The US is seeing a drop off in lower grade debt issuance so far in 2026, relative to 2025 levels, while higher grade US debt, and European markets are seeing issuance growing, potentially reflecting both base rates and expectations of rate cuts.

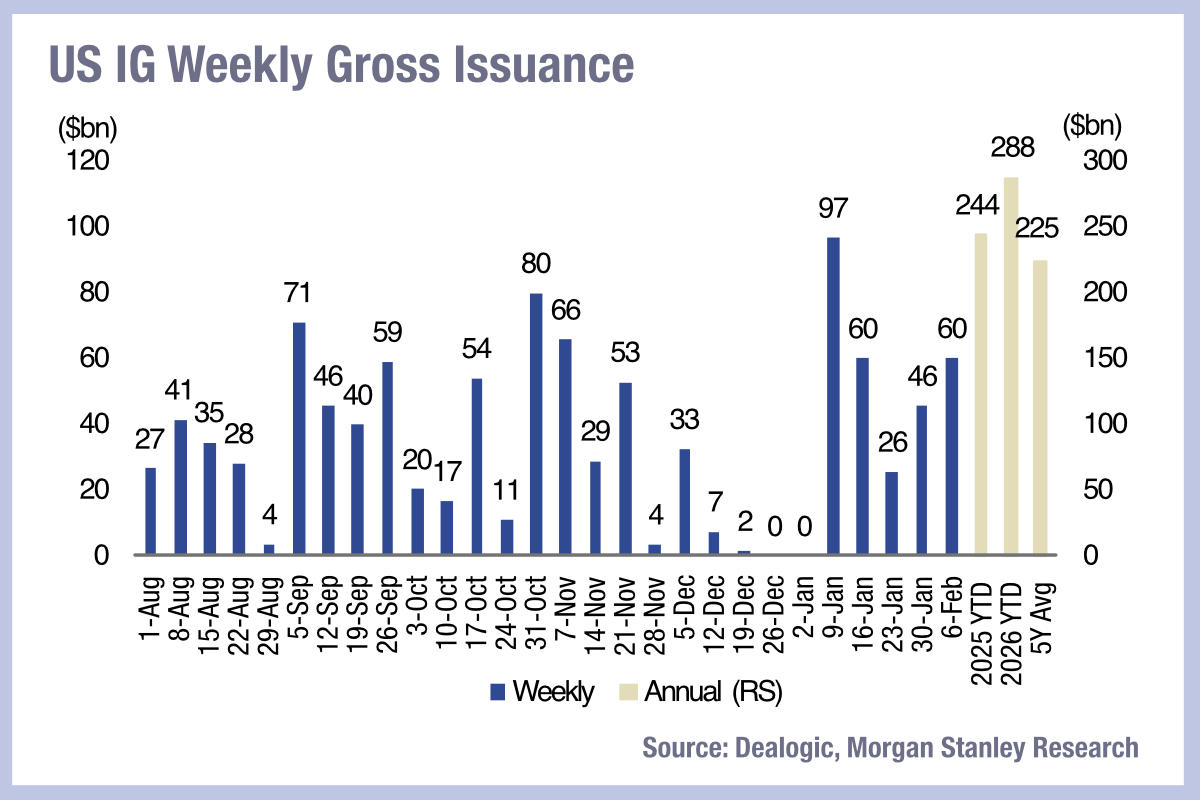

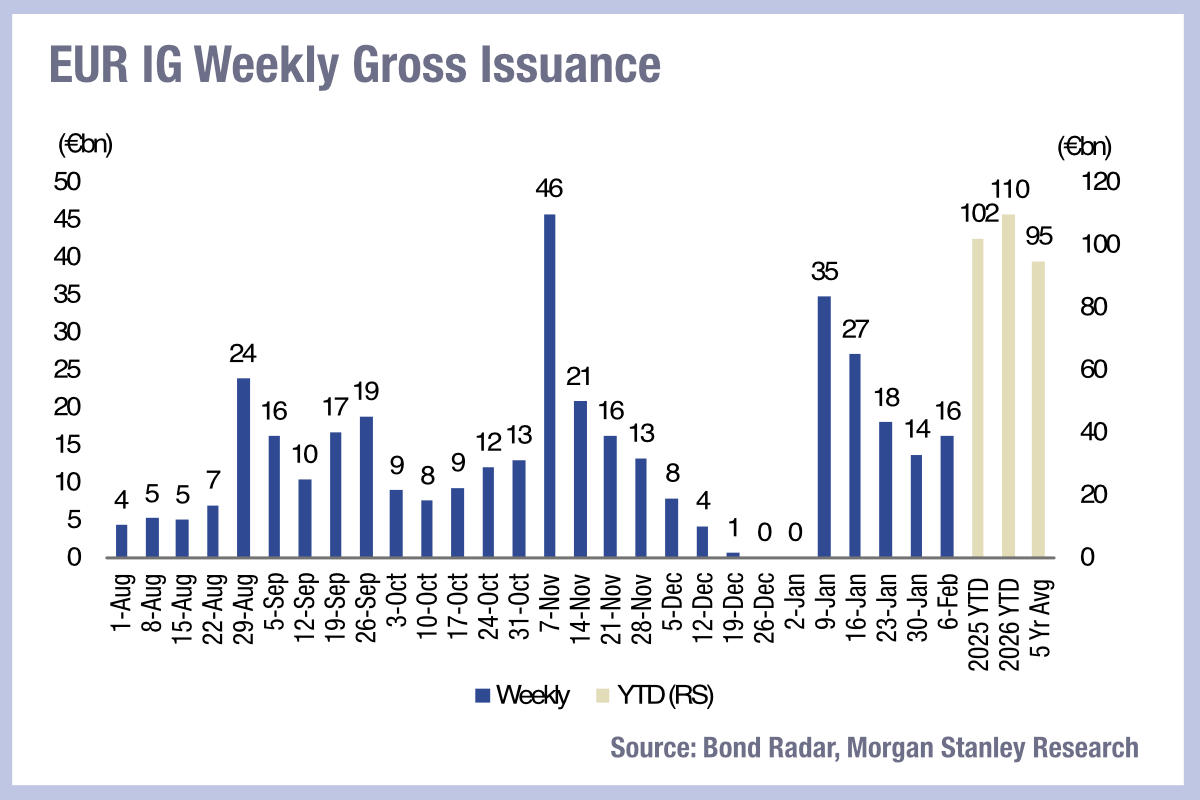

Investment grade bond issuance reached US$60 billion in the first week of February, with year-to-date (YTD) supply tracking at US$288 billion, according to Morgan Stanley, in total up 18% year-on-year (YoY). European IG new issues reached €16 billion the same week, making YTD volumes for January €110 billion, an 8% increase YoY.

With US IG spreads widening by 2 basis points (bp), and European spreads widening by 1bp, US IG was nursing 6 bp losses and European excess return was flat, but funds still saw net inflows, with $22 billion YTD into US funds and $3 billion YTD into European investment vehicles.

In high yield (HY) markets supply is levelling off in the US where YTD supply for US HY has reached $34 billion so far, up 1% YoY, but in Europe HY issuance has reached €19 billion YTD, up 51% YoY.

As the US leveraged loan market is substantially larger than HY in US markets it is worth flagging that leveraged loan issuance reached US$6 billion in the first week of February, with YTD supply tracking at US$59 billion which is down 21% year-on-year.

This difference may reflect current rates and rate cut expectations in 2026, with two cuts widely expected in the US, which has base rates set by the Federal Reserve at a 3.5-3.75% range, where the European Central Bank (ECB) has held rates steady at 2% this year.

©Markets Media Europe 2025

more valuable")