Average bid-ask spreads have been expanding and contracting like an accordion as investors and liquidity providers struggle to form a coherent view on inflation, growth, interest‑rate policy, and risk appetite, a result of the Iran conflict.

Rising yields have triggered a sell-off in some secondary markets, while primary issuance has been supported by big tech deals, with trading in US investment grade bonds hitting a record volume of US$260 billion in the week of 9 March according to MarketAxess data, with Amazon issuing US$37 billion on Tuesday 10 March.

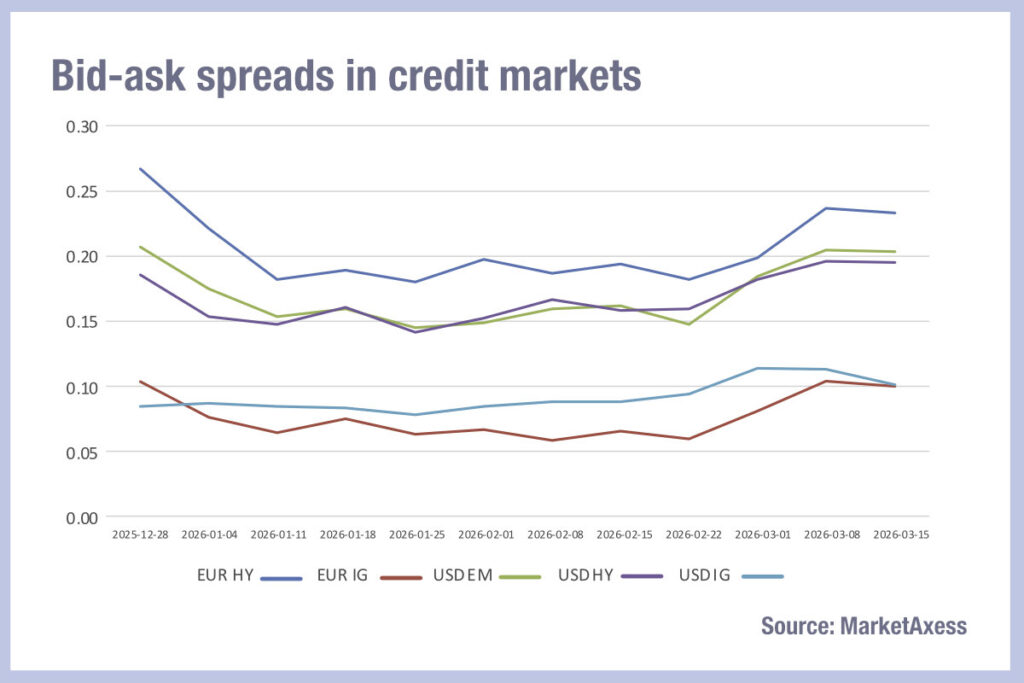

Buy-side bond traders will need to keep a close eye on trading costs and timing as they seek to optimise execution on behalf of their portfolio managers.

Looking at MarketAxess CP+ data which compiles a a consolidated price, we see that investment grade, high yield and emerging market USD bonds all saw spreads jump by around 0.05 of price % of par at the end of February, before flattening or declining slightly from early to mid-March.

A central source of confusion in markets is the volatile oil price, which has pushed Brent crude above US$100 per barrel at several points, raising expectations of inflation and subsequent responses from central banks. They may need to keep interest rates elevated or even hike them, to counter inflationary trends. This dynamic has driven bond yields sharply higher, notably UK gilt yields but also US Treasury yields, undermining the historical role of government bonds as risk free assets in geopolitical crises, which can push yields lower as investors seek safety.

This inversion of the usual “flight to safety” pattern is one of the clearest signs of market confusion. Instead of rallying, Eurozone government bond yields spreads have risen by an average of 29bp since 27 February according to Fitch Ratings.

“If the higher cost of borrowing is sustained it would add to medium-term fiscal pressures through higher interest costs as debt matures and is refinanced at market yields,” wrote Fitch analysts on 17 March. “We do not view these dynamics as creating near-term ‘fiscal cliffs’ for developed markets (DMs), but they could reduce room for manoeuvre if the energy price shock persists and growth weakens.”

Credit risks are also growing. The war has amplified existing concerns in private and public credit markets. Disruption to trade and cashflows is likely to make financials and corporates delay spending and build cash buffers.

Investors are struggling to reconcile the inflation shock with the possibility of slower global growth or even recession, conditions that might normally support bond investment.

The conflict also raises the risk of stagflation, a combination of high inflation and weak growth. Analysts warn that the longer the conflict disrupts the Strait of Hormuz – through which around 20% of global oil supply passes – the more persistent the inflation shock becomes. At the same time, higher energy costs threaten household spending, corporate margins, and government finances, as politicians seek to alleviate the pressure on households.

This dual pressure can leave bond investors unsure whether to price in tighter monetary policy or deteriorating economic fundamentals.

Central‑bank policy expectations add another layer of uncertainty. The Federal Reserve, for example, is expected by many analysts to cut rates once or twice in 2026, but elevated inflation could delay or even reduce those cuts. Markets are now pricing fewer rate cuts than they were before the conflict, contributing to volatility in sovereign bond yields.

©Markets Media Europe 2025

more valuable")