Emerging market (EM) sovereign debt stands apart from other EM asset classes, due to its exceptionally high commodity exposure. For several EM markets, with a high exposure to metals and oil, in the past year this has proven to be a characteristic that shapes both opportunities and risks for investors.

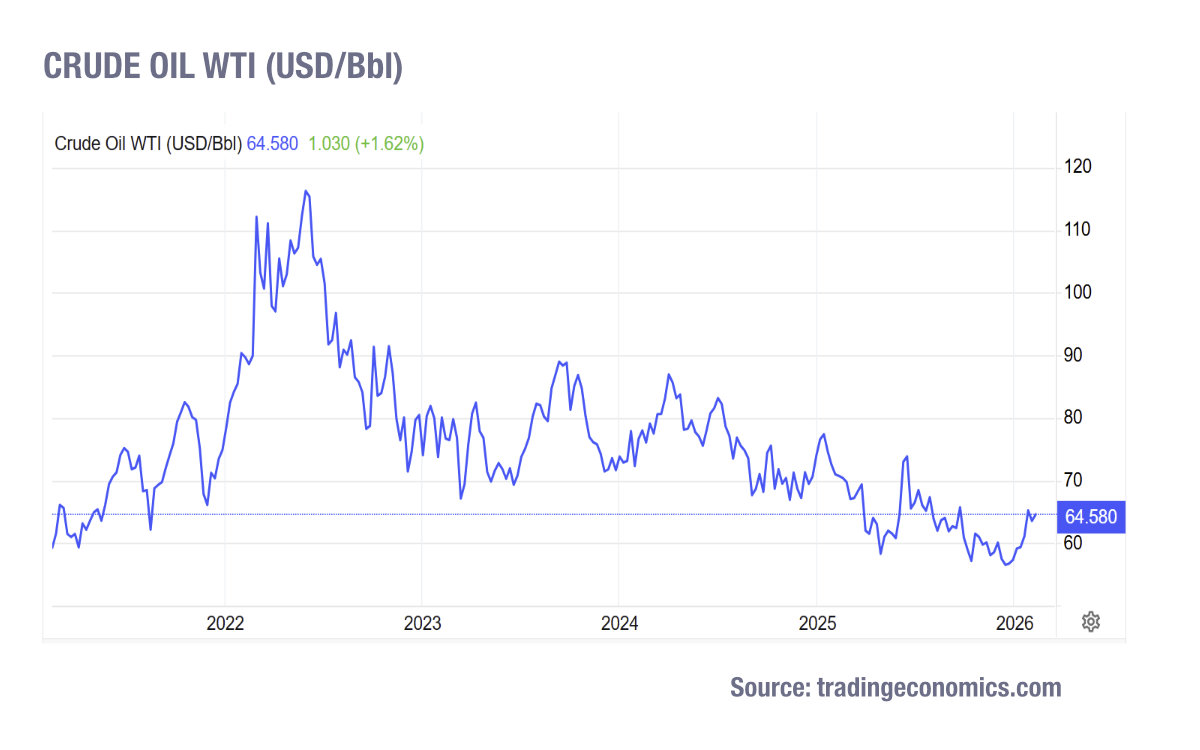

The multi-year rise of gold, silver and platinum prices, with a sharp wobble in the last week of January, along with volatile oil prices, are reflective of geo-political uncertainty.

“The rise in precious metals prices has boosted current account balances, reserves, and government revenues from taxes and royalties,” noted Magda Branet, head of EM & Asian fixed income at BNP Paribas Asset Management in September 2025.

Copper and lithium prices rose over the past year on the back of computer hardware and infrastructure development.

Movements in bond trading in 2026 showed a significant correlation with elevated commodities activity. In January, as major metal exporter economies such as Chile, Peru and Zambia, for whom metals represent double digit percentages of exports, saw volumes in trading over 20% higher than in January 2025, according to MarketAxess data. Interestingly, South Africa, a major gold exporter saw trading volumes drop 25% against the previous January.

Over the shorter term, sovereigns can see more volatile trading, with Chile debt trading jumping 58% In January 2026 against December 2025, a far greater move than seen in other markets.

The major oil exporters whose sovereign debt is most sensitive to commodity movements, according to Morgan Stanley, have all seen massive trading volume growth in January 2026 versus the previous year, for example MarketAxess data shows YoY jumps for Mexico (60.5%), Colombia (53.7%), Angola (22.4%) and Nigeria (16.3%). Exporters have historically issued more debt when prices are lower.

Buy-side bond traders building EM portfolios need to be aware of these potential impacts, and the effects on market activity.

“Higher gold prices offer EM sovereigns tailwinds from improved terms of trade and export growth, enhanced external buffers, and higher fiscal revenues,” write Sam McDonald, sovereign analyst, global sovereign & economics, and Devin Stewart, credit analyst, emerging markets fixed income at Pinebridge Investments. “Yet EM sovereigns should still balance diversification risks in their FX reserves; a sudden reversal in the gold price trend would lead to a deterioration in external buffers.”

For more thinly-traded EM markets, the sudden nature of these movements, exacerbated by ephemeral retail interest in metals and commodities trading, can create liquidity spikes and highly directional bond markets. Where price formation is sparse, or counterparties are limited, this will emphasise the need for better connectivity for EM investors seeking to optimise execution for speed, price and size of trades.

Understanding the effect of commodity dynamics on bond markets has become an invaluable aspect of EM sovereign investment, as commodity price volatility can influence credit spreads and investment outcomes. Equally, picking off opportunities in specific bond markets can require investors to cultivate dealer relationships and broader market access through electronic channels.

Not all that glitters is gold

Historical analysis reveals that while commodity prices are important, they function as secondary drivers of index-level spreads, ranking behind global risk factors such as US credit spreads, the VIX volatility index, and US Treasury yields. Within the commodity inputs, metal prices demonstrate significantly greater influence than oil prices on aggregate spread movements.

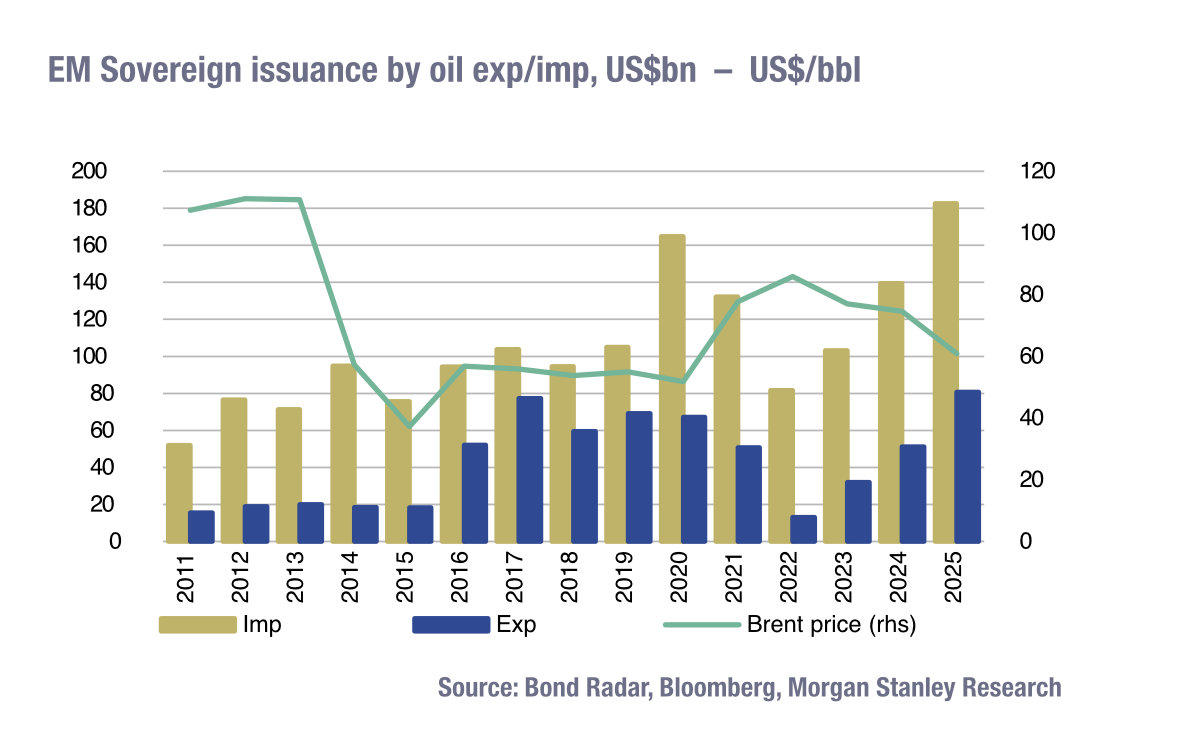

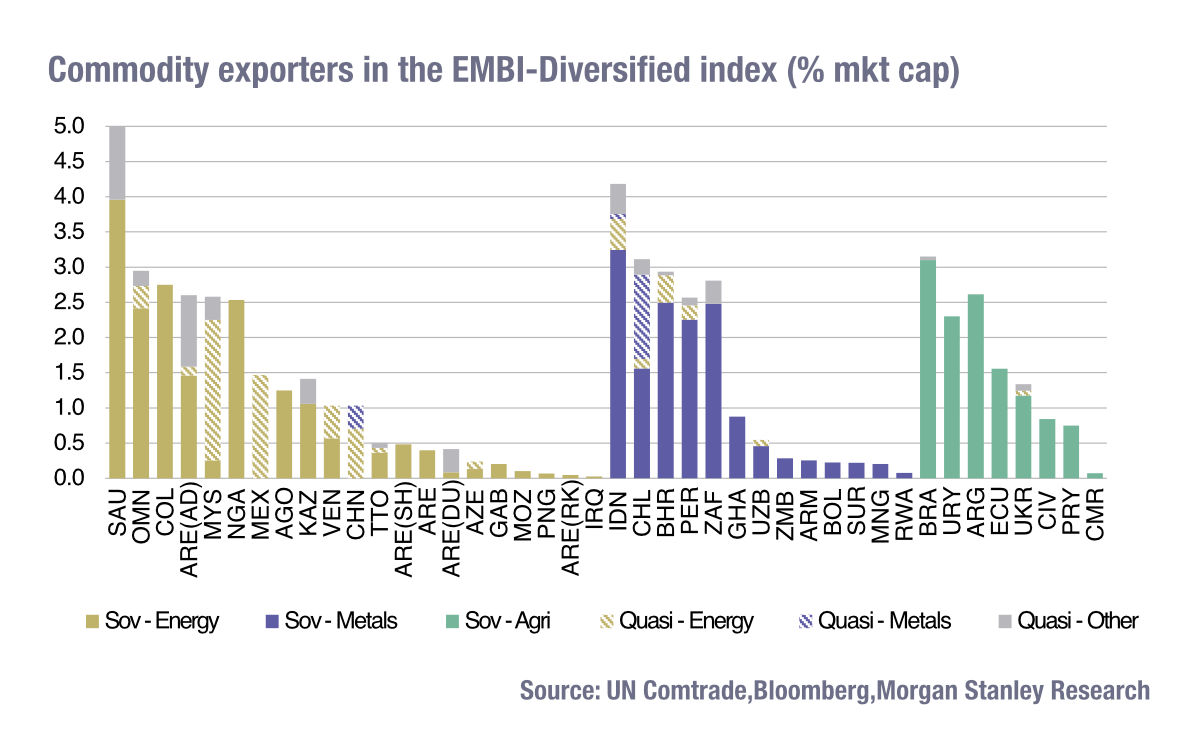

Yet, Morgan Stanley analysts estimate that 58% of JP Morgan’s Emerging Markets Bond Index Global Diversified (EMBIG- Diversified) components are “either sovereign or quasi-sovereigns issued by a country that is a net commodity exporter or by a quasi-sovereign that is a commodity producer in a country that is a net commodity importer (e.g. Mexican oil giant, Pemex).”

As a consequence, the bank notes, the index ought to respond positively to commodity prices moving higher on aggregate.

“We estimate 55% of the index as being countries that are net commodity exporters, with another 3% coming from commodity-related quasi-sovereigns in commodity-importing countries,” write Simon Waeaver, Neville Mamdimika, Emma Cerda, and Guru Sharan Agrawal of Morgan Stanley. “Energy exporters form the largest share of exporters at 24.5%, followed by metals at 18.4% and agriculture at 12.4%, yet there is often also overlap in the export basket. The commodity exposures come from both high-rated credits such as the Gulf Cooperation Council (GCC) region and low-rated frontier credits such as Sub-Saharan Africa, two regions that other EM asset classes have a much lower exposure [to].”

This has been key for EM investors in 2026. Metals have delivered strong performance, with analysts projecting further upside potential, especially for gold. Elevated precious metal prices also support EM sovereigns by positive support fro the pricing of reserve holdings.

“Most EM central banks follow the IMF’s guidelines and classify gold on fair-value accounting or mark-to-market basis,” note McDonald and Stewart. “Therefore, if gold prices rise in a given month, and assuming a stable exchange rate and no newly produced gold added to reserves, then functionally total reserves (which include gold) will rise. Additionally, the gold-producing countries can add to their holdings by weight. For example, the National Bank of Kazakhstan purchases gold from domestic producers in Kazakh tenge and then sterilizes the purchases afterwards with FX sales. Given that gold-producing countries tend to have higher shares of gold reserves relative to total reserves, these countries will see a disproportionate benefit from higher gold prices.”

What goes up

The combined boost from higher value commodity increases the buffers that exist for EM countries, which help from a credit rating perspective, by reducing the risk of default on hard currency debt, and for central banks to better manage economic stability. This makes continued inflows into EM sovereign debt likely as gold prices continue upwards, and sustained directional buying.

Yet the gold and silver price wobble in the final week of January, and the uncertainty of positive or negative outcomes from current geopolitical tensions could dramatically change demand for some commodities and have a corresponding impact on EM debt, likely triggering larger positional buying or selling in some markets.

After such a hefty climb, a drop of some sort is inevitable for some commodities if tensions reduce. These correlations, and the limited confidence in future outcomes, will make preparations on the trading desk – from enhanced data feeds to better trading tools, pay off in spades.

©Markets Media Europe 2025

more valuable")