Covid-19 has triggered a “dramatic” shift in US Treasuries, the world’s largest bond market towards electronic execution from traditional voice trading, according to a report by JPMorgan Chase.

The figures from the Wall Street bank, one of the biggest Treasury dealers, reveal the corona virus accelerated a trend that was gradually occurring in the US government bond market. This is because many of the bank’s clients — who suddenly were forced to work from home in extremely volatile conditions — preferred to transact based on prices quoted on a screen rather than picking up the phone to negotiate with a human trader.

Over the past two years, roughly 50% of trading in the US Treasury market has been conducted electronically. However, the figure jumped to 70% in April, rising to 77% in June as traders became more comfortable with trading these products on screen.

Although the US Treasury market, which is the world’s most liquid bond market, has led the way in electronic trading, it still lags other asset classes such as equities and FX. For example, in the $6.6 trn a day currency market, estimates show that 90% of spot trading is executed digitally.

Anecdotal evidence shows that European fixed income volumes also went down electronic pipes, but it is further behind than the US despite the boost from MiFID II. Figures from a recent Greenwich Associates study – Uncharted Territory in European Fixed Income – show that electronic trading accounts for roughly 45% of the market.

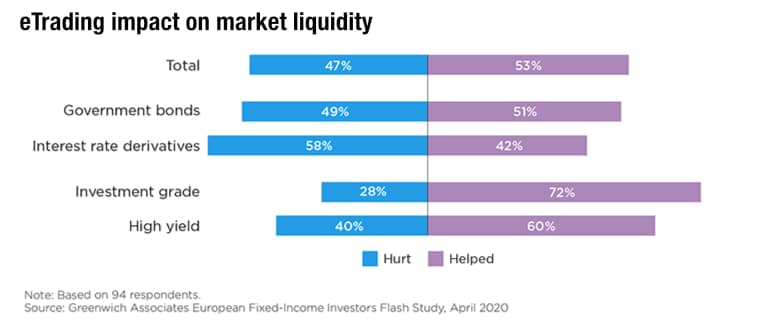

Market participants cited the main benefits of electronic trading – greater liquidity and transparency – were particularly important at the height of the volatility spikes in the first quarter. Traders were able to quickly gauge market depth on their screens, freeing time for more complex trades plus the costs for investors were lower. Estimates were that trades were about 10%-30% cheaper than conventional voice trades.

However, this was not the case for all segments of the European market, and in some cases, such as investment-grade corporate bonds, the volatility and illiquidity sent traders back to their phones, according to a new study from the International Capital Markets Association (ICMA) assessing the impact of Covid on trading.

It said this was due to the difficulty dealers and liquidity providers had in offering prices across electronic platforms. Some banks closed their algo trading completely at the time, while others opted to continue auto-quoting prices.

As a result, while digitalisaton may be the future, industry experts believe that for the foreseeable time, both electronic and traditional trading models based on dealer-client relationships will continue to co-exist.

©Markets Media Europe 2026

more valuable")