A new report by S&P Global has highlighted the systemic risks now posed to the financial markets at the point where bank and non-bank financial institutions meet.

Entitled ‘Systemic Risk: The Rise Of The NBFI-Bank Nexus Is Now The Top Risk’, it notes that the mitigation of risks by major global banks under pressure from regulators, and via systematically better counterparty credit risk management practices, helped by market infrastructure, still leaves indirect spillover risks.

“Banks and nonbanks share exposures to end clients or similar portfolios (such as sovereign debt portfolios),” the report notes. “As such, a sudden and massive deleveraging or forced selling by redemption vulnerable nonbanks could spread losses throughout the banking system – as happened at the onset of the pandemic during the so-called ‘dash for cash’ – or create a liquidity crunch for certain borrowers that hurts the real economy.

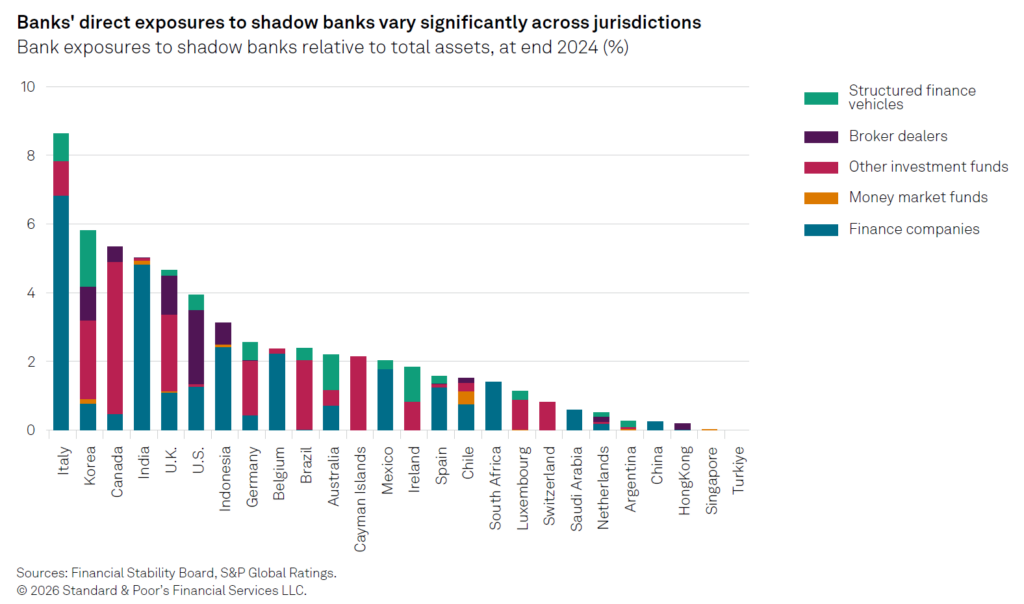

The scale and importance of shadow banks is most significant in funding economies of such as Brazil, Mexico, China, India, and Korea.

“In these countries, investment funds tend to dominate less, and fincos or broker-dealers play a significant role,” it notes. “In Japan, broker-dealers represent a material share of shadow banks’ assets and their activities have expanded recently, mainly reflecting the increase in short-term repo transactions on both the asset and liability sides.”

Shadow banks do not get access to central bank funding during market stresses, where banks’ holding of retail savings underlies a need for support.

“Systemwide funding stress can largely be explained by the vulnerabilities created by the bank/nonbank nexus, but they typically materialise only when funding conditions tighten,” the report authors note. “In our view, geopolitical risks pose the biggest risk to global credit conditions. Specifically, we believe the war in the Middle East might be the catalyst that finally pushes the credit cycle – and the prolonged favourable financing conditions – to turn. More broadly, fading economic dynamism may also test public and private markets’ resilience.”

It also cites market responses to investmetn in and disruption by AI models as potentially affecting markets, with private credit funds most heavily exposed.

“We believe that broader market confidence could be jeopardized if a nonbank were to fail, potentially igniting contagion,” the report concludes. “A run on an open-ended investment fund, for instance, could be seen as a sign of broader weakness in nonbanks and potentially banks, leading to bank runs and self-fulfilling expectations.”

©Markets Media Europe 2026

more valuable")