Two-year Treasury volatility has jumped in March, as yields rose rapidly, reflecting weakening confidence in future rate cuts being made by the US Federal Reserve in 2026.

Vishwanath Tirupattur, chief, fixed income strategies at Morgan Stanley wrote on 23 March, “We now expect that the Fed cuts will be delayed to September and December in 2026, versus June and September; the path for the Bank of Japan (BoJ) remains unchanged with hikes in June and 2027; European Central Bank (ECB) hikes in June and September, versus being on hold in 2026; Bank of England (BoE) stays on hold versus three rate cuts in 2026.”

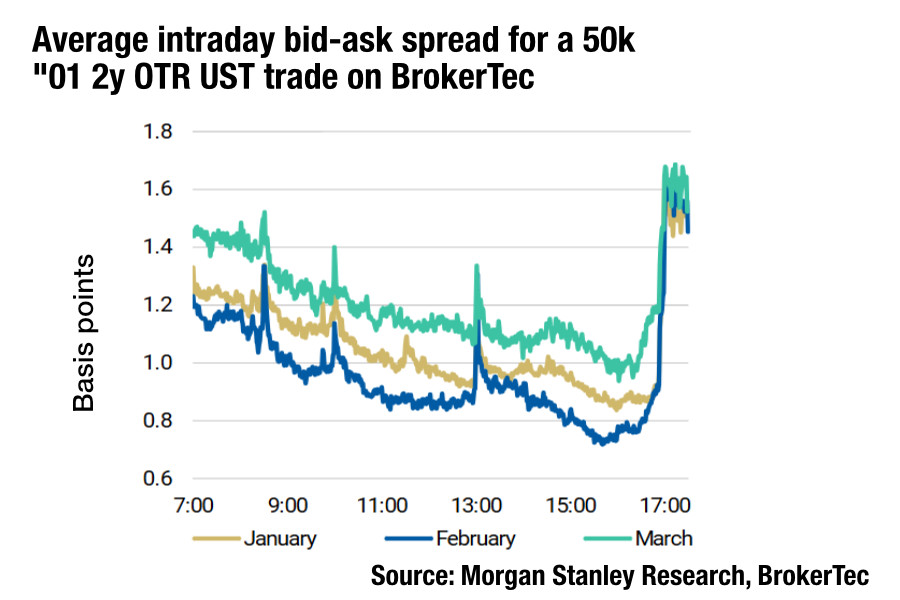

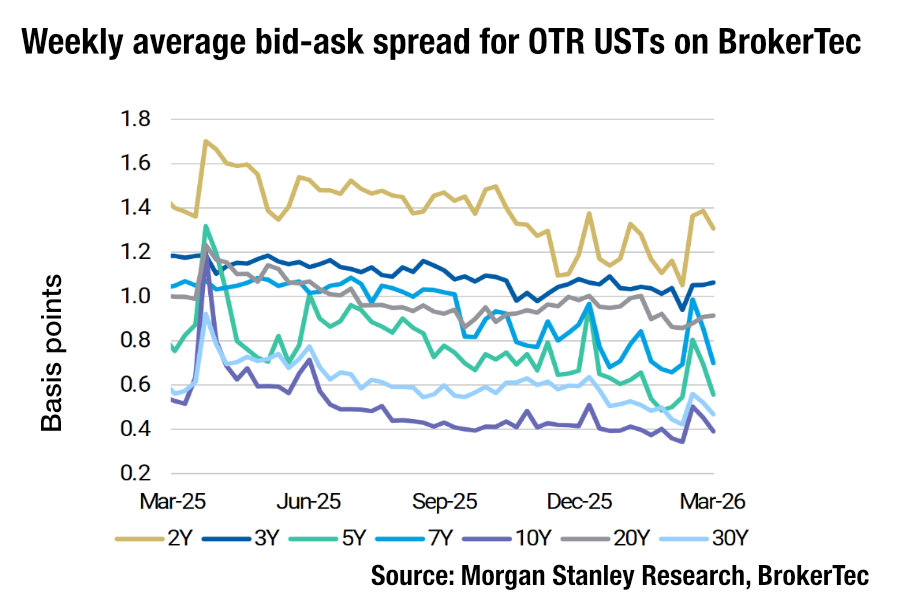

The increased trading costs were highlighted by Morgan Stanley analysts wrote in their report, “Treasury Market Liquidity in the Iran Conflict”, that bid-ask spreads in March have increased around 27% (approximately 0.15bp) relative to their February average, while bid-ask spreads at the long-end have stayed in line with February’s average.

The Morgan Stanley analysis used data from Brokertec, a dealer-to-dealer platform, but several buy-side traders have reported the increased costs of liquidity are being passed down to them in the dealer-to-client market.

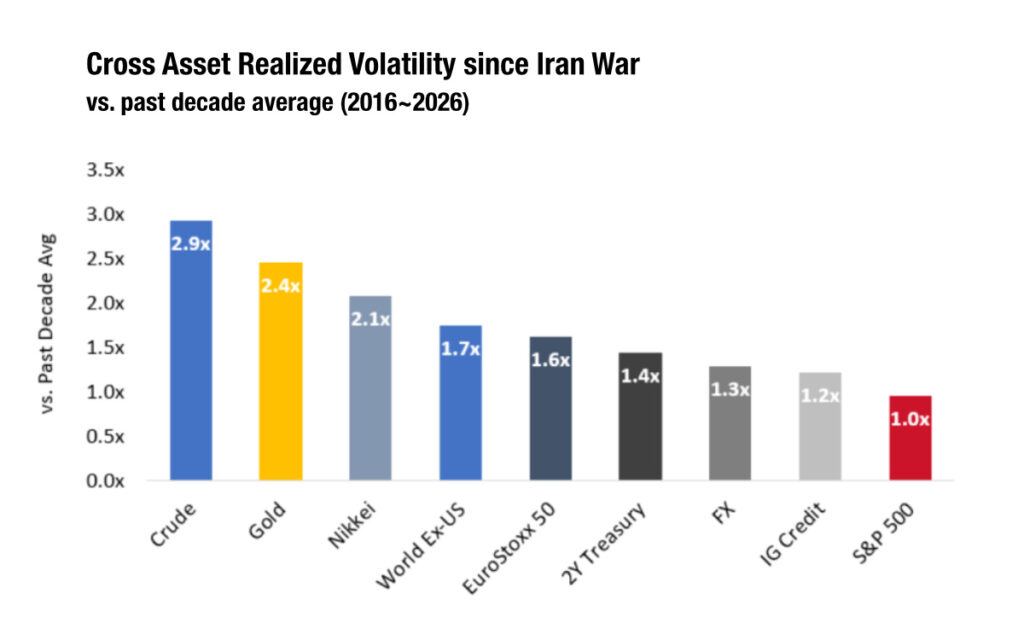

In the fixed income universe, 2-year treasuries appear to be the most volatile instruments, relative to their ten-year average, based on data from Nomura.

Although the costs of trading have increased, Luke Hickmore, investment director at Aberdeen Investments, notes the impact depends on the investment strategy in question.

“We’ve seen this massive pump up in 2-year yields, meaning strategies placing investments into 5- to 6-year to have a flattener on, have worked. If you are thinking about shifting back again [to the two-year] the bid-offer increase becomes a bit marginal,” he says.

Mark Capleton, rates strategist at BofA, wrote on 20 March, noted that, given the volatility, there is obvious scepticism about engaging in the market, but there is value to be had.

“Is it worth even trying to recommend a trade at the very front-end of the inflation market when pricing is as volatile as it has been?” he asked. “And won’t any market observations be out-of-date almost immediately? We think there are still useful things to say about cross-market inflation and real rate spreads at the front of the curve – things that look intuitively odd – without attempting to produce full-blown forecasts for inflation paths. And by considering cross-market trades, the volatility of such positions should be dramatically reduced, we would hope.”

Hickmore backs this point, noting that the right positioning is key, and increased trading costs depend on the

“If you’re worried about this crisis going on, and that might depend on the time of day, one of the things you want is more break-even spread, shifting into the 2-year gives you loads more break-even than staying out in 5- to 6-year,” he says. “Again, a little bit of increase in bid-offer in rates markets, if you’re a rates investor, is going to be a pretty big deal for you, but for credit, where I am, not a massive impact.”

Tirupattur favours stepping back from sensitivity to interest rate moves, writing, “We remain neutral duration in the US treasuries until we better understand the implications of the Iran conflict, both on Fed policy and – as importantly – fiscal policy. Similarly, for EGBs, we await specific catalysts such as geopolitical de-escalation, evidence that activity is slowing or increasing signs of impairment in financial markets. For UK government bonds, we close our long 30y ASW and turn short 10y ASW as the current backdrop should remain unsupportive for gilts.”

©Markets Media Europe 2025

more valuable")