On 22nd July, 2020 a panel of market participants discussed the detailed implications of the Central Securities Depository Regulation (CSDR).

The panel comprised, J.R. Bogan, Senior Product Manager, Investment Operations Outsourcing EMEA at Northern Trust; Derek Coyle, European Custody Product Manager at Brown Brothers Harriman; Alex Duggan, Platform Head of Brokerage, Fees and Billing at Cognizant; Matthew Johnson, Product Management & Industry Relations at the Depository Trust & Clearing Corporation (DTCC); Philip Slavin, Chief Operating Officer and Co-founder of Taskize and was moderated by Lynn Strongin Dodds, Managing Editor of Best Execution magazine.

The European Central Securities Depositories Regulation was born out of the 2008 financial crisis and was designed to improve the efficiency and safety of securities settlement. More than a decade on, the CSDR continues to absorb time and resources and will become yet more burdensome as the anticipated workload includes reporting cash compensation management and workflows. Best Execution talked to leading industry figures to find out how organizations can move forward amid ongoing delays and changes.

Lynn Strongin Dodds, Managing Editor, Best Execution: We cannot ignore the impact of Covid-19. Do you expect any delays to the CSDR and what does the UK opt-out mean?

Derek Coyle, European Custody Product Manager, Brown Brothers Harriman: We received information from ESMA and other industry authorities, including Euroclear that they are considering delaying CSDR’s settlement discipline regime from February 2021 to 2022. This follows the Covid-19 impacts, including the heavy volume of trades and the market volatility from March and April. Industry forums like ICMA and AFME have also called for [Covid-19] to be considered. A delay is likely.

More time is welcome, but the CSDR must be implemented at some point. We will keep preparing and then await final confirmation, hopefully in the next month or two.

J.R. Bogan, Senior Product Manager, Investment Operations Outsourcing EMEA: There is an impact to the regulation, and to the UK saying it is not part of the regime, but there were enough issues with CSDR before the pandemic to justify a delay.

Strongin Dodds: Are fail rates, which were beginning to rise pre-pandemic, expected to increase this year? Are firms getting their houses in order?

Matt Johnson, Product Management & Industry Relations at Depository Trust & Clearing Corporation (DTCC): Firms are preparing, but there is always more to be done. The broker dealer community appointed large, established project management teams that looked at internal processes front to back, which engaged the front office because of the expensive penalties.

If you had asked at the start of this year whether the buyside was ready, I would have said absolutely not; they were still asking fundamental questions which rang alarm bells. Trade associations like the Investment Association (IA), the Association for Financial Markets in Europe (AFME) and International Capital Markets Association (ICMA) have done a fantastic job in getting members up to speed.

The DTCC saw unprecedented volumes across their confirmation and affirmation platforms. The US had record volumes, with nearly 3.3 million trades in one day across Tradesuite and well over a million on Oasys. Global platforms such as CTM saw record volumes at the end of February, with around 1.2 million transactions in a single day.

When volumes increase, fail rates tend to creep up. It could be because banks and buyside systems were creaking, or because they struggled to handle the volume. After Covid-19 hit, pretty much 98% to 99% of people were working remotely. That caused some problems.

J.R. Bogan: Firms are prepared, and if they are not, they should be. SSI storage engagements, how you interact with your matching utilities, and how you track and manage your fails process must be done more efficiently and effectively because the regime includes extra layers of information to gather and understand. If you clean up your own house it will help ensure that if things do fail, it’s not your fault.

Philip Slavin, chief operating officer and co-founder of Taskize: Most of our clients developed a two- pronged attack. First, focus on improving the settlement efficiency of your core business: Second, work to meet your obligations under the new regime for penalties and buy-in processing.

If you look at settlement efficiency, much effort goes in to increasing rates of straight through processing (STP). Depending on which product you’re trading or the region you’re trading in, rates of STP can be high. Nevertheless, independent estimates say that up to 60% of the total cost of operations is made up of people, who are a relatively low-cost unit of resource. Sometimes automating, or investing in the automation of something, goes against the cost model; it may be simpler and more cost effective to just use people to solve the problem.

So, if you improve human efficiency by a few percentage points, you can make a huge difference to the cost base of your operating model, which is a focus for Taskize. We look at how people collaborate and resolve issues more efficiently.

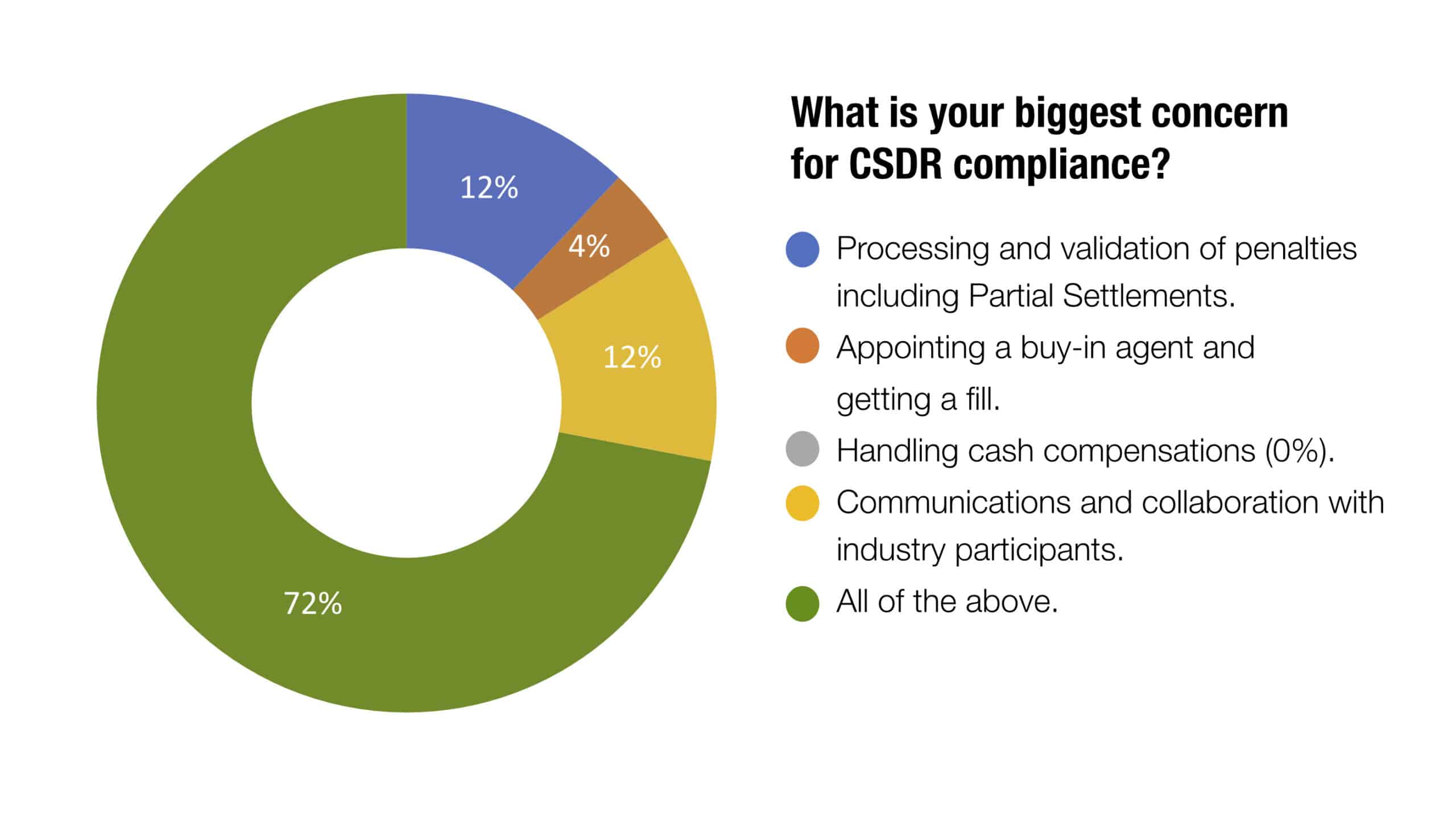

Audience poll

Strongin Dodds: How do you source and validate data?

Alex Duggan, platform head of brokerage, fees and billing at Cognizant: The data relating to CSDR is one of the most complex pieces of the puzzle that people need to solve. People need to understand the closing prices, the ISIN data, the eligibility, whether the security is liquid or illiquid. There are multiple CSDs which could have different solutions. People need a centralized view to support this. They need this data in their pre-matching fails management processing. First, so that they can understand the prioritization of the trades that are outstanding or failing; second, they need to understand the cost of the penalties that are coming in. They also need to be able to reconcile those versus the charges that are coming in from the CSD, and equally they need to be able to dispute those and accrue them so that their businesses can understand the costs that are going through and can prioritize accordingly.

People have multiple referential data systems and legacy platforms alongside different fails and inventory management tools, and stock loan collateral management tools. It’s a very big ask to build that into legacy architecture. We are looking at how we can develop a centralized data hub.

Coyle: Custodians are central to how the data flow will look with a lot of data coming from so many various points. There are 31 countries in the CSDR scope – 30 if you count the UK choosing not to apply the Settlement Discipline Regime – and beyond that, you might have multiple connection points with multiple CSDs. Our first challenge as custodians is to bring all that together. We are going to rely on certain databases, like the European central database that is hopefully going to be the reference point that provides details on securities in scope and the liquidity stages of those, so that when penalties are being measured, they are measured against that by all. Our task is to bring all this data together, balancing the effort of validation with the need to pass data on to clients as quickly as possible, so they can do their own validation and processing.

Slavin: There is definitely a data problem. Data is the oil lubricating the wheels of operations; the better the data, the better the operations. But when a trade fails not all your data needs to be shared to resolve what’s broken. So you need to ask how much data you feel comfortable sharing? Sharing important data may amplify your business or impair it?

Strongin Dodds: How should partial settlements be dealt with? How do market participants focus on reducing the financial impact of fines and penalties through proactive settlement workflow and reporting?

Coyle: First, consider penalty determination and assignment. There are two classifications of penalty that can be reported or determined: late matching and settlement failure.

If a trade failed for four days past intended settlement date, depending on when that was last touched in the process, you could end up with different responsibility and ownership. There could be different permutations within those four days. Let’s say two days of late matching penalty and two days of settlement failure penalty. It will be a challenge to determine responsibility and try to settle based on those timestamps and touchpoints.

Partial settlements are key because no matter how much we talk about the settlement discipline regime and the impact of penalties and mandatory buy-ins, there is a carrot and stick approach here.

The stick hits you with penalties, with buy-ins on top of that. The carrot encourages businesses to settle as much as possible in advance, using STP and best practices, and allows for as many partial settlements as possible.

We’re focusing our efforts now for operational readiness for some of these messaging flows and designs.

Bogan: The issue with partial settlements is how do I know it’s happened, and will it be consistent across all the CSDs? Who do I chase for information? I want there to be certainty around what I think is a failed trade, and to have direct communication of when a trade has partially settled because it minimizes the risk overall.

Another issue is penalties and the thresholds we can used to claim back penalties from other counterparties. It’s likely that lots of small pots of money will accrue and may be lost if they cannot be claimed back on a transactional basis. How is that going to work in practice? That needs to be looked at.

Duggan: To reduce the impact of fines and penalties, looking at it front-to-back is key: the trade booking, referential data, people’s stock loan collateral and inventory management processes.

Regardless of any further delay, firms have already focused people and budgets so they should continue that journey. More and more people are looking for long-term cloud and digital solutions with a single, central view of their fails management because, ultimately, CSDR is part of a global fails management process and not standalone.

What they need is a solution that offers real-time workflow and SWIFT messaging updates, buy-in workflow and claims management, the ability to calculate penalties on a real time basis, use mark to market risk prioritization in their day-to-day work, and have real-time flexible dashboards that offer predictive analysis on what’s going to fail, what’s failed historically, where is the biggest risk. And not just from a trade level but from a net settlement position too.

That gets them to 50%, where they can look after themselves internally and demonstrate compliance, but it’s market interoperability and collaboration that gets you the extra mile. You can only resolve if you’re able to deal with your counterparty, your market participant, your custodian, or your outsourced provider.

Strongin Dodds: Is it front and middle offices that need to take the most responsibility for collaboration? Can client portals help with the resolution of disputes?

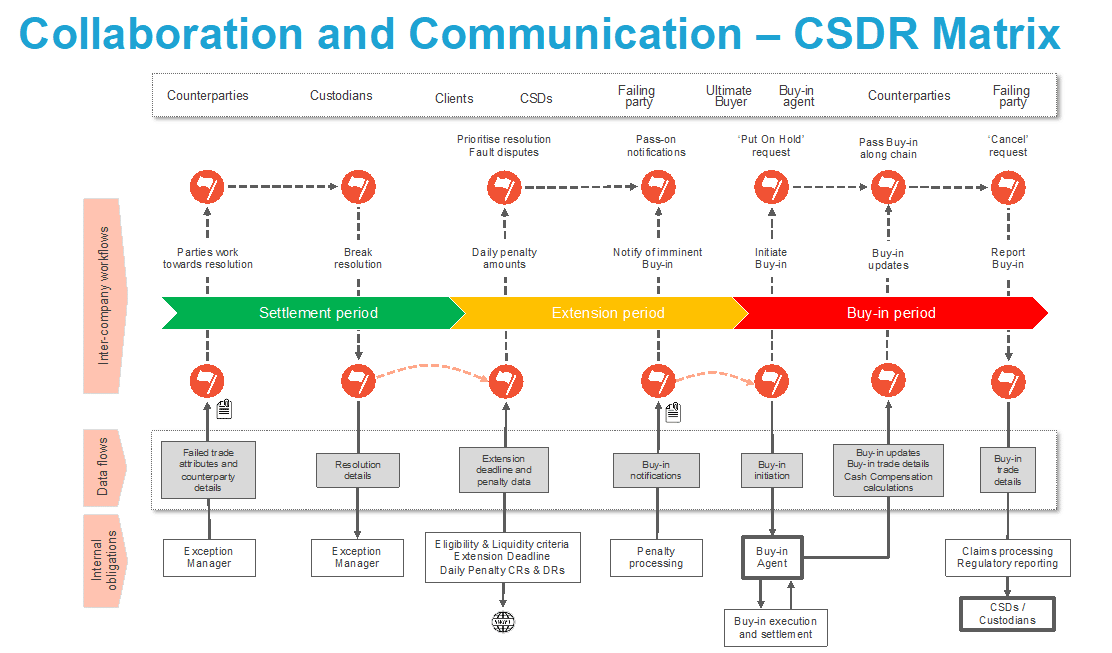

Slavin: The diagram (above) summarises the areas firms need to consider when looking at CSDR settlement efficiency and new obligations for penalty processing and buy-ins [bottom row]. Business decisions on internal solutions must also consider how to collaborate with clients, counterparties, or service providers to make sure that all parties are kept informed during the resolution of the failed trade or any subsequent buy-in.

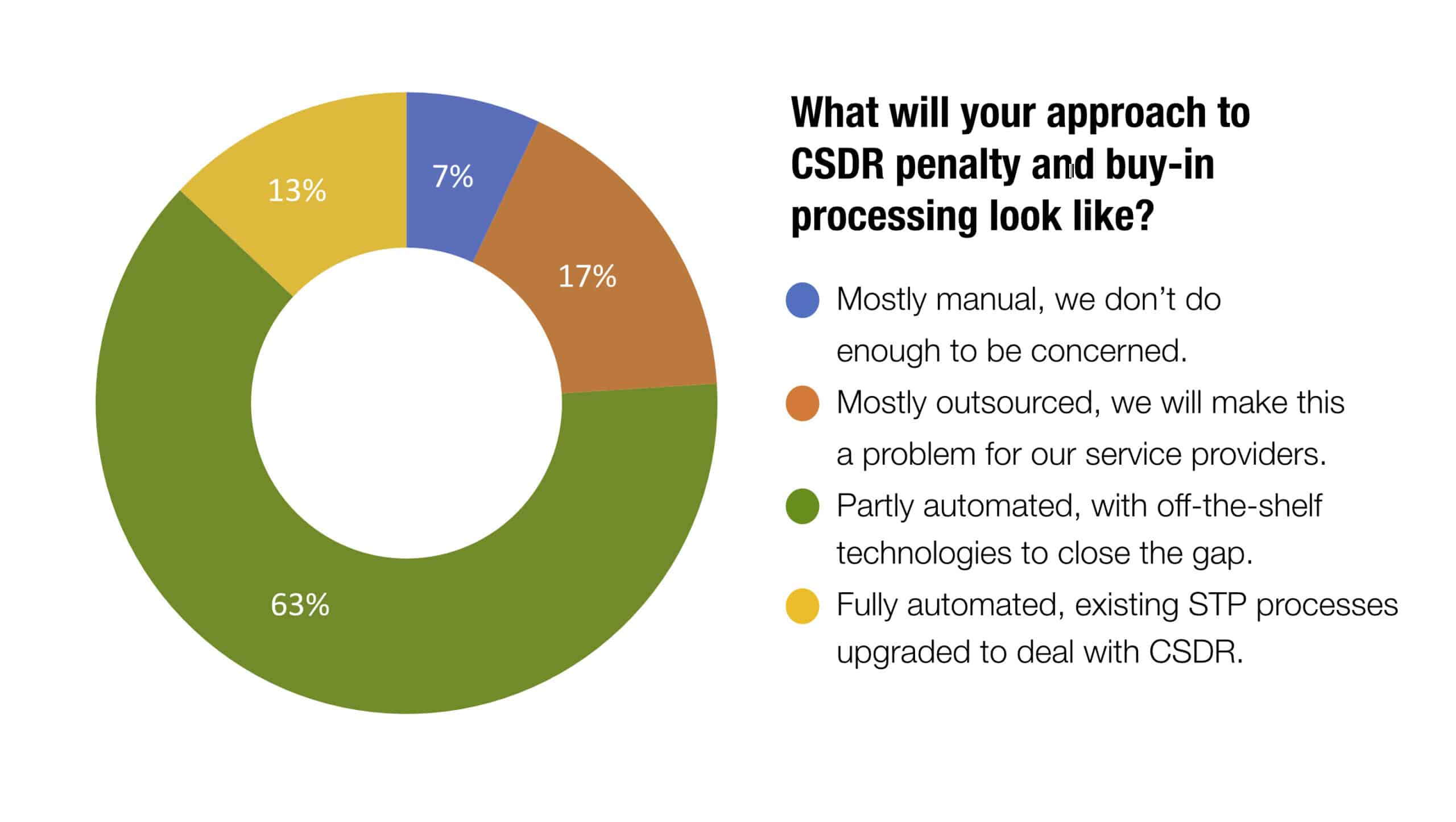

In today’s audience poll, 17% believe the process will be fully automated, but we know some organizations are not SWIFT enabled or have such low volumes they can’t justify the investment required to take the new SWIFT messaging. Importantly, SWIFT doesn’t support some of the notifications required. We need alternative platforms able to support the human to human interaction.

Organisations need collaboration and specific inter-company workflows should guide participants through the process so they meet their obligations. This will be second nature for businesses with high volumes, but for those with low volumes, or who are fully manual, they need to do the right thing in the right sequence. Each organization must pick the capabilities they need and integrate them with their own internal capabilities which relies on platforms having open architecture.

Everything has got to work together, whether it’s internal (below the coloured line in Fig. 1) or with other 3rd party systems.

Duggan: With the model that people have nowadays spanning many systems, many countries, different outsource providers, e-mail isn’t going to be optimal. When it comes to issue resolution, the actual generation of the query needs to be automated. Any communication then needs to be populated with the core information that’s required and then sent out to the relevant parties to be resolved by the appropriate person in the in the market. And I think that’s key.

There’s going to be a lot of disputes, a lot of questions from the front offices. You’ll need a centralized audit trail of data and communications, one that shows the timings of everything that happened on that transaction so you can demonstrate compliance to the regulator, to your internal auditor, but more importantly to your client or to your business.

Strongin Dodds: What is the sequencing of events and approach for buy-ins? What is the downstream impact for the buyside and how will panel members handle cash compensations?

Bogan: First, you have to know you’re going to get fails, then you have to be able to discern what type of fail it is. Then you have to chase it and that’s the point around collaboration. We’re going to have to be a lot more succinct in dealing with our counterparties around why a fail isn’t getting to a resolution a lot quicker. Once your ISD plus four has come up, you have to think about the buying agent. Then there’s the question of pre-notification. So, you’ve made the decision to buy, do you have to tell the person?

And then you have to worry about the execution and then the instruction. There are so many different elements in the chain that need to be worked on, and these can not only be different for each firm but different depending on how you interact with your counterparties.

Coyle: There’s also the question of who is at fault if the transaction has reached a buy-in. Who takes responsibility for additional buy-in charges? If there are price differentials, then there’s already a discussion – depending on which way the price goes – would that end up in a kind of claim process or will it be settled as part of that overall charges approach?

It’s complicated.

Johnson: As it stands, there is only one buy-in agent and if you look at it purely from an onboarding perspective, we’ve got about 3,000 buyside firms across Europe that need access to an agent. They need to onboard at a fund level – and they could be managing upwards of 200 to 300 portfolios. There are probably just not enough man hours to do that.

Who owns the buy-in process? Is it middle or back office? Is it price discovery, do firm’s view it from that angle or is it just a way to get the trades settled in the middle office?

I totally agree with Alex about the need for real-time data. If the front office is going to be initiating the buy-ins to the agent, they’re going to need to know exactly what and when to buy-in. If all they see is the fully executed position of the failed trade, they don’t see what’s been partialled, and without that information they could buy-in too many bonds or too many shares and that can obviously lead to liquidity funding issues and all sorts of operational issues.

Audience Poll

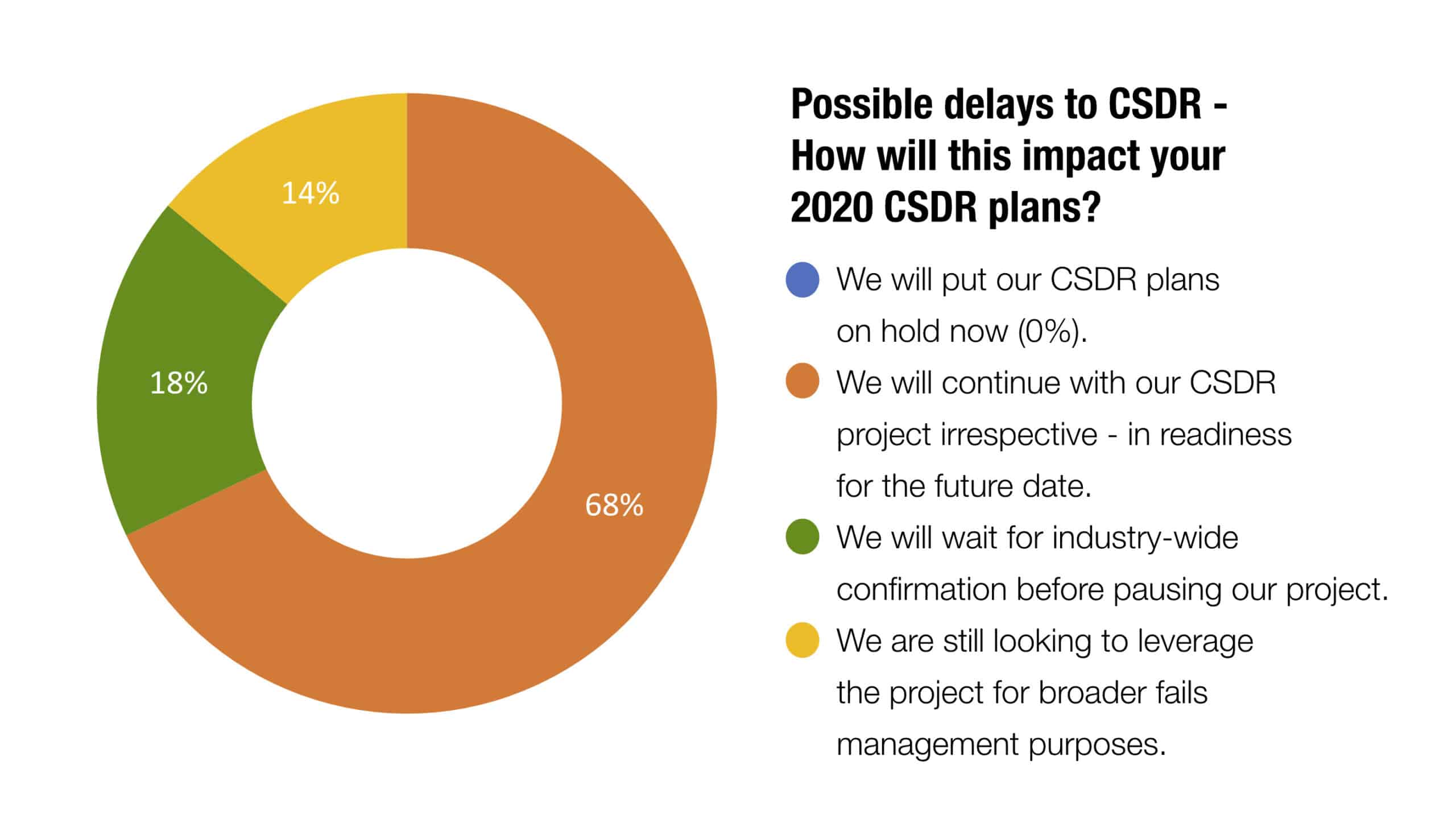

Strongin Dodds: What are your final thoughts on the CSDR delays?

Coyle: We know where the delays will impact operations in terms of flows and processes. Look at building out the project designs and then naturally reach into the connection points, whether upstream or downstream, and talk about those flows. Those data connection points and those communication channels are going to be key in terms of being ready.

Slavin: Everybody seems to understand the delay does not mean ‘stop working’’. The focus should be less on how to manage penalties and buy-ins as there is now more time for the regulation to evolve. However, the settlement efficiency projects should continue at pace.

Duggan: People recognise they must interoperate and collaborate, and the pandemic has reaffirmed this. There is also a recognition that the legacy architecture that most people have isn’t the full solution that can get them to where they need to be to mitigate and reduce the impact of the regulation. Having a single workflow in a centralized place which can give you real time updates and interoperate with the market is going to be key.

Bogan: The whole industry has got to change and work with this. If it’s not standardized and it’s not general best practice, then you’re going to have divergence of thought on how something can be done. Firms must have their houses in order and understand what’s going to go wrong in order to limit the impact of CSDR.

Johnson: It comes down to accurate data, for example making sure that SSIs are in the correct formats and in the correct place. Automation or creating no-touch workflows will reduce problems and failures. For the buyside, it’s about onboarding into buy-in agents and understanding who owns the buy-in process and whether they can handle the volume of buy-ins that will potentially come their way.

Audience Poll

To view the webinar online please click the image:

Kindly sponsored by:

![]()

©Markets Media Europe 2025

more valuable")