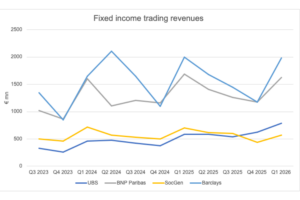

There are two rivalries in European banks’ fixed income trading revenues. Barclays and BNP Paribas are the heavyweights, sitting in the €1-2 billion bracket, while a closer competition plays out between UBS and Societe Generale in the welterweight class.

In Q1 2026, Barclays was the biggest hitter with almost €2 billion in fixed income trading revenues. The bank’s €1.98 billion represented a 68% increase quarter-on-quarter (QoQ), but a marginal 0.9% decrease year-on-year (YoY).

Considering widespread volatility over the quarter, group finance director Anna Cross confirmed, “We are very mindful of the environment around us, and that’s why we are managing risk and capital very carefully.”

She went on to explain that the bank has high operating leverage and absolute capital, increasing its resilience. “We got into this environment with a resilience that would not have been there a few years ago. We are operating with a greater proportion of our capital focused on more stable returns.”

“At this point, we don’t see any significant impact from the situation in the Middle East,” she added – but noted, “We’re a little more mindful of some of the investment bank exposures. We’ve put a little bit of downside into the investment bank calculation.”

In credit, “We’ve had no losses, or negligible losses, across all of this,” affirmed CEO CS Venkatakrishnan.

BNP Paribas, which has only edged ahead of the British bank once since Q3 2023, saw €1.6 billion in fixed income trading revenues this quarter, up 39% QoQ and down 3.4% YoY.

Commodities and currencies operations under the FICC umbrella were strong, chief financial officer Lars Machenil said during the bank’s earnings call, but highlighted less favourite primary and rates activity.

Machenil assured that its results were positive.

“The business had strong momentum, as you can see in the market share and the ranking gains. Particularly, if you look at India, we maintain our leadership amongst European banks with a 5.1% market share,” he said.

Lower down the weights, a tighter fight is going on between SocGen and UBS – although in Q1, UBS pulled ahead of its French competitor.

SocGen, meanwhile, reversed the downward trajectory it saw in 2025 and rose 31% QoQ to €571 million. However, this still represents an 18% yearly decline.

Group chief financial officer Leo Alvear explained, “[As] in previous quarters, we were impacted by our large weighting in rates [in] Europe. Lower revenues resulted from a high volatility, tight spreads environment, which limited our ability to monetise flows.”

On the broader corporate and investment banking decision, CEO Slawomir Krupa concurred on the reason for SocGen’s declining revenues. “[It’s] nothing else than simply market conditions which were particularly unfavorable to what is the biggest business we have in our mix.”

UBS reported €786.8 million in fixed income trading revenues, up 34% YoY and 26% QoQ.

Group CEO Sergio Ermotti used the firm’s earnings call to draw attention to a recent announcement from the Swiss government proposing an increase to the capital that banks are required to hold for certain assets.

“We continue to strongly disagree with the proposed package because it is not proportionate or aligned with international standards, and as importantly, [it] does not reflect the root causes and the key lessons learned from the Credit Suisse crisis,” he said.

All foreign subsidiaries of the bank would also have to be backed by CET1 capital.

“Regardless of how the figures are presented or which assumptions are applied, there is a broad agreement, including among the authorities, that the announced measures would require UBS to hold around CHF 22 billion in additional capital in CET1 terms. This is on top of the CHF 15 billion that we already need to hold as a result of the Credit Suisse acquisition under existing regulations. If the package were to be finalised as currently drafted, that CHF 22 billion of capital would be trapped and unproductive,” Ermotti argued.

©Markets Media Europe 2025

more valuable")