By Boon Peng Ooi, chief investment officer for fixed income, at Eastspring Investments.

Over the past two years, a “strategy” of “tactically” trading risk has looked appropriate given both the tighter spreads that have prevailed and the better valuations seen at the longer-duration and higher-risk ends of the bond universe. With the 2018 outlook little different from that earlier this year, such an approach still seems relevant for today’s environment.

While there could be some uncertainty generated around both monetary policy and various geopolitical issues, we would be surprised to see a “Minsky” moment, i.e. a sudden major collapse of asset values that is part of an extended credit or business cycle.

Many commentators, for example, are concerned that “rich” US equity valuations will lead to sell-offs that trigger a bear market. Similar concerns are evident in the bond market where the JP Morgan Asian Credit Index spread is hovering around a low 220 basis points compared with its 10-year historical average of 304 basis points (from Bloomberg as at 30 October, 2017).

While acknowledging these concerns, we are not convinced: we see several outweighing factors.

The global economy, for example, continues to chug along with inflation seemingly under control. Oil prices look poised to remain within a trading band unlikely fueling inflation. And while central banks are either tightening or poised to tighten, indications are that any tightening will be gradual; it will likely generate waves that rock the boat, which we will trade through, but waves insufficiently high to sink it.

Perhaps most telling, is the benign global inflation outlook; core inflation in the US, Eurozone and Japan seems set to either remain subdued or fall short of target. Rising UK inflation is something of a “red herring”, it seems, in that the bulk of the rise can be laid firmly at the foot of sterling’s post-Brexit fall.

Structural factors also make it difficult for inflation to move significantly higher.

The full implications of an aging demographic, for example, are only slowly dawning on policy makers it seems. We are now encountering an aging workforce, with many of the over 55s active in the workforce. Older workers may need to be “reskilled” for the new-economy, higher-paying jobs. Many may “need the job” and will accept low or no pay increments. In addition, low productivity may constrain the ability of employers to pay higher salaries.

As a result, there are strong grounds for arguing that the upward pressure on wages, for which various central banks have not only been looking but also basing policy, will be muted.

With low inflation projected, the major central banks can afford to be gradual in their monetary tightening trajectory. Indeed, the US Federal Reserve’s 14 June 2017 press release, when it announced the path of its proposed monetary tightening, is infused with caution suggesting a quick response in the case of any policy misstep.

At this point, monetary policy “forks”, with central banks trying to control both the volume of money and interest rates. Both have different implications for the bond markets.

The Fed is shrinking its balance sheet, with both the European Central Bank and the Bank of England hinting that they will begin tapering asset purchases at some time in the coming year. Sceptics argue that this will kill growth. In contrast, we view such moves positively believing they will head-off excessive risk-taking.

We cannot see the Bank of Japan pushing its Yield Curve Control target for its 10-year government bond yield higher from the current 0% given stubbornly low inflation. The impact of this policy on the volume of money is indirect; effectively, the Bank has told the government it will “print” whatever money is required to effect government policy.

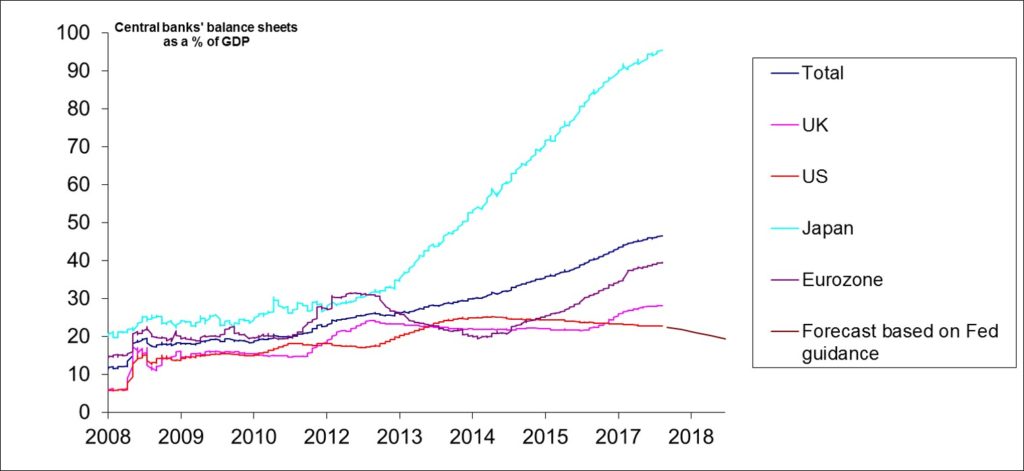

The long and short of this policy switch is that liquidity should support the financial markets in 2018 albeit less aggressively than in the past (refer to Fig 1).

Fig 1: Cautious central bank claw backs should support liquidity in 2018 Source : Central banks for balance sheet data plus official sources for GDP from Datastream as at 10 November 2017.

The US estimate for 2017/2018 is based on US Federal Reserve Board announcements and the consensus GDP forecasts from Consensus Economics as at 10 April 2017

This is not to say that we see monetary tightening as a total non-event.

Credit spreads, for example, should widen. There is a possibility that shrinking US liquidity could trigger US equity selling but we think this possibility has a low probability. On the whole, the impact of the quantitative easing unwind should be pretty much contained; not only is preserving economic and financial market stability (a basic tenet of central bank policy) but also we have already hinted that the initial phase of the Fed’s balance sheet reduction is intentionally limited.

The second “fork”, rising US interest rates, could, however, trigger volatility in both bond and currency markets.

While the Fed, for example, has been (relatively) clear in its intentions to hike rates by ¼% in December 2017 with a further ½% in 2018 , this trajectory is still being underpriced by US interest rate markets, in our view. Investors may have priced in a more benign inflation outlook than is warranted. We too see benign inflation, but not that benign.

Critics of our view could argue that we are conveniently extrapolating our view of credit and asset markets towards a “soft-landing”.

Our response is that compared against history, this “normalization” cycle will be more muted. We are faced with the prospect that global interest rates will rise and credit spreads expand, but the conditions suggest that the longer-term value can quickly re-emerge.

We still see opportunities in Asian credits and emerging market local currency bonds

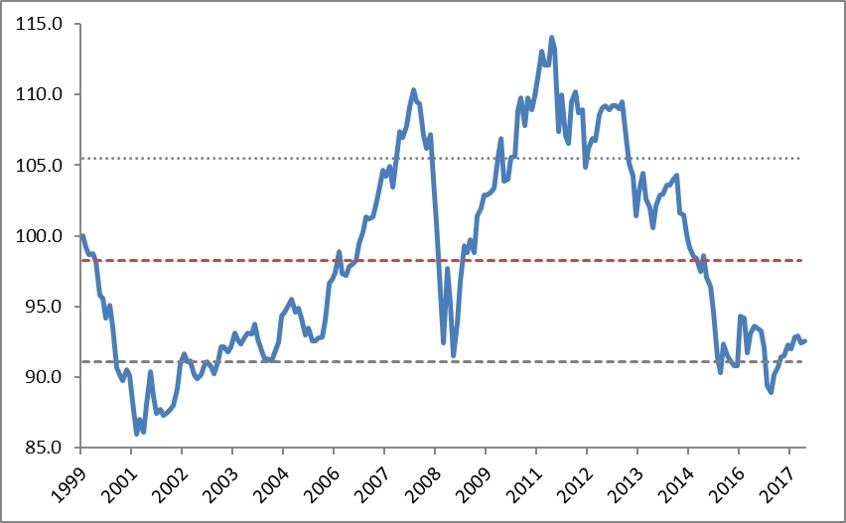

The latter could benefit from currency tailwinds (refer to Fig 2) given those attractively valued emerging market currencies, which are at the cheaper ends of their historical trading ranges (although the US dollar could see bouts of strength as, and when, US interest rates rise). Emerging market and Asian local currency bonds offer longer term value, we think.

Fig 2 ; Many Asian foreign currencies are trading at recent lows against the US dollar

Source: Eastspring Investments based on exchange rate data vis-à-vis the US dollar from Bloomberg as at 10 November 2017. The above index is an equal weighting on a month-end basis of the Asian currencies vis-à-vis the US dollar rebased to 100. The index does not include Hong Kong’s dollar given its currency peg to the US dollar.

The underlying environment, however, remains one of tighter spreads and yields that may not move much lower. The trick to successfully navigate this world will be to remain nimble, and “tactically” trade value opportunities as and when they appear.

©TheDESK 2017

©Markets Media Europe 2026

more valuable")