New platforms and late bloomers are all seeing greater interest.

This year buy-side desks have a renewed vigour for investing in trading tools, with far higher proportions of traders planning to onboard new platforms and data sources than in 2021.

There are green shoots as several fintechs show steady growth in their small but engaged user bases, and we see great appetite and growth for both new and third generation trading venues. The big four trading platforms – Bloomberg, MarketAxess, Tradeweb and Liquidnet – are all clearly proving the value of their existing tools and still innovating in the face of mounting competition.

Direct price streaming from brokers has captured a lot of interest from many buy-side desks yet there has been little significant growth in the firms using it this year, while auto-execution on streamed dealer price via platforms has made notable progress. We also see auto execution against platform prices taking steps forward. While portfolio trading is not commonplace on platforms, 6% of traders report that portfolio trading is their preferred protocol for use on Tradeweb.

Bloomberg leads as the most used source for pre-trade data, trading interface and preferred trading venue for both primary and secondary markets, and its ongoing efforts to improve service quality and smart use of natural language processing (NLP) appear to be reaping dividends.

That said, MarketAxess is once again seen as the most effective of tools at finding liquidity and has joint lead with Bloomberg in use as a secondary markets venue, with Bloomberg having a slight lead in the number of major users.

Given this tough competition between the major incumbents, a consistent annual performance from Liquidnet and UBS Bond Port, and the rising stars of Neptune, LedgerEdge and Trumid nipping on their heels, it is clear that 2022 will be an exciting year for fixed income market structure.

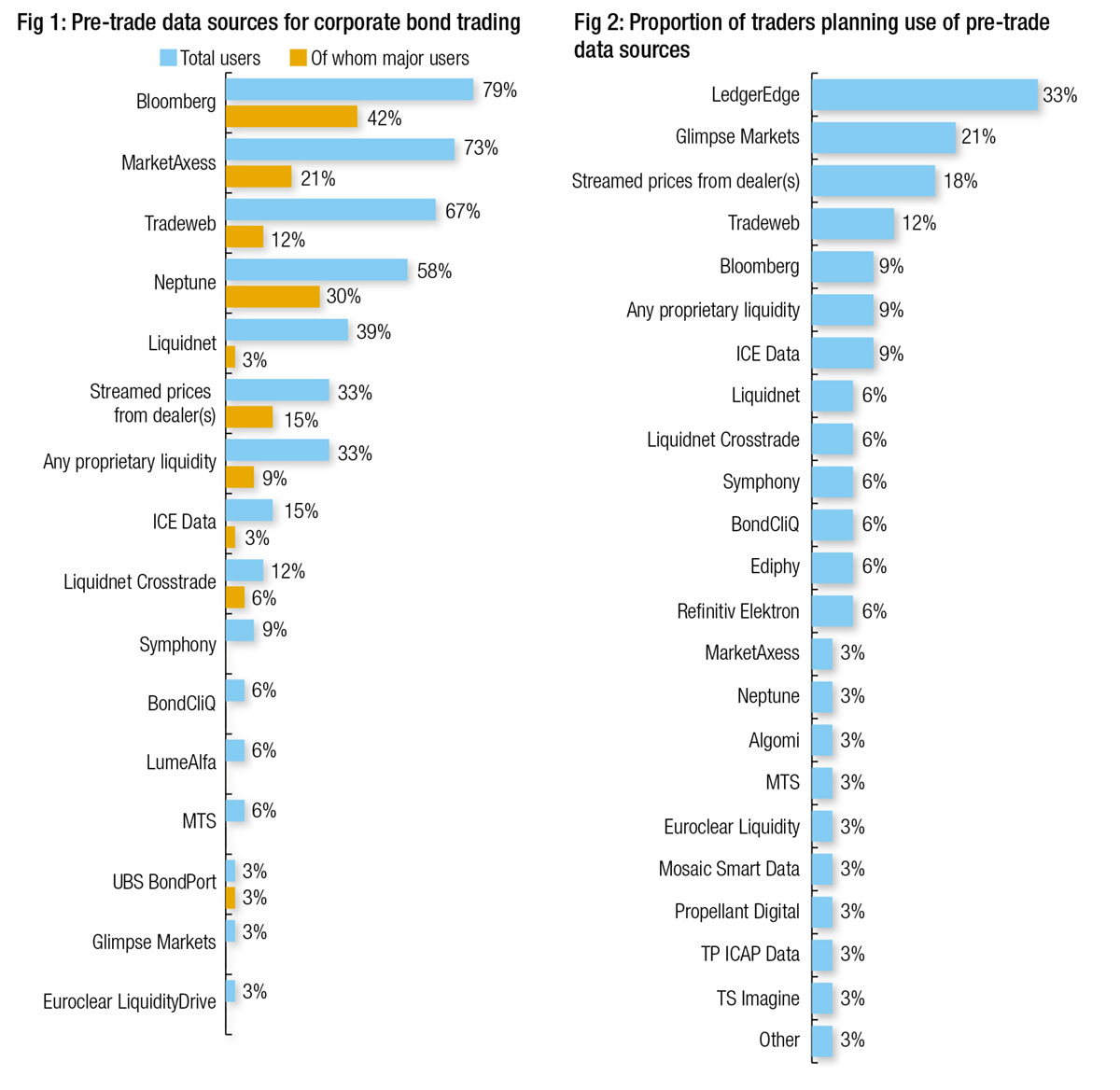

Pre-trade data

Pre-trade data provision has seen a rebalancing between the major providers, with leader Bloomberg overall use falling back slightly on 2021 – albeit with a slightly higher proportion of major users – while MarketAxess and Tradeweb both saw growth (see Fig 1).

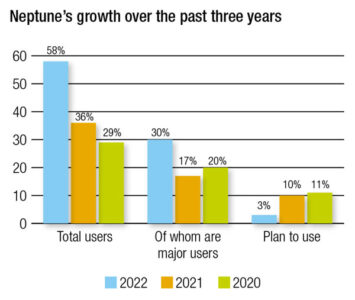

The biggest story here is Neptune – 58% of buy-side firms reported using it up from 36% in 2021, and 30% now view themselves as major users, up from 17% in 2021. Other numbers were relatively stable, with fintechs including Symphony, BondCliQ, LumeAlfa (formerly Algomi) and Glimpse Markets showing positive expansion although still in single figures.

Looking at the pipeline for new business, LedgerEdge is clearly on a tear with 33% of respondents planning to use it for pre-trade data in future (see Fig 2). Glimpse also has a solid platform for 2022/23 with 21% of firms planning to engage with it as well. Direct price streams have increased in popularity with a pipeline of 18% over 2021’s 10% and Tradeweb has retained its 12% pipeline as a pre-trade data provider from the previous year. Overall the appetite for onboarding new pre-trade data tools is far stronger than last year’s.

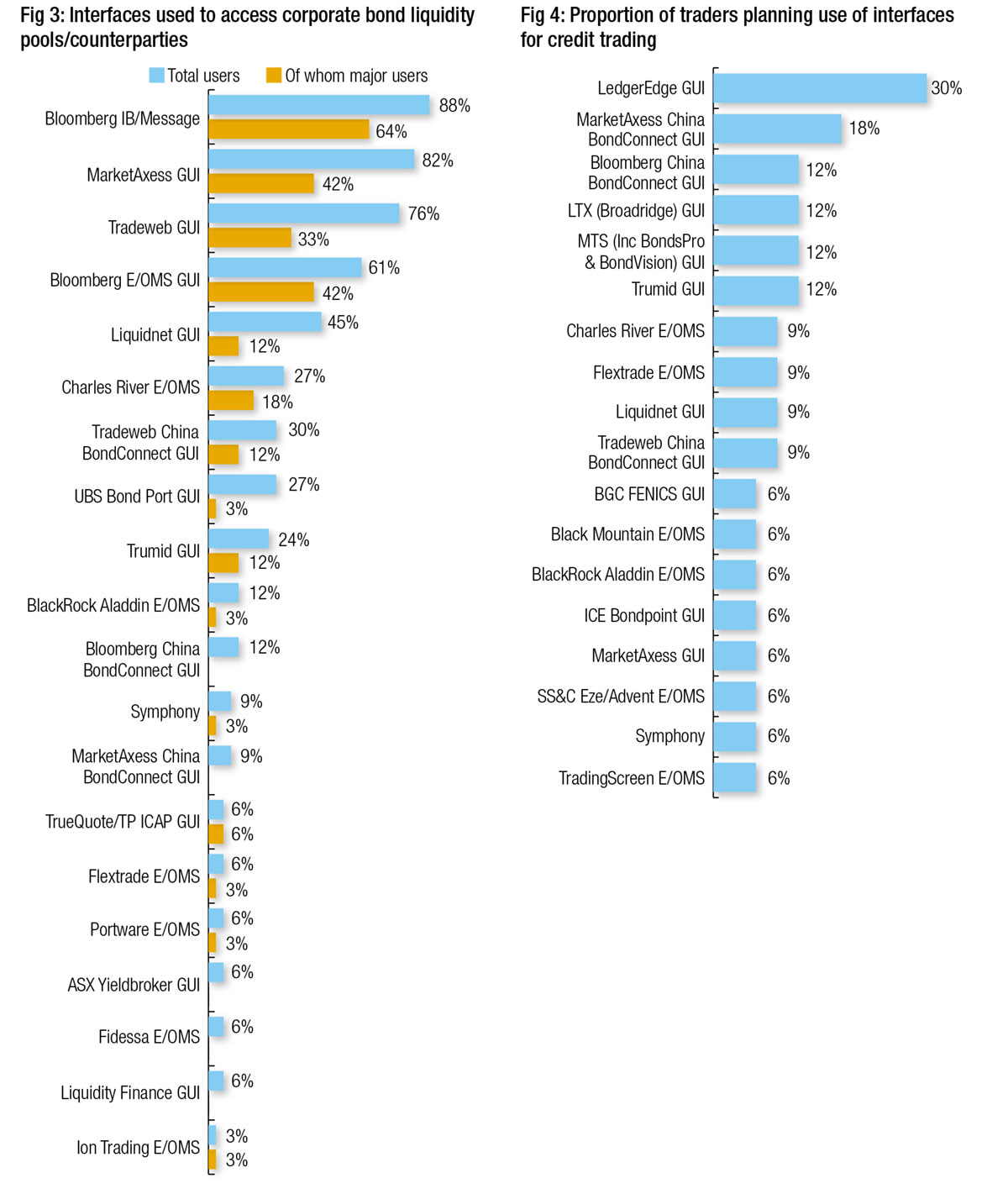

Trading interfaces

Bloomberg IB/Messaging is still the primary interface for traders and has seen the proportion of traders considered ‘major users’ grow by nearly 30% this year. Bloomberg’s E/OMS tools also grew not only in users but in the level of major users, which increased by 15 percentage points.

MarketAxess and Tradeweb GUIs both increased the level of use, the latter by 15 percentage points. On the E/OMS side Charles River really stood out for growth, with the rest steady at around 6% market share.

Looking ahead at future intended use, again LedgerEdge has nearly a third of trading desks in its sights as prospective clients, having had none reporting intent in January 2021.

Electronic interfacing into China’s markets is making both MarketAxess’s and Bloomberg’s China BondConnect platforms desirable, while we again see a much healthier interest in onboarding new GUIs for the year ahead across E/OMSs and platforms.

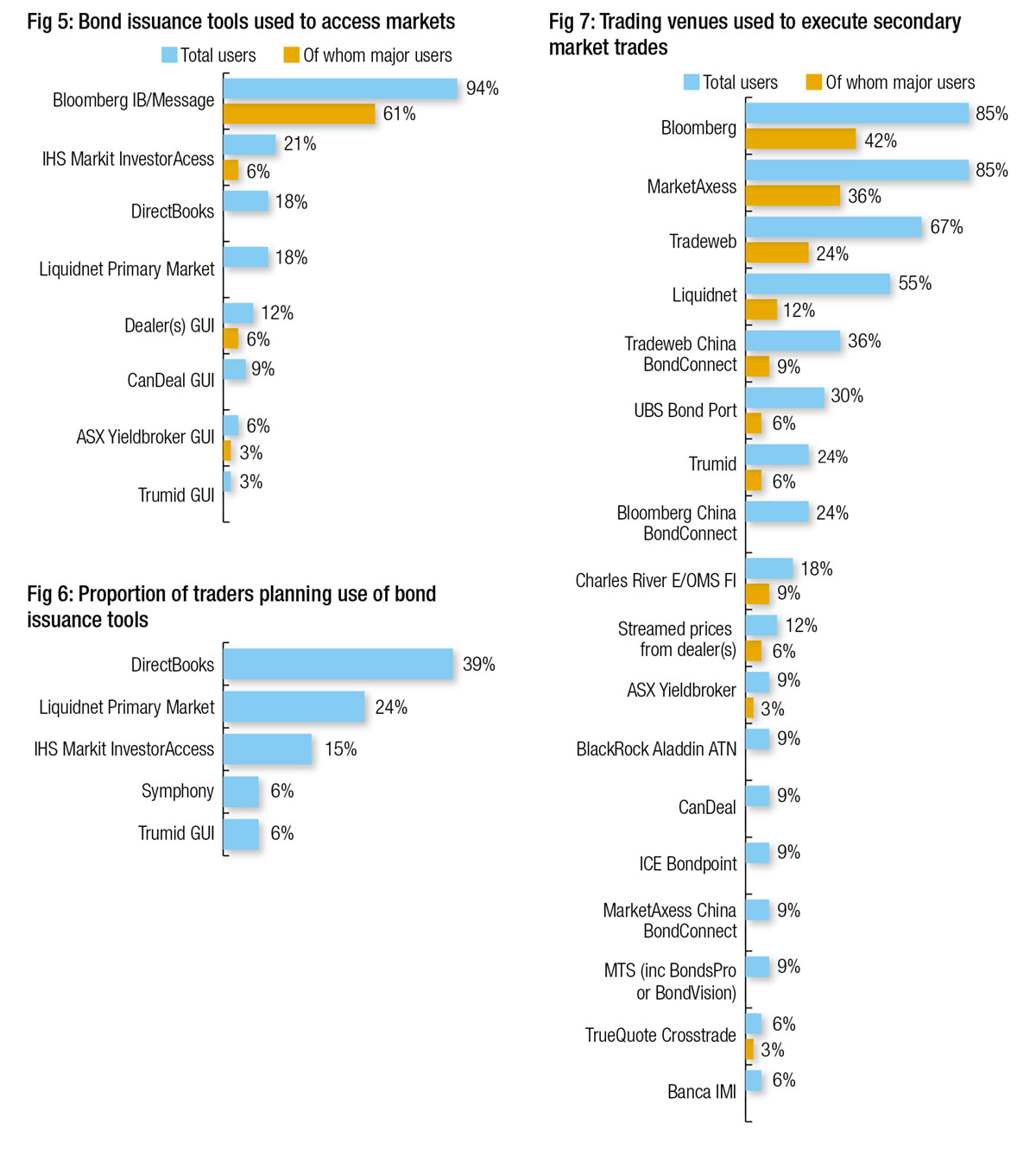

Primary markets

Tackling new bond issues on the buy side is still a priority, even as rates rise and issuance levels begin to fall, making the advances of new and existing players really key to more efficient trading desks. This year we have seen growth for Bloomberg, DirectBooks and Liquidnet in this space, the latter two having mustered low single figure users last year and yet each taking 18% this year. Bloomberg’s IB/Messaging tools have been sharpened with natural language processing since last year, allowing traders to reduce the number of manual processes in engaging with them, helping it to maintain the lead with a nine percentage-point increase.

DirectBooks and Liquidnet also present the lion’s share of future growth, on a similar chart to last year, although with slightly lower figures as some prospects have been converted to users in the interim. IHS Markit’s InvestorAccess tool also has decent future growth and with many firms talking about interoperability it will be interesting to see how these players expand into a wider technology eco-system that can still offer efficiency over fragmentation.

Secondary markets

Bloomberg and MarketAxess are neck-and-neck this year as the most used venue for credit trading, with Bloomberg’s proportion of ‘major users’ edging it over the line into first place. Tradeweb’s growth last year has fallen back a little, although its China BondConnect platform grew well, while Liquidnet has kept on a par with 2021. With no big shake up across the big four, and UBS Bond Port retaining its position as fifth most popular platform in credit, the real story in secondary trading comes from Trumid, which at 24% of respondents has jumped by 10 percentage points since last year. Another slower but just as interesting development is Charles River, which has increasingly been able to offer execution in trading venues through enhanced connectivity – every year it grows a little more.

Bloomberg and MarketAxess are neck-and-neck this year as the most used venue for credit trading, with Bloomberg’s proportion of ‘major users’ edging it over the line into first place. Tradeweb’s growth last year has fallen back a little, although its China BondConnect platform grew well, while Liquidnet has kept on a par with 2021. With no big shake up across the big four, and UBS Bond Port retaining its position as fifth most popular platform in credit, the real story in secondary trading comes from Trumid, which at 24% of respondents has jumped by 10 percentage points since last year. Another slower but just as interesting development is Charles River, which has increasingly been able to offer execution in trading venues through enhanced connectivity – every year it grows a little more.

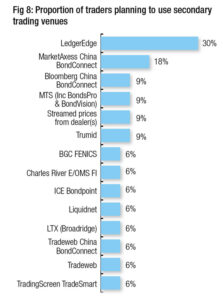

It is perhaps not surprising that a third of traders are planning to use LedgerEdge as a trading venue – based on its performance in the other categories – but that makes it no less impressive. For a firm that did not register as a prospective trading venue in 2021, it has clearly built a solid groundswell of support.

MarketAxess’s China BondConnect is relatively new and clearly 15% of traders are keen to get into the market through that portal, but there are limited other new offerings that traders are keen to onboard. Trumid again stands out, with a 9% pipeline for new business up considerably on last year, and also LTX, the platform from Broadridge promising to make a splash over the next year.

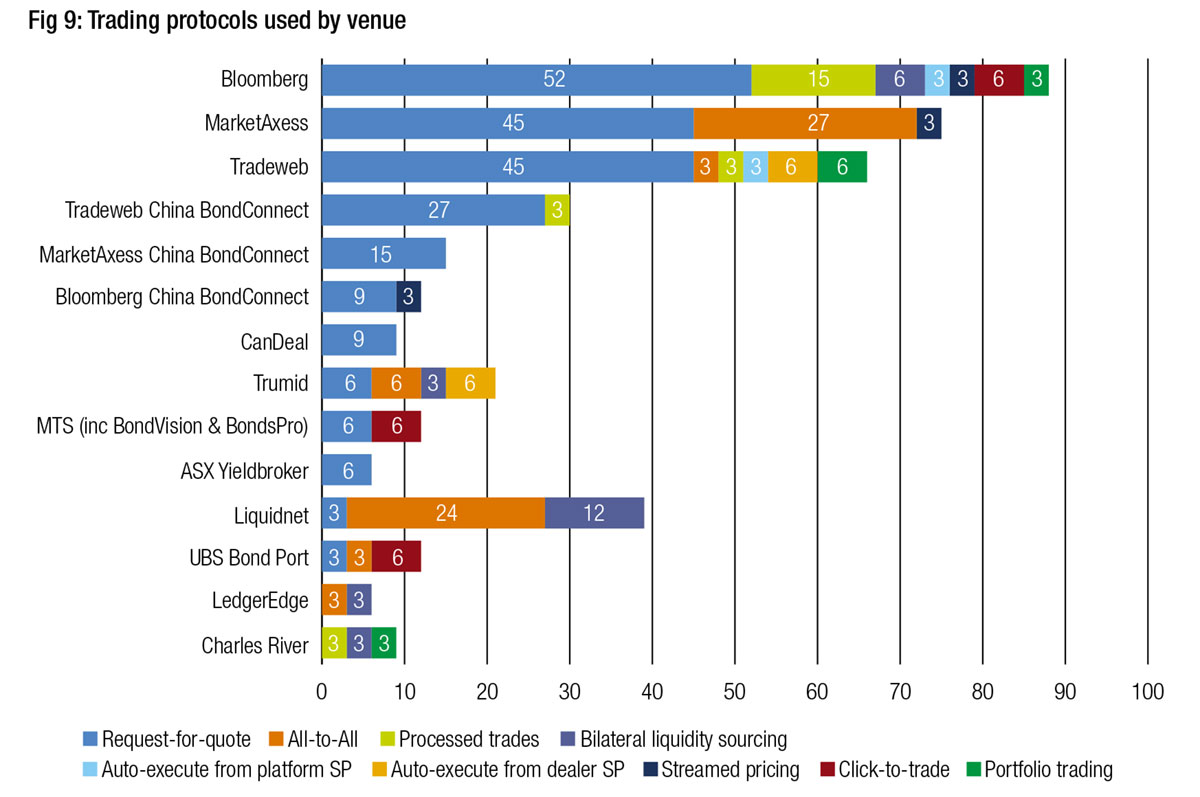

Execution protocols

The request-for-quote protocol is still the dominant trading protocol with roughly half of all traders using this as their main trading mechanism across Bloomberg, MarketAxess and Tradeweb. Low touch trading has been best used on Bloomberg, UBS Bond Port and MTS with click-to-trade and auto-execution for platform streamed pricing used at low levels across MarketAxess and Bloomberg, with auto-execution against dealer streamed price more common on Trumid and Tradeweb. All-to-all is still mainly used on MarketAxess and Liquidnet, with small amounts showing up across a variety of other venues. Portfolio trading is clearly small but growing on Tradeweb, while Bloomberg and LedgerEdge are also seeing low levels of use.

Effectiveness at finding liquidity

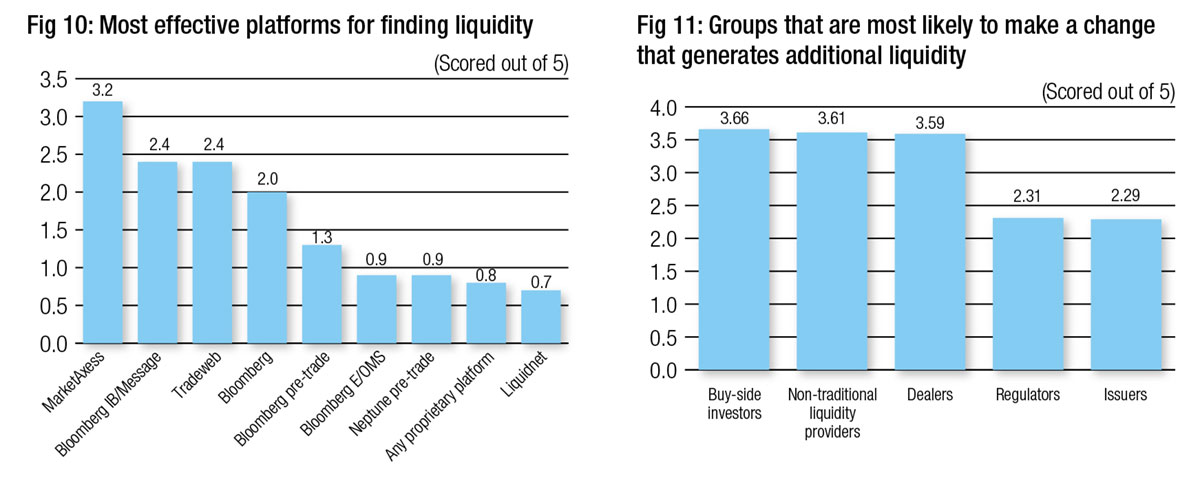

Ranked out of five, MarketAxess’s venue is seen as the most effective tool for finding liquidity, followed by Bloomberg’s IB/Messaging tool and Tradeweb’s market, the former having caught up with the latter over the past year. Bloomberg’s suite of tools collectively make a higher proportion of the top tools or liquidity sourcing than any other firm. It is clear to see that many buy-side firms building their own proprietary tools see these as highly effective, supported by the data provision of commercial operators and internal data sources. Neptune and Liquidnet are both ranked as highly effective at finding liquidity, both ranking within the top five providers by company.

A real change in perspective this year has been expectations of who is most likely to support the generation of additional liquidity. Where buy-side traders have been seen as the best bet since this survey began in 2015, non-traditional liquidity providers and dealers are now perceived to be within a point of equalling the buy side potential, which shows quite how far those parts of the market have evolved over the past seven years.

Demographics

Demographics

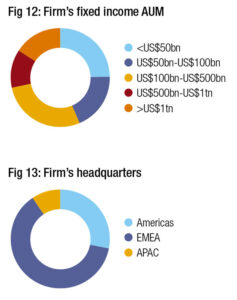

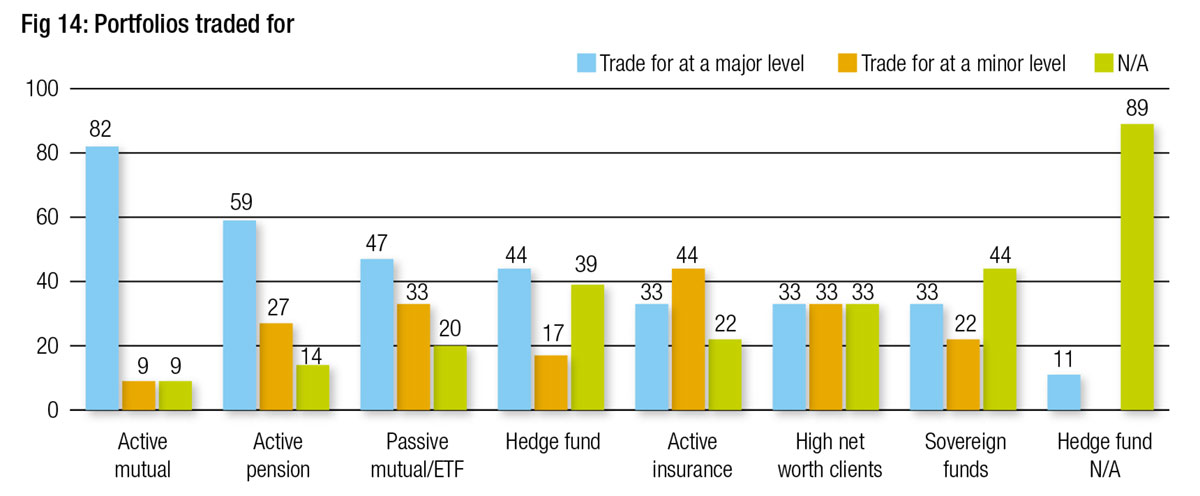

This year our research took in the views of 33 buy-side firms, including firms with a huge range of fixed income assets under management, from sub-US$50 billion to over US$1 trillion. The majority are headquartered in EMEA, and the desks trade for a wide range of portfolios including long-only, real money funds from mutual, pension and insurance businesses, passive funds and hedge fund/total return portfolios.

Neptune: King of the data ocean

Neptune, the data connectivity network which supplies sell side axes and inventory to the buy side on a pre-trade basis, has seen its use amongst asset managers increase significantly over the past year.

Neptune, the data connectivity network which supplies sell side axes and inventory to the buy side on a pre-trade basis, has seen its use amongst asset managers increase significantly over the past year.

In this year’s survey, Neptune is easily the most highly used independent pre-trade data source, achieving nearly twice the proportion of use than proprietary buy-side analytics platforms, which are the next moist used independent pre-trade data sources.

Pre-trade information is in great demand from both buy- and sell-side trading desks but the quality and frequency demanded has proven challenging for many independent provider to supply.

“JP Morgan’s recent e-trading survey, showed that 80 per cent of their clients expect to use more e-trading this year,” says John ‘Coach’ Robinson, CEO of Neptune, the axe-streaming service. “To do that you are going to need high quality and actionable data. At Neptune we only really want to take in axes and inventory, and we discourage runs. Now more than ever you have got to depend on actionable axes. An indication or run that you can’t act on, is borderline useless.”

Backed by sell-side firms, Neptune has enabled a standardised and streamlined way for buy-side desks to consume dealer trading information, such as axes, so that traders can better assess how and when they might achieve best execution.

“Clients take in Neptune data in three different ways, those that have proprietary order/execution/portfolio management systems (O/E/PMS) themselves and can aggregate the data; others that are hooked up via a commercial OMS and EMS, we are integrated with Charles River, Aladdin, FlexTrade, TradingScreen and so on,” says Robinson. “Thirdly are those using our web based graphical user interface (GUI).”

“Clients take in Neptune data in three different ways, those that have proprietary order/execution/portfolio management systems (O/E/PMS) themselves and can aggregate the data; others that are hooked up via a commercial OMS and EMS, we are integrated with Charles River, Aladdin, FlexTrade, TradingScreen and so on,” says Robinson. “Thirdly are those using our web based graphical user interface (GUI).”

Having established the quality of data, Neptune has found a strong user base across investment and trading teams, supporting the need to assess liquidity and price much earlier in the investment process.

“Clean data helps with pre-trade transparency, portfolio construction using different parameters, multi-directional trading and so on,” he explains. “It also helps them identify how much it’s going to cost to build the portfolio when they have access to all this clean data. They are not guessing what the levels are going to be, they know what the levels are.”

The firms has also worked hard to deliver data to support new trading protocols, such as portfolio trading, which has been effective across bilateral and platform trading.

“We have been really working hard to get axes from portfolio trading desks, it’s been a big effort for us,” Robinson asserts. “We have been very successful in that, because the clients want to use portfolio trading desk axes for portfolio construction, or just to track the flows.”

To evolve its services further, Neptune is now looking at product development, based on an enhanced application of data science.

“We recently hired a data scientist who will drive our data strategy,” says Robinson. “We are going to create a data product for buy-side clients to receive products like liquidity scores, composites and data sets. We are going to create a data package that goes back to the dealers themselves, so they can track what they send out versus the competition in terms of quality and quantity on their axes.”

Erratum: for all instances of ‘Banca IMI’; this should read ‘MarketHub (Intesa Sanpaolo CIB)’

©Markets Media Europe 2022

©Markets Media Europe 2026

more valuable")