The Philippine government’s overall borrowing programme for 2026 is set to remain broadly in line with 2025, but the composition is shifting in a meaningful way, which will likely impact access to, and cost of, liquidity in late 2026.

While the amount expected to be raised has risen only marginally, Manila is deliberately rebalancing its funding mix by lifting the share sourced from international investors from around 19% in 2025 to a targeted 25% this year, according to Morgan Stanley. That shift translates into gross external bond issuance of approximately US$5.3 billion in 2026, a sharp increase from the US$3.3 billion raised offshore in 2025, and underscores the country’s more outward-looking debt management programme.

“The bond market is small, especially in the corporate bond segment, with total bonds outstanding amounting to around 60% of GDP and bonds issued by the private sector amounting to less than 10% of GDP,” noted the Organisation for Economic Co-operation and Development (OECD) in it February report on the Philippine’s economy. “A package of reforms focused on strengthening corporate governance; streamlining equity listing and bond registration rules; and broadening the investor base would boost capital market development.”

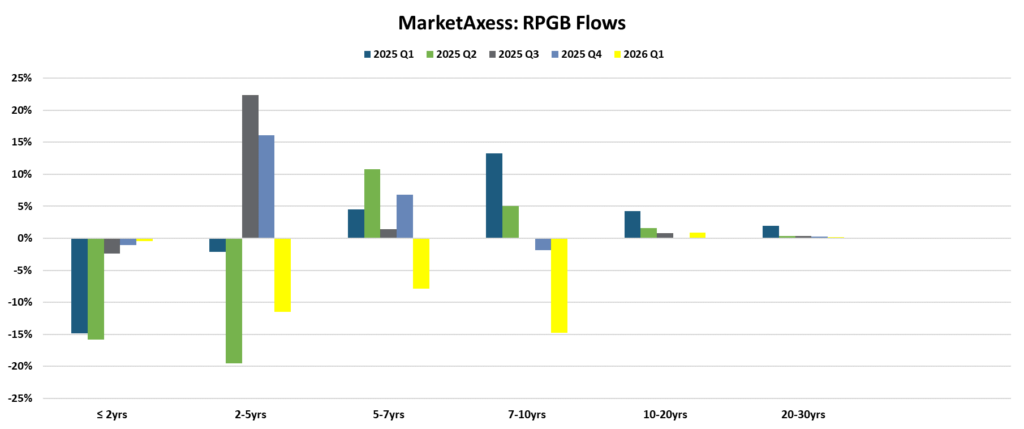

Electronic trading in Philippine Peso (PHP) bonds is already taking off, with MarketAxess reporting volumes up over 200% in Q4 2025 and a further 230% in Q1 2026, which has been supported by the constructive macro backdrop and expectations around potential inclusion into the JP Morgan’s Government Bond Index for Emerging Markets (GBI-EM).

Opening the gates to international capital supports a more diverse investor base, but will also broaden the range of investment strategies and priorities of investors, increasing support for two-way liquidity in the market. That ought to mean buy-side traders are able to source liquidity more effectively.

The strategic impetus behind the external pivot is not purely a financing calculation, however. Hovering in the background is the prospect of inclusion in JP Morgan’s GBI-EM index. JP Morgan placed Philippine peso-denominated government bonds on ‘Index Watch Positive’ status in September 2025, which is the final review phase before potential admission to the GBI-EM series. Given the typical six-to nine-month period for review, confirmation of inclusion was expected to happen anywhere after the first quarter of 2026, with any index changes likely taking effect in October 2026.

The implications for the Philippines’ liquidity profile are substantial and follow a series of changes that in themselves have supported market functioning.

“Key enhancements such as the availability of Republic of Philippines Government Bonds (RPGBs) via Euroclear, improvements in secondary market liquidity through the consolidation of benchmark tenors, the fine-tuning of the Primary Dealership System for Government Securities (PDSGS), the streamlining of Tax Treaty Implementation, the expansion of the GS repo market to include non-banks, and the launch of the Philippine Peso (PHP) interest rate swap market, have been viewed positively by global investors,” announced the Bureau of the Treasury in September.

Inclusion would be expected to attract more foreign investment as passive investors tracking the fund begin to pick up larger numbers of bonds, increasing liquidity and lowering borrowing costs for the government and eventually the private sector.

National Treasurer, Sharon Almanza, has indicated that an initial index weight of around 1% would translate to approximately US$3 billion in foreign inflows, though some analysts place the figure higher. Foreign ownership of Philippine peso government bonds has already doubled from 1.8% in 2021 to 5.2% as of mid-2025, equivalent to US$12.78 billion, partly driven by market reforms including the aforementioned revival of the repo market and the launch of a peso interest rate swap market.

For the Philippine bond market, the combined action of a greater external issuance programme and the structural shift of index inclusion, could prove transformative.

Greater foreign participation would not only deepen secondary market liquidity, but materially increase trading volumes and turnover, drawing the country’s domestic debt market into closer alignment with global emerging-market standards. The shift in borrowing mix is, in that sense, both a financing decision and a market development strategy, which will need to be factored in by the trading desks and investment teams at institutional investors.

©Markets Media Europe 2026

more valuable")