Global futures volumes are up 71% between 2019 and 2025 with fixed income being the engine for that growth. A new Crisil Coalition Greenwich report makes clear that the macroeconomic environment of the past several years has been unusually fertile ground for rates and credit derivatives activity, and that the structural conditions which produced that growth show little sign of abating.

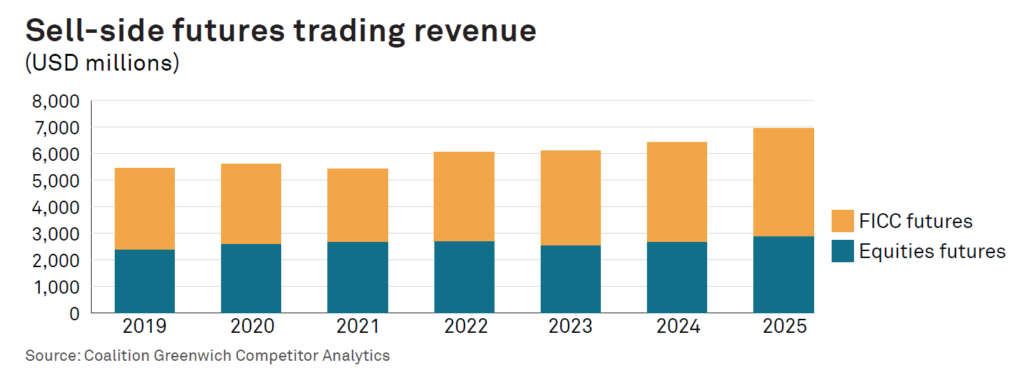

The report breaks out sell-side futures revenue by asset class, showing FICC futures revenue rising 35% between 2019 and 2025, outpacing the 21% growth recorded by equity futures over the same period. That gap is meaningful. It reflects the degree to which the rate cycle that began in 2022 — the most aggressive tightening by major central banks in a generation — created both hedging necessity and speculative opportunity across the fixed income complex. Interest rate futures and options volumes surged as market participants scrambled to manage duration risk, express views on terminal rates and hedge mortgage and bond portfolios against a backdrop of historically unusual volatility in government bond markets.

Beyond the volume story, the revenue composition reveals something important about how fixed income derivatives generate returns for intermediaries. The report notes that much of the revenue growth from 2022 onward reflected not just trading commissions but interest income that futures commission merchants (FCMs) captured from client margin accounts. In a zero-rate environment, margin balances earn nothing. At 5%, they become a meaningful revenue line. This structural tailwind helped fixed income-focused FCMs disproportionately, given that rates and credit products typically require larger margin deposits relative to notional than equity derivatives.

Looking forward, the report points to two factors with particular relevance for fixed income and credit. The first is the expected relaxation of dealer capital requirements in the United States, which could expand sell-side balance sheet capacity for market-making in both listed and OTC derivatives. OTC credit derivatives — including credit default swaps and total return swaps — remain significantly more capital-intensive to intermediate than their exchange-traded equivalents, and any reduction in the regulatory capital burden could meaningfully increase liquidity and dealer willingness to hold risk.

The second is tokenisation. The report acknowledges that tokenisation holds genuine promise for improving post-trade processing in OTC derivatives, particularly collateral management, a function that remains partly manual and is especially burdensome in fixed income and credit products given the complexity of collateral schedules, inventory management within banks across team and risk books, and the frequency of margin calls.

©Markets Media Europe 2025

more valuable")