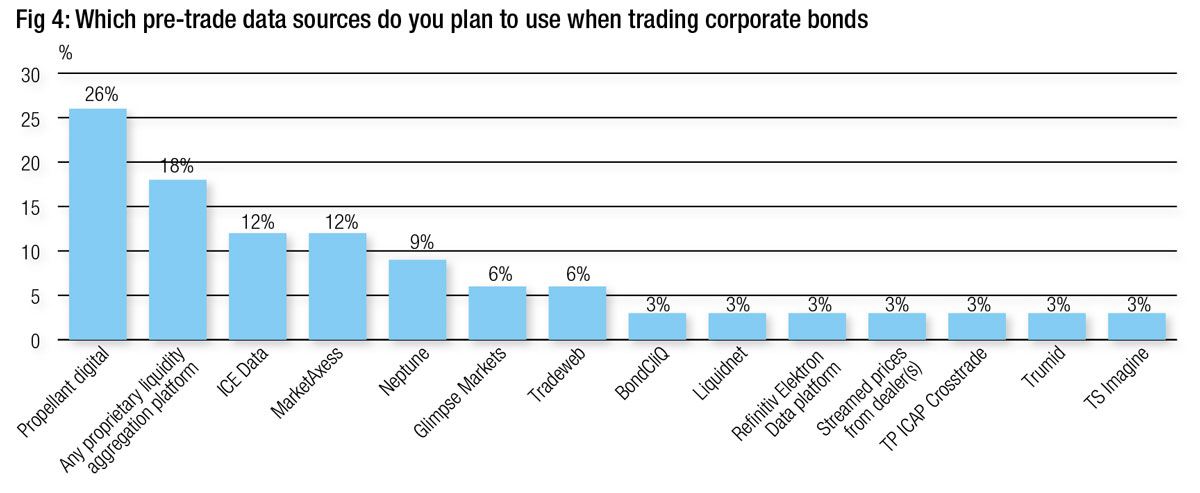

The pipeline for adoption has one clear winner – Propellant Digital (see Fig 4). With just over a quarter of firms saying they plan to use the service, it is clearly impressing potential users. Nearly a fifth of firms plan to build a proprietary liquidity aggregation analytics system. After Propellant, the most promising commercial data offerings are from ICE Data and MarketAxess who both have an expected 12% of respondents planning to adopt their data offerings.

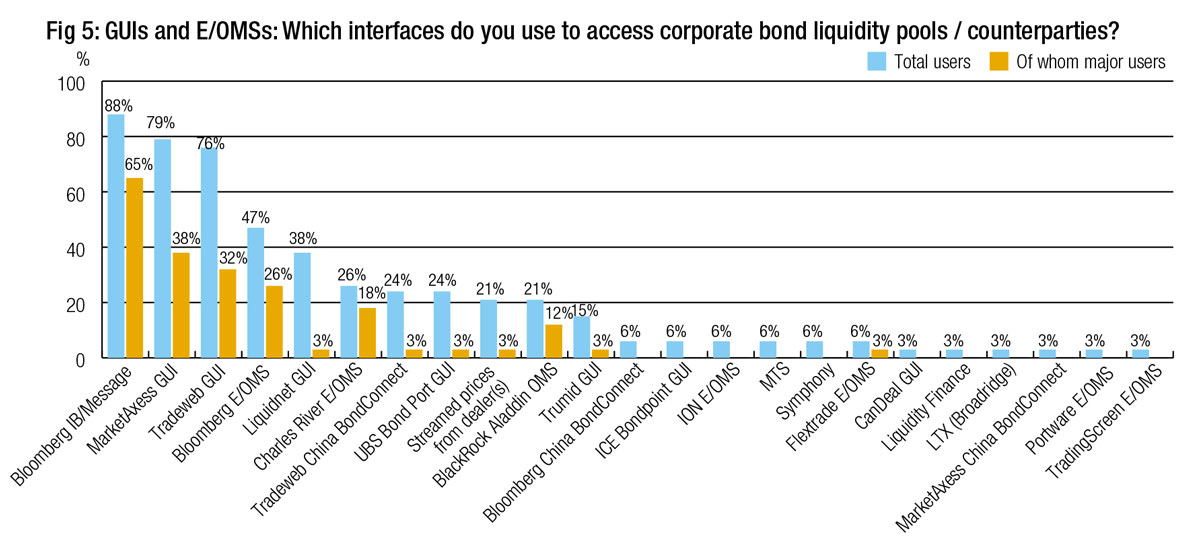

GUIs, interfaces and E/OMSs

Ongoing electronification of markets across regions is still largely managed via the interfaces that trading platforms use, reflecting the need to engage directly with the trading protocols and data that each offers. The leading communication channel is Bloomberg IB / message which 88% of respondents use today, most of whom are major users, reflecting the need for unstructured communication in bond market negotiations across both comp and non-comp trades (see Fig 5). MarketAxess’ GUI is used by 79% of respondents, making it the leading trading platform interface in credit. That is closely followed by Tradeweb; with 76% of the market Tradeweb has proven itself very able in the credit space.

Across execution and order management systems (E/OMSs), one feature stands out – they are heavily used when they are in place. Bloomberg’s E/OMS services are used by 47% of respondents and more than half of those are major users of those tools. Charles River is used by 18% of firms and two thirds of users are major users. Aladdin has been adopted by 21% of respondents with over half seeing themselves as major users.

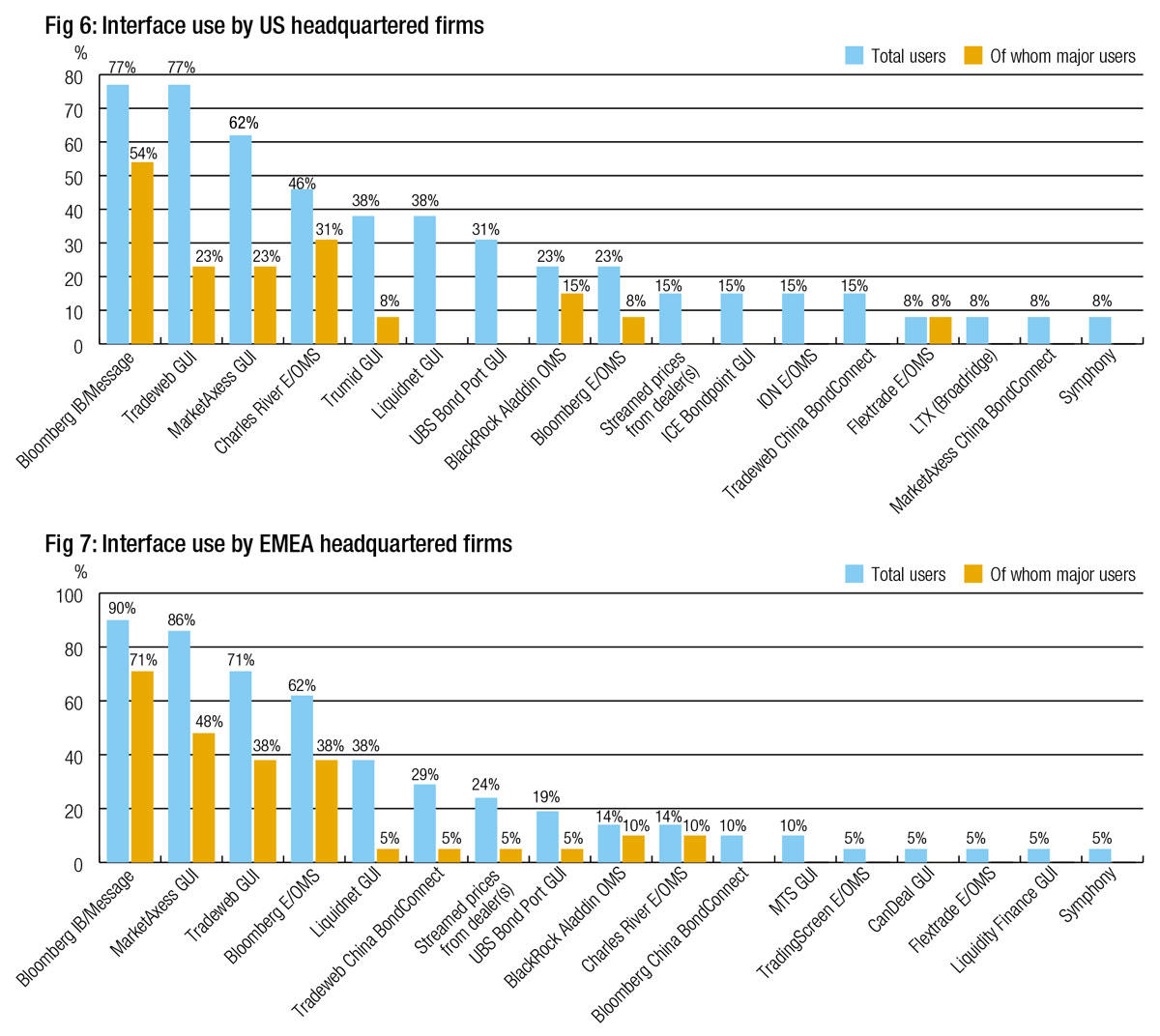

Splitting out by the location of a firm’s headquarters, it is apparent that Tradeweb’s focus on workflow has made the firm’s interface highly successful amongst US-based firms, at 77% tying with Bloomberg IB / Messaging for most used interface (see Fig 6). MarketAxess is in second place with 62% adoption. Charles River is the most used E/OMS with 46% of US-HQ firms, while both Trumid and Liquidnet have nearly 40% of respondents using them.

Amongst European headquartered firms, MarketAxess’s GUI at 86% sits close behind leader Bloomberg IB/ Messaging (90%), Tradeweb’s GUI being third at 71% (see Fig 7). Bloomberg’s E/OMS has a very high adoption rate relative to its peers, with 62% being users. Liquidnet’s interface has a 38% adoption rate, putting it clearly in the top five GUIs.

Amongst European headquartered firms, MarketAxess’s GUI at 86% sits close behind leader Bloomberg IB/ Messaging (90%), Tradeweb’s GUI being third at 71% (see Fig 7). Bloomberg’s E/OMS has a very high adoption rate relative to its peers, with 62% being users. Liquidnet’s interface has a 38% adoption rate, putting it clearly in the top five GUIs.

Looking ahead at the planned adoption of GUIs, Trumid has a strong pipeline amongst respondents, with 12% planning to take the system on (see Fig 8).

Primary market tools

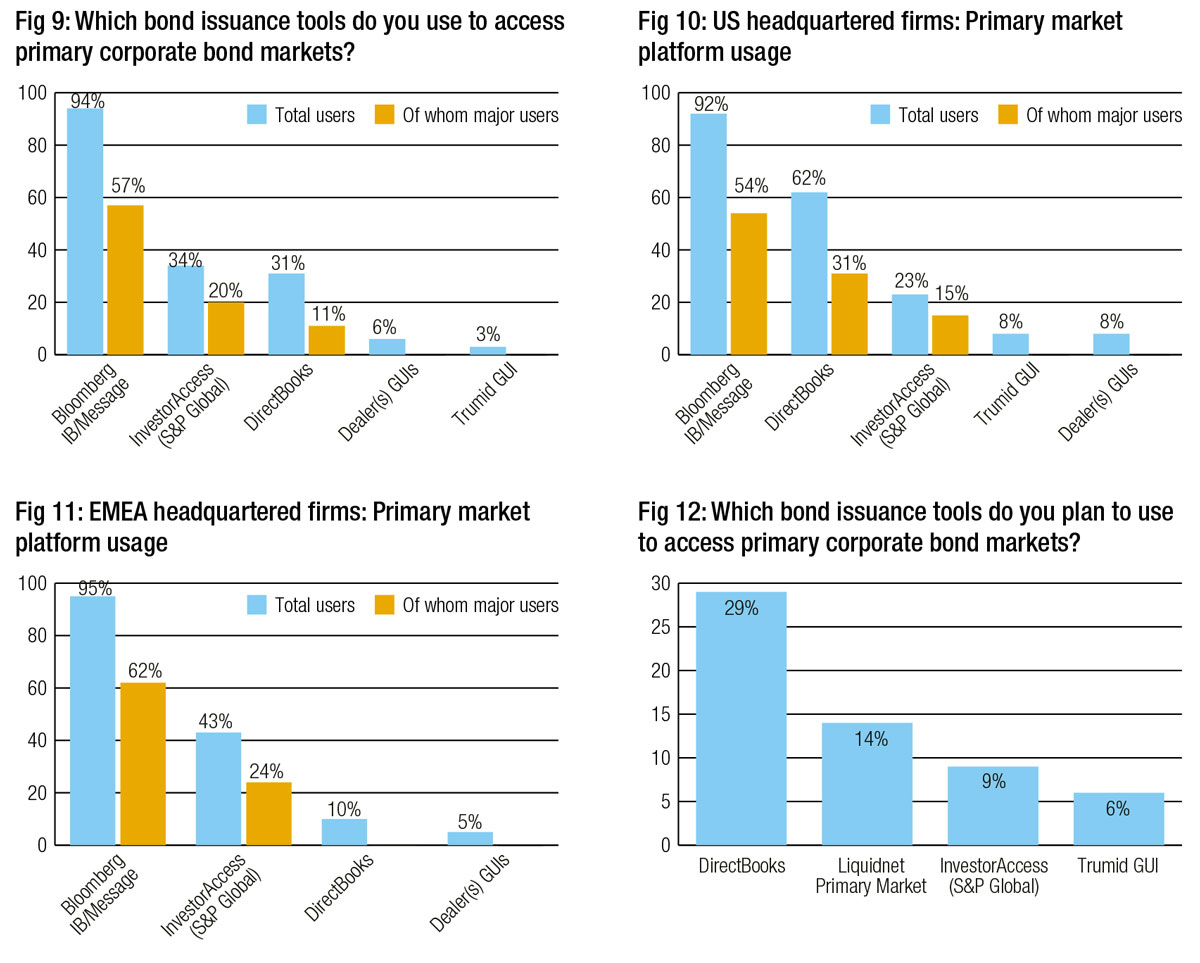

New issue efficiency is a hotly contested area in 2024, and we see that 94% of firms are still using IB/Message on Bloomberg for primary market activity, with 57% being major users of these tools (see Fig 9). However, there is still a strong level of adoption of Investor Access (formerly Ipreo) and DirectBooks which have a 34% and 31% take-up respectively.

Splitting by country of origin, asset managers with a US HQ have adopted DirectBooks primarily, with 62% of respondents using the platform half of whom are major users (see Fig 10). Nevertheless 23% of US-based firms have adopted Investor Access and more than half rate themselves as major users. Trumid is also in play here, with its grey market functionality allowing firms to trade newly issued bonds, adding liquidity into the mix early on in the bonds’ life.

Those asset managers headquartered in EMEA have adopted Investor Access primarily, with 43% using it, of whom more than half classify themselves as major users (see Fig 11). Directbooks has nevertheless been adopted by 10% of firms, despite being far more nascent in securities outside of the US.

DirectBooks has the biggest pipeline for onboarding, with 29% of firms planning to use it in the future (see Fig 12). Liquidnet has 14% of respondents looking to adopt it in future, while 9% have plans to take on Investor Access as a new platform.

Secondary market trading platforms

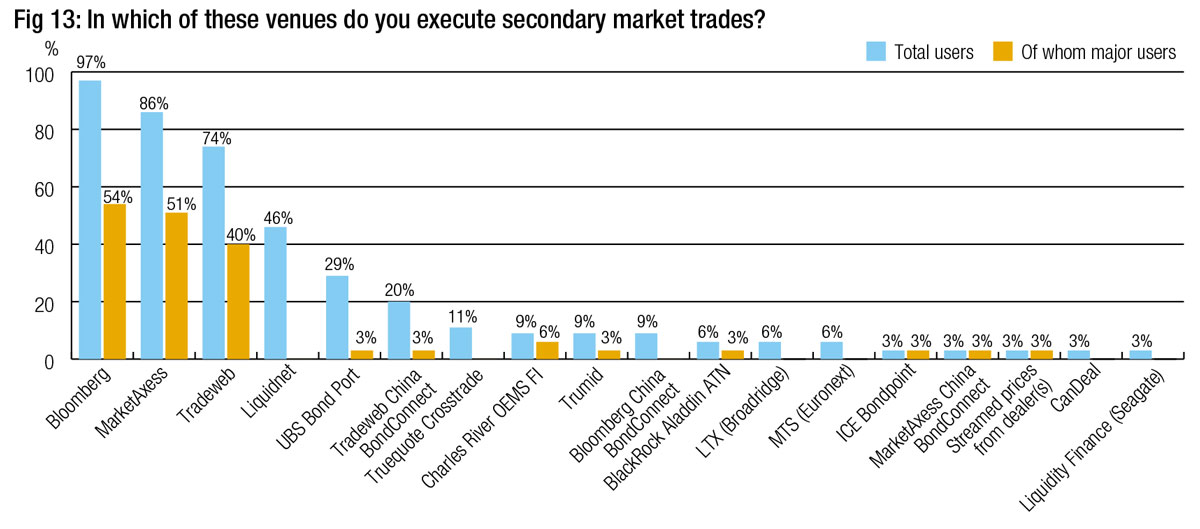

The most widely adopted secondary market bond trading platform is Bloomberg, used by 97% of respondents. MarketAxess has 87% of firms using it for trade execution, while Tradeweb is third at 74% (see Fig 13). Each has fought tooth and nail via new trading protocols, platform interface enhancements and other services to encourage buy-side firms to use them to connect with dealers. These firms have been in the top slots for the last ten years, but newer platforms have also achieved success.

Liquidnet’s credit trading venue is in use by 46% of buy-side firms, and the BondPort platform from UBS has nearly 30% of respondents using it. These are in line with historical use.

There has been a marked decline in the fortunes on China BondConnect platforms, reflecting the decline of the country’s credit outlook, but with 20% of firms as users Tradeweb has the largest share here.

It is also worth noting that streamed prices from dealers are used for execution far less than they are for pre-trade and interfacing (see above). That suggests the economics of providing those prices may not be paying off for dealers, and potentially challenge their value to the sell side.

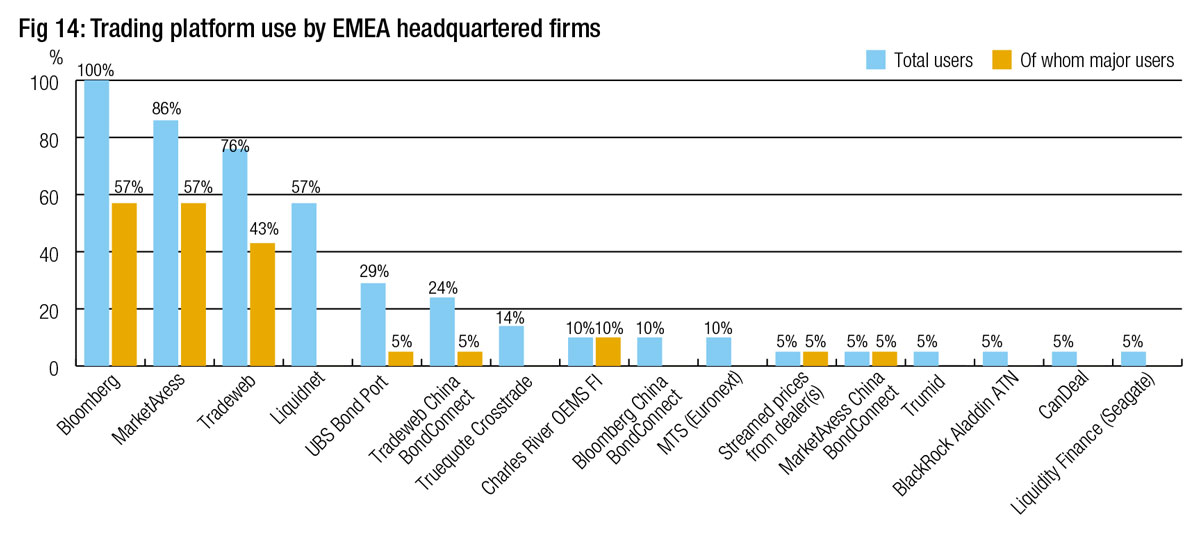

Breaking venue use out by geographical bias, EMEA headquartered buy-side firms follow the global pattern very closely (see Fig 14). They are fully engaged (100%) with Bloomberg for trading, and over half are major users. MarketAxess is used by 86% of asset managers and two thirds of that number (57% of respondents) consider themselves major users. Tradeweb is used by 76% of firms, also with over half major users. More than half of European asset managers use Liquidnet but none are major users.

More unique points are found further down the curve. Tradeweb’s China BondConnect is in use by nearly a quarter of respondents and Truequote’s internal crossing service – unusable in the US – is being employed by 14% of firms.

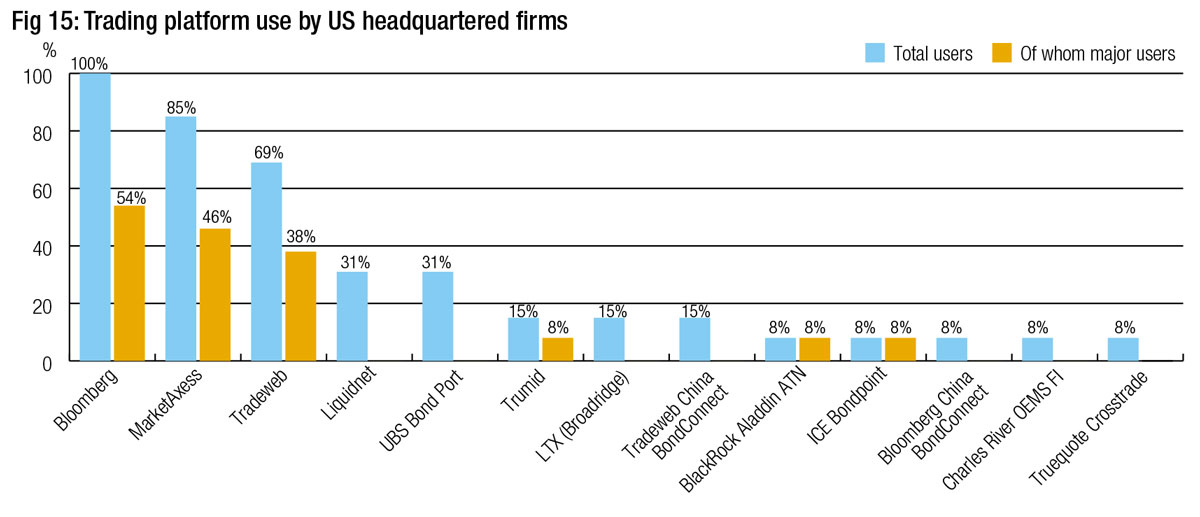

The US-headquartered firms reflect the same pattern of use for the tip four trading platforms (see Fig 15). Among the growth firms we see Trumid, which is being used by 15% of respondent in this category, more than half of which are major users, and also LTX which has a 15% adoption rate for trading.

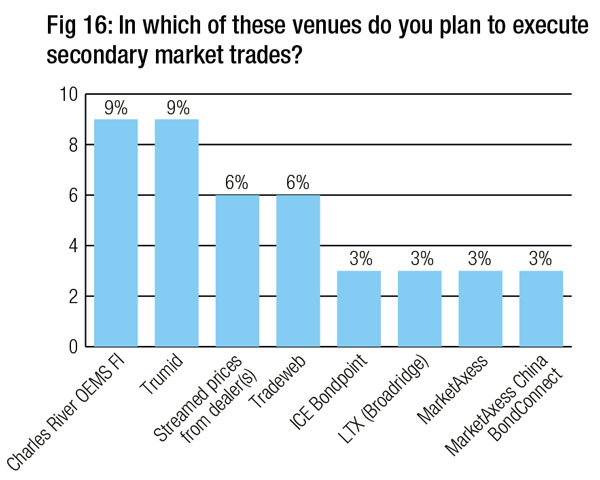

The pipeline for new adoption of execution platforms has a joint top space shared by Charles River and Trumid (see Fig 16). This is interesting – Charles River has been at the forefront of partnerships with trading venues, potentially allowing it be used for directly engaging with liquidity in those venues. Trumid has reported significant gains in market volume, and seems to have captured momentum.

The pipeline for new adoption of execution platforms has a joint top space shared by Charles River and Trumid (see Fig 16). This is interesting – Charles River has been at the forefront of partnerships with trading venues, potentially allowing it be used for directly engaging with liquidity in those venues. Trumid has reported significant gains in market volume, and seems to have captured momentum.

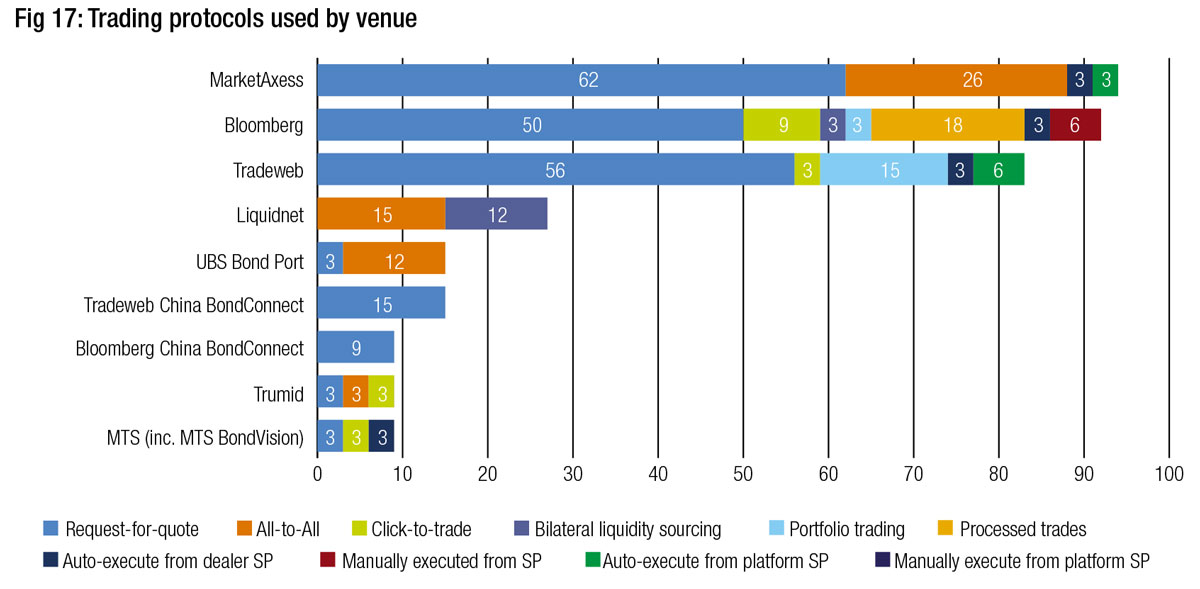

When we assess how firms are trading on those venues, it is apparent that streamed prices are increasing in activity via the platforms – perhaps rather than direct via dealers – allowing for a uniformity of delivery and execution (see Fig 17). Clearly request for quote execution is still leading the field as a preferred execution method, but each platform is championing new diverse ways of trading. Tradeweb clearly dominates in portfolio trading and has a good lead in automated execution. Bloomberg has a stronger case for bilateral liquidity sourcing, click to trade and manually executing against streamed flow, while 18% of trading is processed trading. MarketAxess is the all-to-all champion and is making comparable inroads into automation.

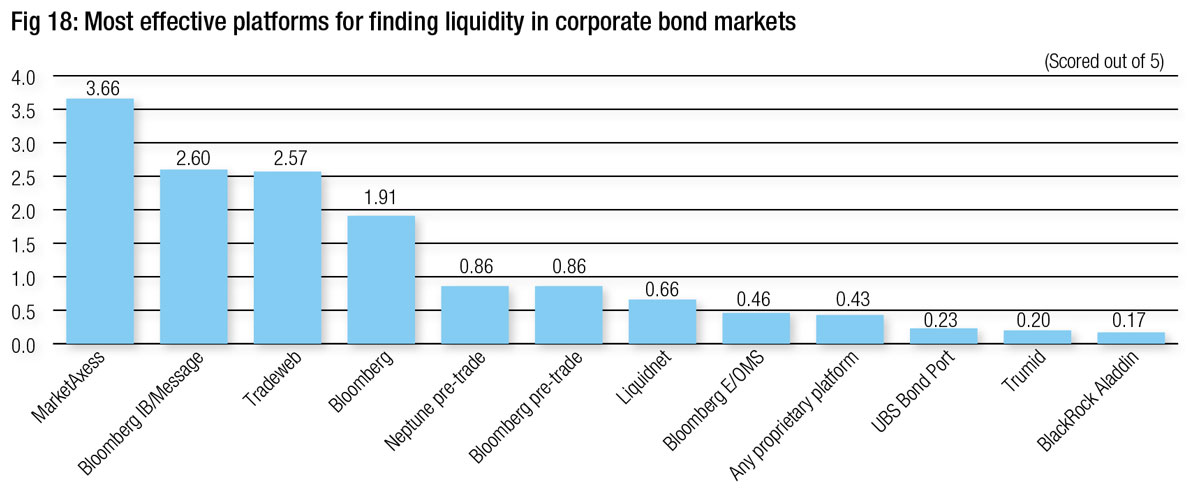

Ranked for effectiveness in finding liquidity, MarketAxess is the top choice for buy-side traders. Bloomberg’s messaging function and Tradeweb’s venue are ranked nearly equal for effectiveness, followed by Bloomberg’s trading venue (see Fig 18).

Ranked for effectiveness in finding liquidity, MarketAxess is the top choice for buy-side traders. Bloomberg’s messaging function and Tradeweb’s venue are ranked nearly equal for effectiveness, followed by Bloomberg’s trading venue (see Fig 18).

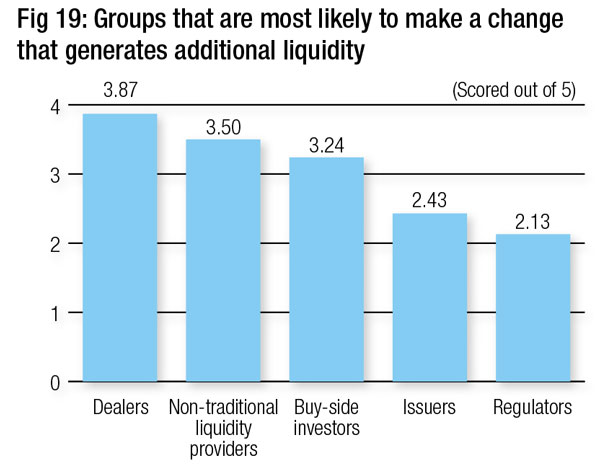

Generation of liquidity is seen to be in the hands of both dealers and non-dealer liquidity providers, followed by buy-side investors (see Fig 19).

Demographics

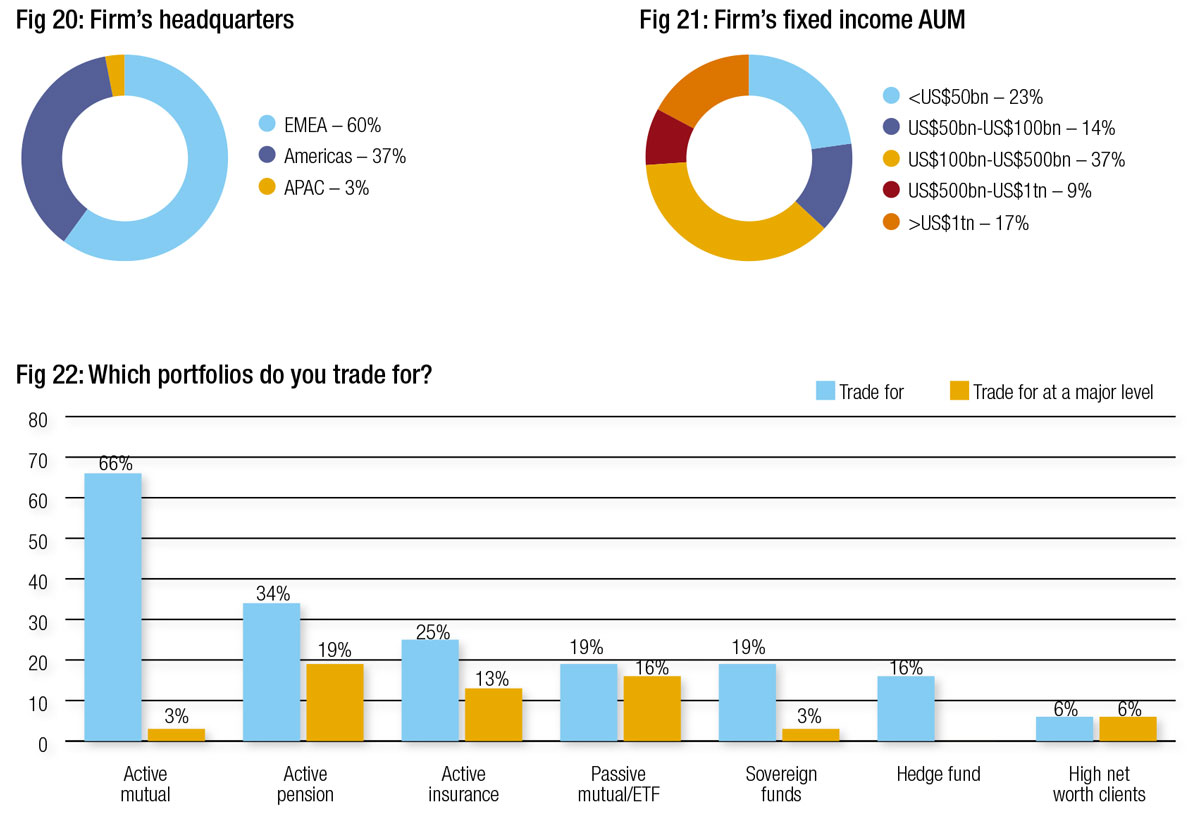

We survey heads of trading as well as heads of desk and traders and this can often mean a single respondent covers trading globally and is able to discuss trading across regions (see Figs 20-22). As a result, we cannot split geography by the country in which trading takes place by respondent.

To provide some differentiation between respondents, we ask them where their firm is headquartered, so at least we know the firm they trade for is based in APAC/EMEA/US.

We do ask for AUM for the firm, and the fund traded for, which tells us we have a largely active, long-only fund manager demographic, with a good spread of AUM coverage.

For more information on Neptune click here.

For more information on DirectBooks click here.

©Markets Media Europe 2023

©Markets Media Europe 2026

more valuable")